Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

The energy transition: Geopolitical volatility and clean power assets

In this blog, we explore the conflict in the Middle East’s implications on the energy transition and whether it may bolster the case for clean power-related assets.

Key takeaways:

· A prolonged Iran conflict may accelerate the energy transition. The post‑Ukraine gas and power price shock was followed by a robust clean power buildout and reducing European reliance on natural gas. While gas reliance and prices remain far below the Russia-Ukraine highs, further escalations could push Europe back toward similar dynamics.

· The Iran war raises Europe’s energy security imperative, reinforcing, in our view, the strategic value of clean power infrastructure as a resilient energy source.

· In our view, escalation may support clean power infrastructure through two channels: stronger government impetus to accelerate buildouts, and higher power prices that boost cashflows for merchant‑exposed generators, particularly in gas‑linked markets.

· Impacts will be uneven across markets and technologies. Gas‑reliant countries are likely to see larger power price responses. Within renewables, wind assets may be well-positioned, while increased volatility should benefit battery storage and hybridised renewables assets.

Beyond decarbonisation, Europe’s energy transition is increasingly being shaped by a desire for greater energy security. Recent events in the Middle East – which we covered more broadly here – remind us that geopolitical shocks can feed through into gas and power markets, changing the outlook for clean power infrastructure.

Like before, but different…

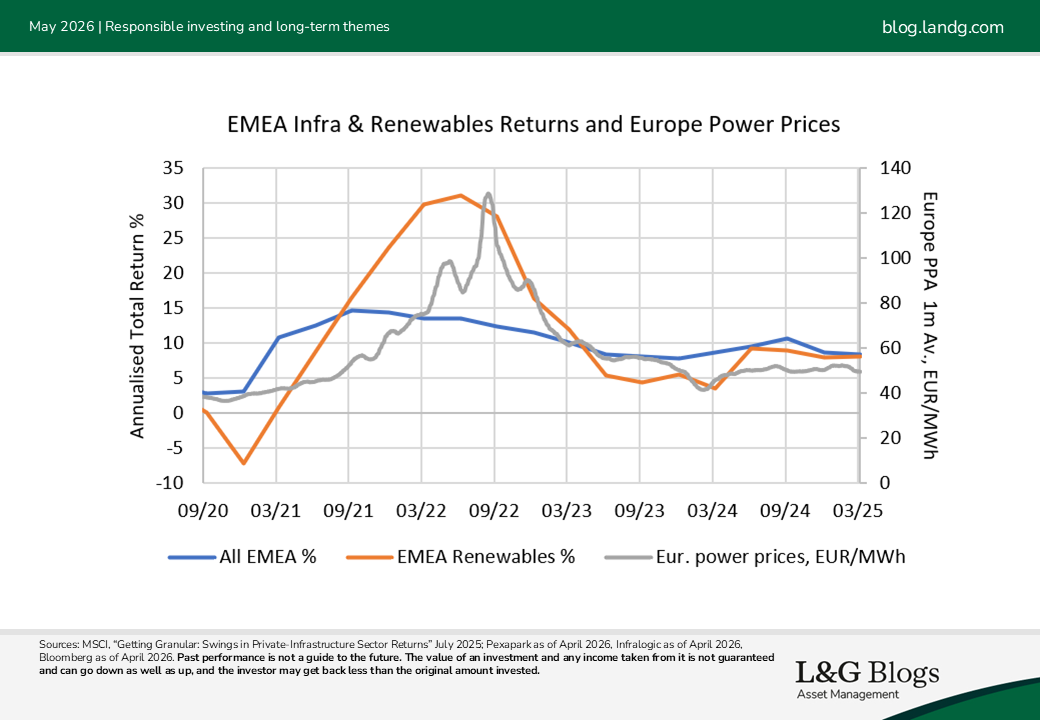

For institutional investors, there’s a lesson from recent years: when energy security is threatened, the strategic case for domestic clean power strengthens. This was evident after Russia’s invasion of Ukraine, when reduced Russian gas supplies drove a sharp rise in European power prices.

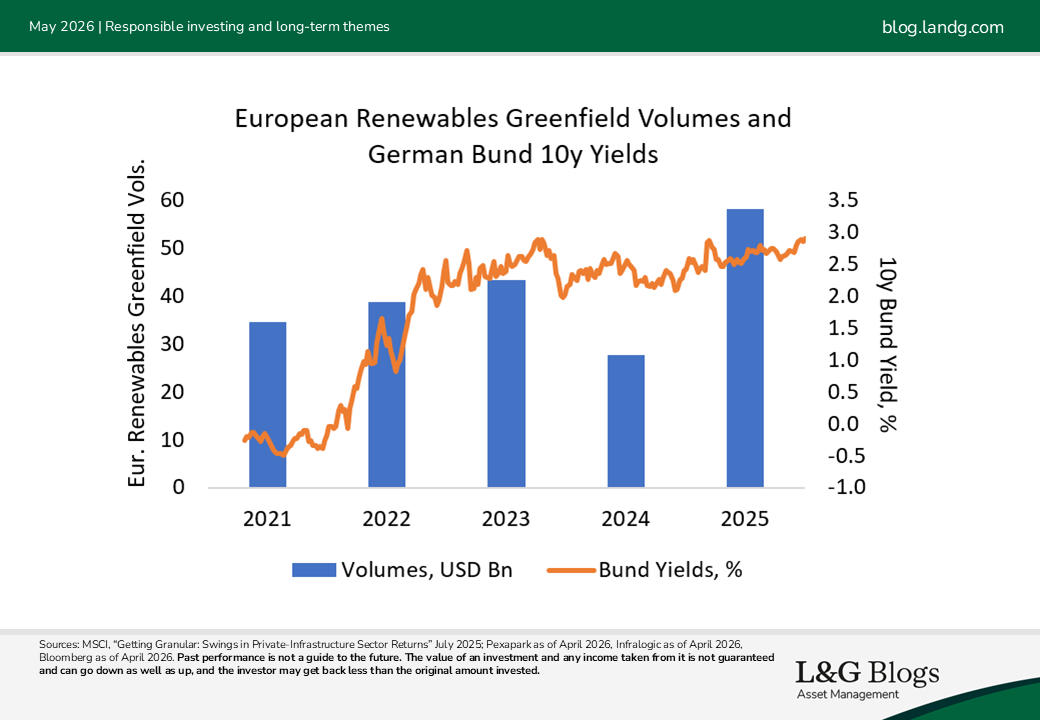

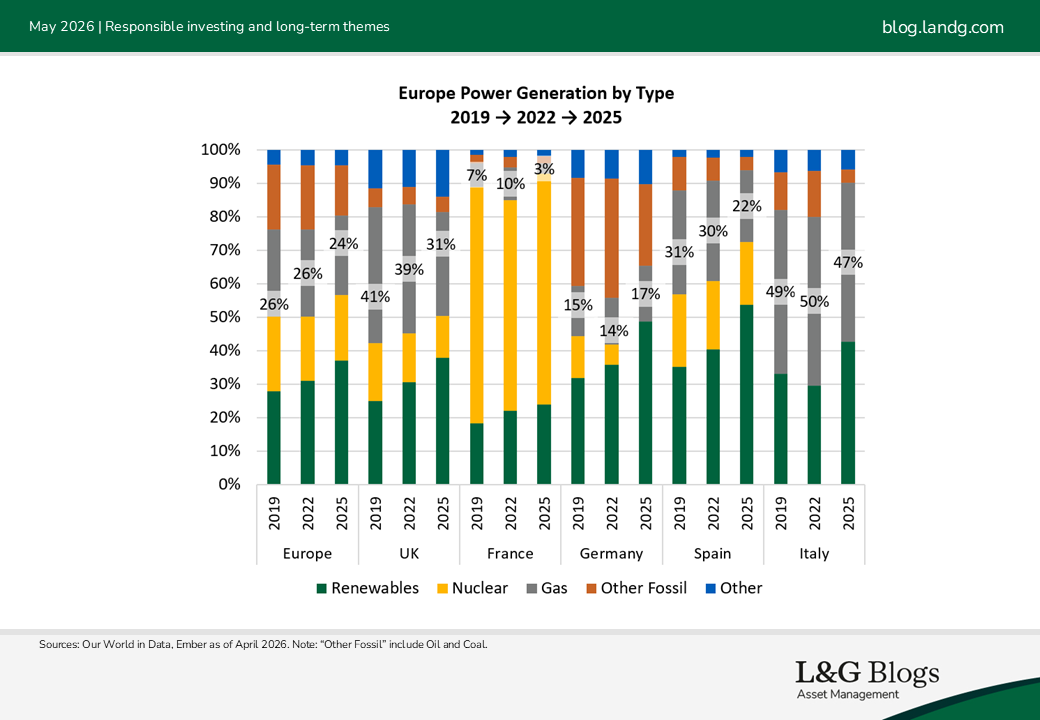

For renewable assets with merchant exposure, these higher prices were an enabler of stronger returns. Those improved returns also helped sustain development activity, even as interest rates moved higher. As returns improved and development accelerated, renewables became a larger part of the European infrastructure asset universe. More importantly, the continent began to reduce its dependence on gas-fired power generation as clean power deployment increased. That is the broader strategic result: energy shocks can accelerate the structural change from the energy transition.

This is why the Middle East conflict matters for the energy transition. It is reported that 20% of global liquefied natural gas (LNG) exports passes through the Strait of Hormuz[1], so any sustained disruption has the potential to tighten gas markets and lift prices. While European gas prices remain well below the extremes seen during the 2022 energy crisis, market scenarios suggest that several months of disruption could still raise gas prices significantly.[2]

If that happened, the same transmission mechanism we previously saw could re-emerge, in our view. That means higher gas prices feed into higher power prices, particularly in gas-linked power markets, and higher prices support cashflows for merchant-exposed clean power assets.

The investor implications

Europe is better positioned than it was in 2022. Renewables penetration is higher and dependence on gas is lower, but the direction of travel remains the same. A prolonged conflict would likely reinforce the need to accelerate domestic clean power buildout, storage and grid investment.

That said, the implications are not uniform across markets or technologies. Countries with greater gas dependence are likely to see a stronger power-price response than those with more insulated generation mixes. The UK and Germany, for example, are more exposed to gas-linked dynamics than France, where nuclear plays a larger role. For investors, in our view this likely means the impact of any renewed gas shock is likely to be highly market-specific rather than broad-based across Europe.

We believe asset-level exposure matters just as much. Not all renewable projects benefit equally from higher wholesale prices. Assets operating under fixed-price contracts may see limited immediate upside, as their revenues are largely insulated from spot market volatility. By contrast, merchant-exposed assets are more directly positioned to benefit. Within renewables, wind may be relatively well-positioned in markets where its capture price aligns more closely with the wholesale power price.

We believe higher volatility could also strengthen the investment case for battery storage and hybrid assets. In a market where gas prices rise while solar penetration continues to grow, intraday price swings may become more pronounced. That improves the revenue opportunity for flexibility assets that can arbitrage volatility and support system balancing. In that sense, geopolitical disruption may not only support renewable generation, it could also reinforce the value of storage and grid-enabling infrastructure.

We see listed markets offering a more nuanced signal. Higher expected power prices can improve future earnings for some renewable assets, but that benefit may be offset if higher inflation and bond yields discount those earnings at greater rates and compress equity risk premia. In addition, listed renewable funds hold assets with contracted revenues, which limits sensitivity to wholesale price movements. For institutional investors, this is an important reminder that the opportunity is selective: revenue model, contract structure, market exposure and financing conditions all matter.

Final takeaways

We believe the current conflict reinforces, rather than weakens, the long-term investment case for the energy transition and associated assets. It does so through two channels. First, it raises the strategic value of domestic clean power, storage and grid infrastructure as tools of energy security. This is recognised by European governments, where the escalation raises the impetus to accelerate clean power buildouts. Indeed, the European Commission is already seeking to strength EU energy resilience following the escalating Middle East conflict.[3] Second, if disruption to gas markets persists, it could improve the earnings outlook for selected clean power assets, particularly those with merchant exposure in gas-linked markets.

The experience of the past few years suggests that geopolitical stress can accelerate capital formation and policy support across clean power. The current conflict may yet prove to be another catalyst.

Key Risks

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass.The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested. Past performance is not a guide to future performance. The details contained here are for information purposes only and do not constitute investment advice or a recommendation or offer to buy or sell any security. The information above is provided on a general basis and does not take into account any individual investor’s circumstances. Any views expressed are those of L&G as at the date of publication. Not for distribution to any person resident in any jurisdiction where such distribution would be contrary to local law or regulation.

Legal & General Investment Management Ltd. Registered in England and Wales No. 02091894. Registered office: One Coleman Street, London EC2R 5AA. Authorised and regulated by the Financial Conduct Authority.

In the European Economic Area, this document is issued by LGIM Managers (Europe) Limited, authorised and regulated by the Central Bank of Ireland as a UCITS management company (pursuant to European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations, 2011 (as amended) and as an alternative investment fund manager (pursuant to the European Union (Alternative Investment Fund Managers) Regulations 2013 (as amended). LGIM Managers (Europe) Limited’s registered office is at 70 Sir John Rogerson’s Quay, Dublin, 2, Ireland and it is registered with the Irish Companies Registration Office under company no. 609677.

[1] IEA, “Strait of Hormuz, Factsheet”, February 2026

[2] Citi Research, March 2026

[3] European Commission, Commission proposes actions to protect Europeans from the fossil energy crisis, April 2026

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.