Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Scope and mirrors – Potential illusions in corporate Scope 2 emissions disclosures for investors

In this blog, we look at the various ways corporate Scope 2 emissions can be disclosed and the nuances that investors may wish to be aware of.

Scope 2 emissions, which come from companies’ consumption of purchased electricity and heat, are central to the pace of the energy transition. Electricity generation is responsible for a quarter of global emissions, the majority of which is used by companies.[1]

The measuring and reporting of emissions has been a key engagement topic for us, through our Climate Impact Pledge, our Climate Action Strategy, and policy engagement. The Greenhouse Gas (GHG) Protocol’s Scope 2 guidance is undergoing its first revision since its publication in 2015.[2] We’re taking this opportunity to analyse challenges with using Scope 2 emissions reporting for investors under the existing framework, while offering an outlook under the GHG Protocol’s proposed new system.

Why do investors care about emissions reporting?

As an asset manager, we require accurate and consistent emission data from our investee companies to measure our own Scope 3 financed emissions[3]. Emissions reporting also helps investors understand three dimensions of companies’ interaction with the energy transition:

1. Exposure: Companies are exposed to transition-related risks and opportunities, for instance through carbon pricing. Emissions reporting allows us to improve our understanding of that exposure and manage it across our portfolios.

2. Impact: Companies’ activities can have positive or negative impacts on the energy transition by increasing or decreasing emissions in their own operations or their supply chains. Emissions reporting over time allows us to understand the way that impact is changing, hence assessing what transition outcome companies are aligning towards.

3. Incentives: Reporting on emissions can create incentives for companies to manage their carbon footprint and reduce emissions in the real world – they can only manage what they can measure.

Location- versus market-based accounting – two sides of the same coin

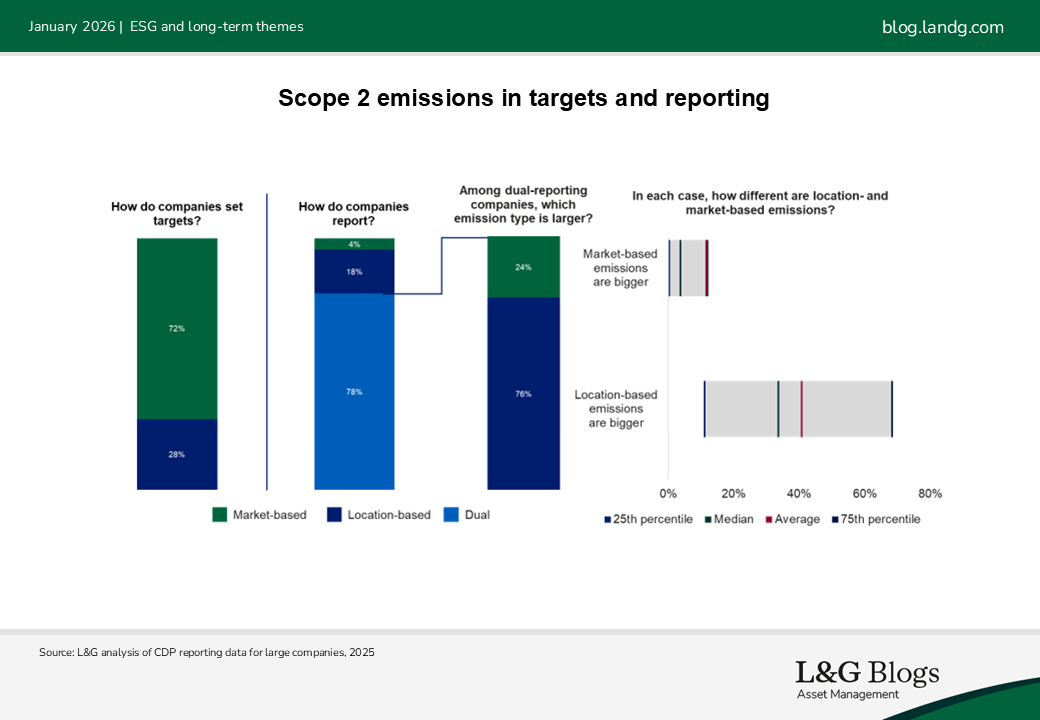

Companies are expected to report Scope 2 emissions using two methods – location-based and market-based accounting – under the GHG Protocol. Location-based emissions reflect the emissions intensity of the local electricity grid where energy is consumed, while market-based emissions reflect companies’ procurement decisions, meaning the contracts they sign with electricity suppliers to source electricity generation.

Metrics produced using these two methodologies do not provide the same information to investors. Nearly 80% of companies report both location- and market-based Scope 2 emissions, but 70% of companies with a Scope 2 target have set it using the market-based method.[4] This poses a challenge as the two methods can lead to different results. Among the 75% of companies which report higher location- than market-based emissions, location-based emissions are higher by 40% on average. Alternatively, among companies for which market-based is larger, the difference is only 11% on average, as shown in the chart below.[5]

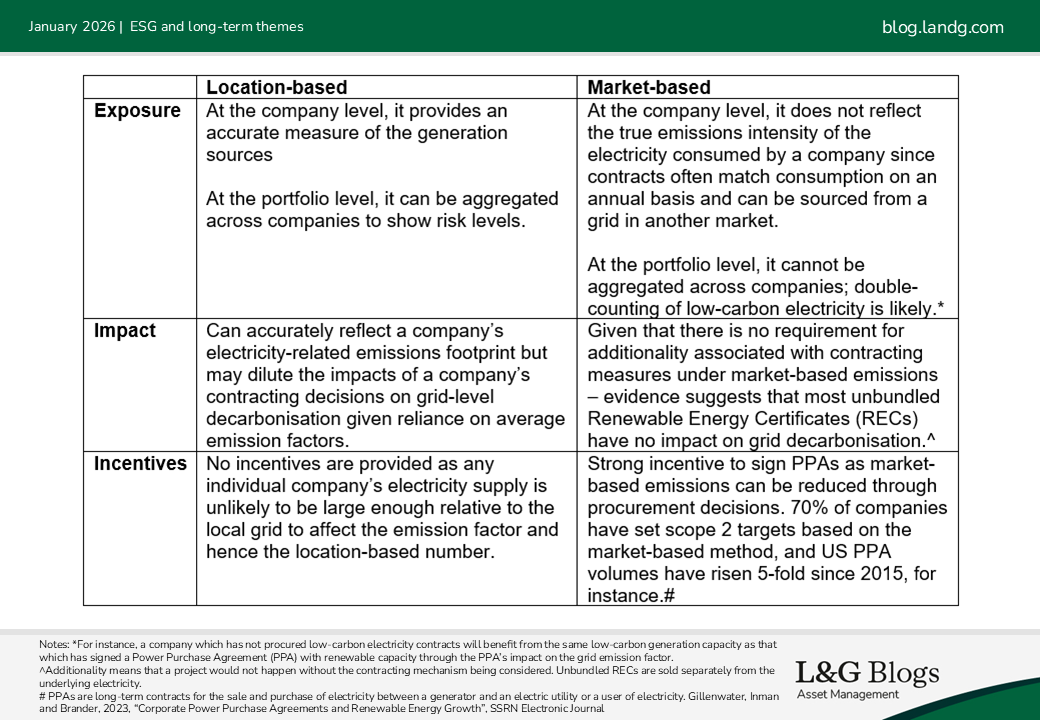

The below table outlines the performance of each measure against the three purposes of emissions reporting. In summary, market-based emissions pose challenges as measures of exposure and impact, but they do provide incentives which are lacking from the location-based measure.

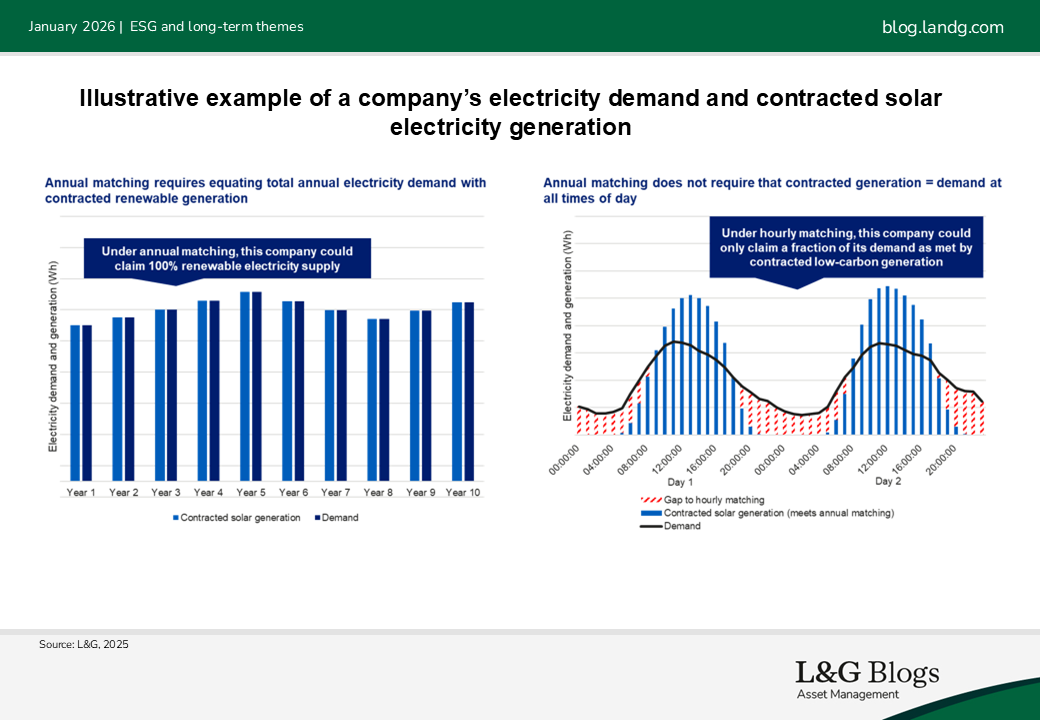

Hourly matching – Perfect data, imperfect outcomes

To address the aforementioned limitations of market-based Scope 2 accounting, the GHG protocol is considering updating guidance to require market-based instruments follow hourly, instead of annual, matching of electricity consumption to generation, as well as ensuring physical deliverability (see the chart below for an illustration for a hypothetical company).[6] Some companies, particularly in the tech sector, are already pursuing hourly matching strategies. Despite some potential advantages, our view is that hourly matching raises significant questions around emissions impacts and could have unintended consequences.

Pros

· Hourly matching of low-carbon electricity generation to consumption would mean Scope 2 reporting is a more realistic representation of companies’ actual footprint – hence making market-based measures a more accurate measure of exposure and impact, although market-based emissions would still be exposed to double-counting if added up across companies.

· While hourly matching does not resolve concerns around additionality, we believe it should incentivise companies to sign contracts with not only renewable electricity generation, but also assets which provide flexibility and dispatchable power to the grid, like utility-scale batteries. Flexible generation is essential to be able to meet demand across all hours. These technologies are critical to achieving low-carbon electricity grids, particularly as the penetration of variable renewables like solar and wind increases, but companies are not incentivised to support them in the current GHG Protocol guidance.

Cons

· Some companies pool consumption across locations or with other organisations to be able to reach commercial viability for a PPA. This would not be possible with hourly matching.[7] As a global investor, we are concerned this could disincentivise PPAs, particularly in regions with high grid emissions intensity. Since these need the most action, it could potentially lead to worse decarbonisation outcomes.

· Added administrative complexity and potentially significant additional cost of complying with hourly matching claims could further discourage uptake of decarbonisation targets.

Summary and implications for engagement

Decarbonising electricity and rigorous emissions accounting are critical to the energy transition. Both location-based and market-based Scope 2 emissions play different roles with varying impacts. Our guiding principle is that the emissions accounting rules should give companies fair credit for the actions they take to reduce emissions – either their own, or of the broader system. If the hourly Scope 2 rules incentivise corporates to procure low-carbon electricity in a way that more effectively supports grid decarbonisation, while reflecting a more accurate picture of their underlying exposure to risks and impacts on the grid, then the Protocol revision would be an effective tool in the next phase of the transition. However, the rule change could also have unintended consequences which need to be monitored – particularly if greater complexity leads to a decline in incentives for corporate action in some countries. We encourage companies to participate in the Protocol consultation process, and we will continue to closely follow updates to the guidance and to support measures which encourage real-world decarbonisation.

[1] IEA Electricity Statistics, 2025

[2] https://ghgprotocol.org/blog/upcoming-scope-2-public-consultation-overview-revisions

[3] For our previous research paper on the topic of Scope 3 emissions, please see here: LGIM Scope 3 Omission impossible

[4] L&G analysis of CDP reporting data for large companies, 2025

[5] L&G analysis of CDP reporting data for large companies, 2025.

[6] Physical deliverability means the project has to be connected to the same electricity network as the user of electricity. GHG Protocol Public Consultations | GHG Protocol

[7] https://www.mckinsey.com/industries/electric-power-and-natural-gas/our-insights/rethinking-your-companys-clean-power-strategy

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.