Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

The American consumer’s hidden cracks

Conventional wisdom says the US consumer is fine. A closer look at the data suggests the foundations may be quietly shifting.

Key takeaways:

|

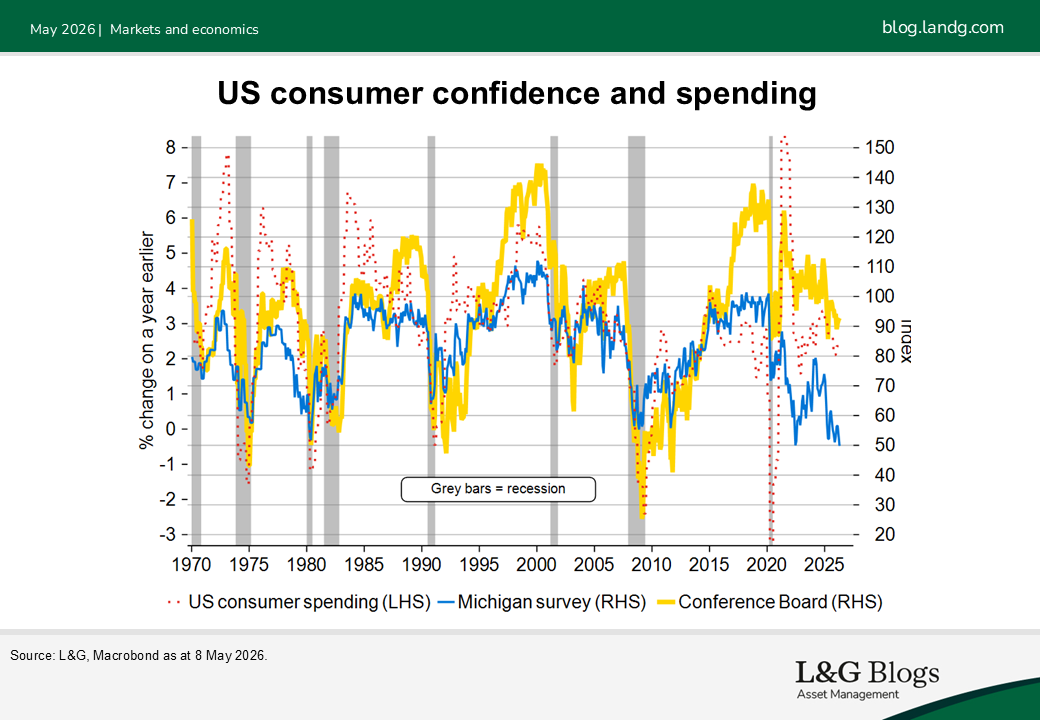

Since Covid, the US consumer has proven remarkably reliable and has powered the US economy through a series of shocks including a stagnant manufacturing sector, surging interest rates and geopolitical crises. Quarter after quarter, households keep spending.

The current consensus narrative has settled on the ‘K-shaped economy’: diverging fortunes between income groups; but overall consumer spending growth holding near 2% for the foreseeable future. The macro backdrop is supportive with a stable labour market, tax cuts, rising equity prices and easy access to credit. Corporate earnings have reinforced this view, with companies across sectors reporting a resilient consumer.

Consensus has tended to dismiss the signal from consumer sentiment due to the political bias in answering the survey.

A deeper decomposition of the income drivers behind consumer spending tells a more complicated story. And if those drivers are deteriorating — quietly, gradually, beneath the surface — the resilience narrative may have a shorter shelf life than markets are pricing.

What actually drives spending?

Most analysis of the consumer looks at aggregate real income growth. That approach masks a great deal. Break down income by source, and the coefficients on consumer spending diverge sharply.

Employment growth: ~1.0×

Dominant driver. One-to-one relationship with real consumer spending

Wages and salaries per employee: ~0.5×

Meaningful, but half the impact of headcount growth

Inflation: ~0.5×

Negative drag as elevated; potential easing later in year offers partial relief

Non-labour income: ~0.1×

Interest, dividends, rental income, transfer payments — far less important than assumed

The implications are significant and employment growth is the linchpin. Payroll growth has slowed materially in recent quarters, partly a consequence of curbs on immigration. With the ‘breakeven’ pace of job creation now estimated somewhere between zero and +50k per month (versus triple digit prior cycle norms), the structural tailwind from headcount expansion has largely gone.

Consumer spending rarely contracts outright — it has happened on a year-over-year basis only four times since 1960. But that resilience can mask a slow deterioration in the underlying fundamentals.

The wealth effect isn't what it was

One of the more striking findings concerns the wealth effect. Equity markets have performed well, and the conventional assumption is that rising stock prices boost consumer confidence and discretionary spending. The data suggests otherwise — at least at the margin.

Depending on the model specification, the wealth effect from housing could be as much as five times larger than from equities.. And US real house prices have been falling. With significant overvaluation, excess inventories, and new home build rates running above equilibrium — a situation exacerbated by near-zero net immigration and deteriorating demographics — the housing outlook is poor. The wealth effect, once a tailwind, has turned marginally negative.

5× HOUSING VS EQUITY WEALTH EFFECT

6%+ NEW MORTGAGE RATES ERODING BUDGETS

0–50k MONTHLY PAYROLL BREAKEVEN (NEW NORMAL)

The frozen housing market operates through two further channels. Declining home sales suppress demand for household goods and furnishings — a quiet but persistent drag on retail. And the historic gap between new mortgage rates (north of 6%) and the rates on legacy mortgages means that as older, cheaper loans are gradually retired and replaced, mortgage payments as a share of income creep inexorably higher. Neither channel makes headlines, but both compound over time.

The inflation wildcard — and the saving rate problem

Tariffs are adding to inflationary pressure. The short-run effect should fade, assuming no further escalation beyond existing measures — but there are upside inflation risks. Energy shocks can feed through in unpredictable ways, and surging memory chip prices are already starting to show up in electronic goods. Even if oil follows futures curves lower later in the year, headline inflation is likely to rise an extra 1% relative to pre-crisis levels, before it eases.

Tax refunds may be providing a temporary cushion, potentially flattering the income data and masking the real squeeze on household budgets from tariffs and higher gasoline prices.

The saving rate compounds the picture. Already low by historical standards, it leaves households with a limited buffer to absorb shocks. This is not a crisis signal on its own, but it narrows the margin for error.

Several factors could materially improve the outlook:

- Income data is heavily revised. A significant upward revision to wages and salaries could close the gap between model and reality — and simultaneously raise the saving rate, converting a headwind into neutral territory.

- AI capital expenditure is large, but its employment multiplier remains uncertain. If capex spending broadens into more labour-intensive activities, payroll growth could surprise to the upside.

- The relationship between employment and consumption is contemporaneous and self-reinforcing. A positive payroll surprise can beget a spending surprise, which in turn supports sentiment and hiring.

- Any durable resolution to geopolitical tensions could see energy prices fall faster than futures currently imply, taking inflation with them and restoring some real income headroom.

The bottom line

The consensus view of a resilient US consumer is not wrong — it just may be late. Consumer spending is famously difficult to derail; the historical record confirms this. But now the structural supports are beginning to falter.

Employment growth is slowing. Real house prices are falling. Mortgage costs are rising. Tax cuts are fading. The saving cushion is thin. Inflation is set to tick higher before it eases. None of these individually is disqualifying. Together, they suggest the near-2% spending growth the consensus has pencilled in for coming quarters faces meaningful downside risk — even without a major exogenous shock.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.