Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Energy shocks and geopolitical volatility: What the Middle East conflict has meant for private markets

In this blog we assess the impact the conflict in the Middle East has had on private markets and the outlook for these assets.

The conflict in the Middle East has led to heightened portfolio scrutiny by private markets investors. Despite a two-week ceasefire announced on 8 April, there remains significant uncertainty. Much of this centres on if the ceasefire will hold and when the world might return to ‘normal’.

The conflict has led to energy prices rocketing, volatility in equity markets and bond yields rising. The current energy shock is feeding through to inflation expectations, especially in energy-sensitive Europe and the UK. While there are echoes of 2022, the difference is that the starting point is weaker; growth is softer, inflation is still above target and borrowing costs were already elevated pre-conflict.

A tricky environment to navigate for private market investors

Private markets are not marked to market meaning lower day-to-day volatility, but nor are they insulated from macro and geopolitical stress. Higher energy prices can squeeze margins, raise development costs and weaken demand.

The areas most exposed are those with high energy intensity, large capital expenditure needs, long supply chains or meaningful dependence on consumer spending and GDP growth. Manufacturing, transportation, leisure, retail and other consumer-facing businesses look more vulnerable if the shock proves persistent.

The second transmission channel is the cost of capital. Government bond yields feed into discount rates, debt costs and valuation assumptions across private equity, private credit, real estate and infrastructure. Uncertainty can also slow transaction activity. When rates and inflation expectations are moving sharply, we expect bid-offer spreads to widen, making new transactions and exits harder to execute and resulting in a likely pause in deal making.

Private credit: Higher yields, but pockets of higher borrower stress

Private credit sits in the middle of this tension. On one hand, higher base rates and some spread widening should, in our view, improve prospective returns for new lending.

On the other hand, higher debt servicing costs increase pressure on borrowers, especially in sub-investment grade direct lending where debt is commonly floating-rate. While we expect well-diversified portfolios that have been prudently underwritten to be resilient, there may be heightened default risk in the lower credit quality borrower segment where leverage and exposure to cyclical sectors are greater. Return potential may be improving but, in this environment, we believe credit quality matters more than ever.

Infrastructure and energy: Resilience is selective

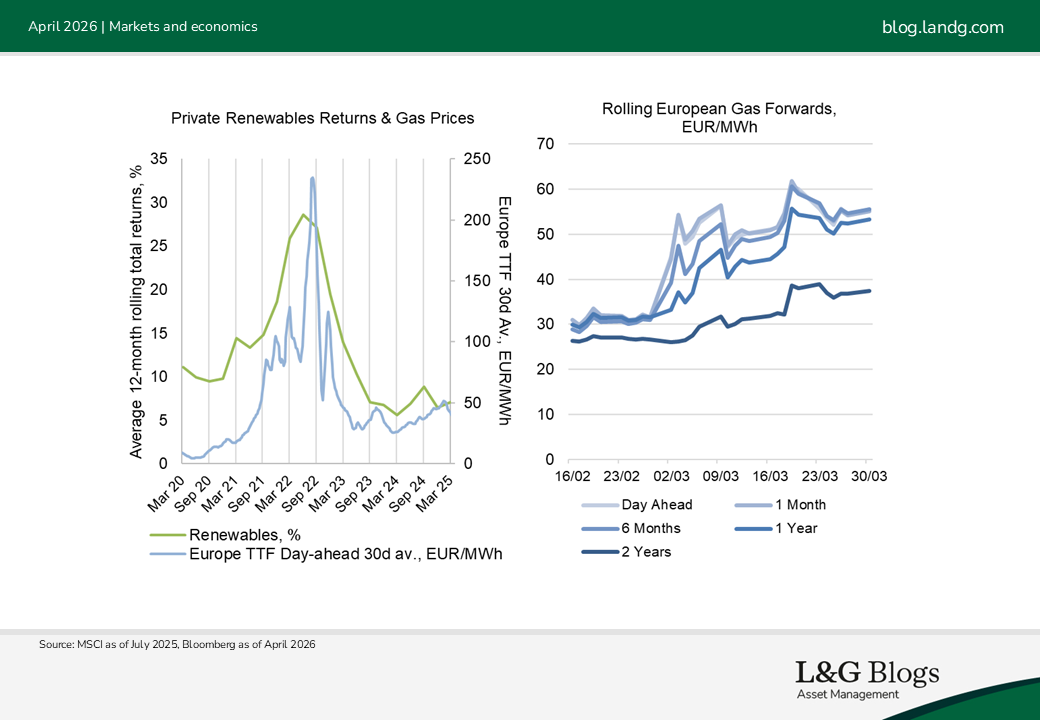

Infrastructure is often viewed as defensive, and in many cases that still holds. But the current environment demonstrates that resilience may be dependent on asset structure. In renewables, for example, some assets may benefit from higher power prices if they retain merchant exposure[1], while those on fixed-price contracts may capture less upside.

Cashflow impact is not uniform. With inflation linkage, infrastructure showed stable returns relative to other private asset classes following the energy crisis in 2022, so the elevated geopolitical tensions may retain investor interest in infrastructure as an enabler of portfolio resilience.

In our view, the investment case for energy transition infrastructure may be strengthening. Gas-reliant markets such as the UK, Germany and Italy have seen sharper moves in forward power prices, reinforcing the need for domestic energy production, storage, electrification and broader energy security. With battery storage supporting inflexible generation, accelerating the buildout of clean power for energy security further bolsters the investment case for grid-enabling infrastructure.

Furthermore, the volatility of the gas forward markets demonstrates investor uncertainty on the level and duration of the conflict’s impact, with higher prices likely over the medium term too, given the damage to Middle East gas production facilities. Therefore, we believe even a short-term geopolitical shock may deepen structural themes that were already shaping private market opportunities.

Real estate: Prime assets are holding up better

In real estate, listed markets have reacted faster than direct property. Rising gilt yields have weighed on UK REITs, which are highly sensitive to moves in the risk-free rate. Direct real estate is typically slower to adjust and pricing is influenced by many other variables such as rental growth expectations. Furthermore, in many cases yields remain quite high following the 2022 correction, potentially providing investors with some insulation against risk. For now, there is not yet strong evidence, in our view, that another wave of repricing is imminent.

Strategically, uncertainty supports allocations to lower beta (i.e., less economically sensitive) sectors like residential, but cyclical repricing since 2022 highlights yield insulation elsewhere, such as high-quality office and retail. Portfolios weighted to good quality, well-located assets with sensible cash and liquidity management at fund level will be best placed to weather current uncertainty as well as offering outperformance prospects. Significant alpha potential remains in segment, location and asset selection alongside active asset management.

If higher inflation lifts construction costs again while financing remains expensive, project viability could come under renewed pressure, but this would also limit supply risk and may be an upside to rental value over the medium term, assuming economic growth recovers.

Capital flows, bargaining power and resilience

We believe the conflict could also shape capital flows into private markets. If public market values fall again, despite the ceasefire being in place, some institutional investors may face a renewed denominator effect due to lagged private market valuations. The volatility may also drive a more cautious attitude towards new commitments. That need not mean a collapse in demand, but it could make fundraising more selective, favouring managers with clear differentiation and resilient portfolios. On the other hand, we do believe it is conceivable that equities may recover strongly, underwritten on relatively shaky geopolitical signals. Private assets may offer more attractive yields on firmer valuation foundations in this scenario.

For investors with capital to deploy, volatile markets can also improve bargaining power. The key, in our view, is to remain disciplined. Not every dislocation is an opportunity, but periods like this may potentially create attractive entry points for investors focused on quality and downside protection.

More broadly, the episode reinforces the importance of resilience. Assets with visible cashflows, inflation linkage and pricing power may, in our view, be better placed to outperform. It also strengthens the case for investment themes linked to deglobalisation, including supply chain resilience, domestic manufacturing, defence and energy independence.

Looking onward

From a private markets perspective, we believe this is less a broad risk-off episode than a story about selectivity. Despite the ceasefire, the geopolitical backdrop remains volatile and fragmented. The current shock may raise the hurdle for cyclical, leveraged and development-heavy exposures. At the same time, it may strengthen the appeal of assets linked to energy security, inflation protection and essential services.

For institutional investors, we believe the opportunity is likely to come from allocating capital more deliberately – towards resilient sectors/geographies and managers with proven underwriting discipline and operational capability.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass.

Past performance is not a guide to the future.

[1] “Merchant” refers to selling electricity directly to the wholesale spot market and thus exposed to the prevailing energy price.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.