Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

A benign year runs into an energy reality check

Higher energy prices have unsettled what looked like a calm year for growth and inflation and this is proving difficult for central banks to ignore.

The following is an extract from our Q2 2026 Asset Allocation outlook.

Ahead of the conflict in the Middle East, consensus was expecting a benign year with growth around potential across most regions and inflation at or returning towards target. The surge in energy prices has thrown these forecasts into disarray. However, there is a reluctance to get pinned down with fresh views given the uncertainty around how the conflict evolves and the path for energy prices.

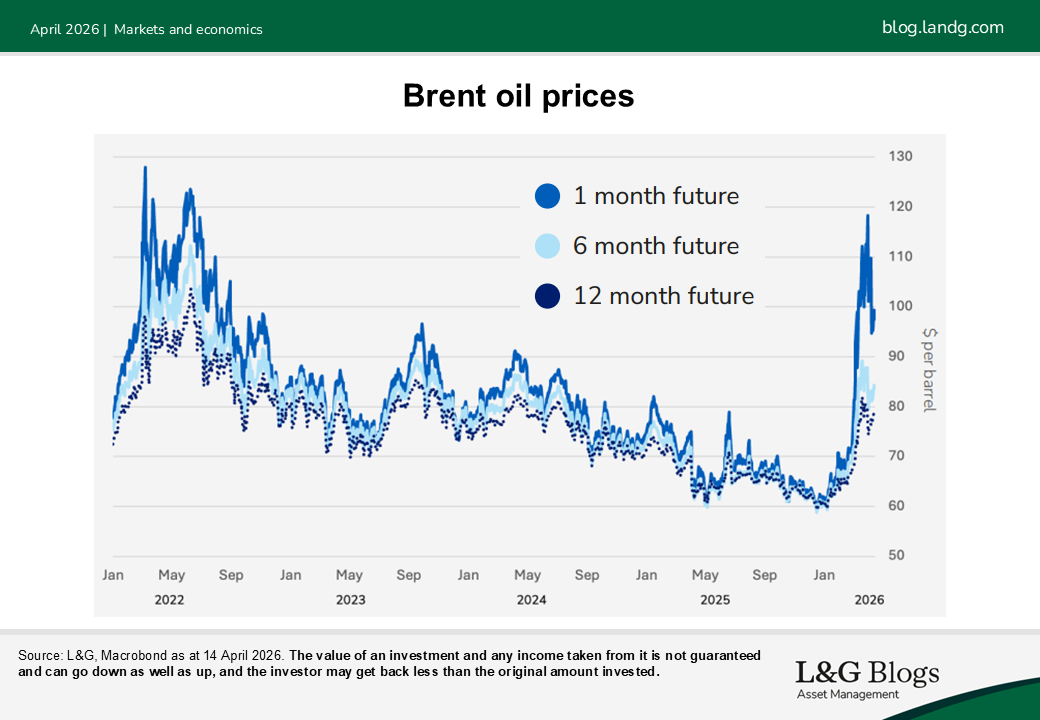

There has been tremendous volatility in oil prices. Developments are now hostage to both the extent energy infrastructure in the region suffers further damage and the speed oil is allowed to flow again through the Strait of Hormuz. But for now, oil prices seem unlikely to quickly return to pre-conflict levels.

The impact on inflation

The first round effect on inflation is relatively simple to calculate. If Brent crude oil is around $100 a barrel, this should add just over 1% to UK and euro area headline inflation.

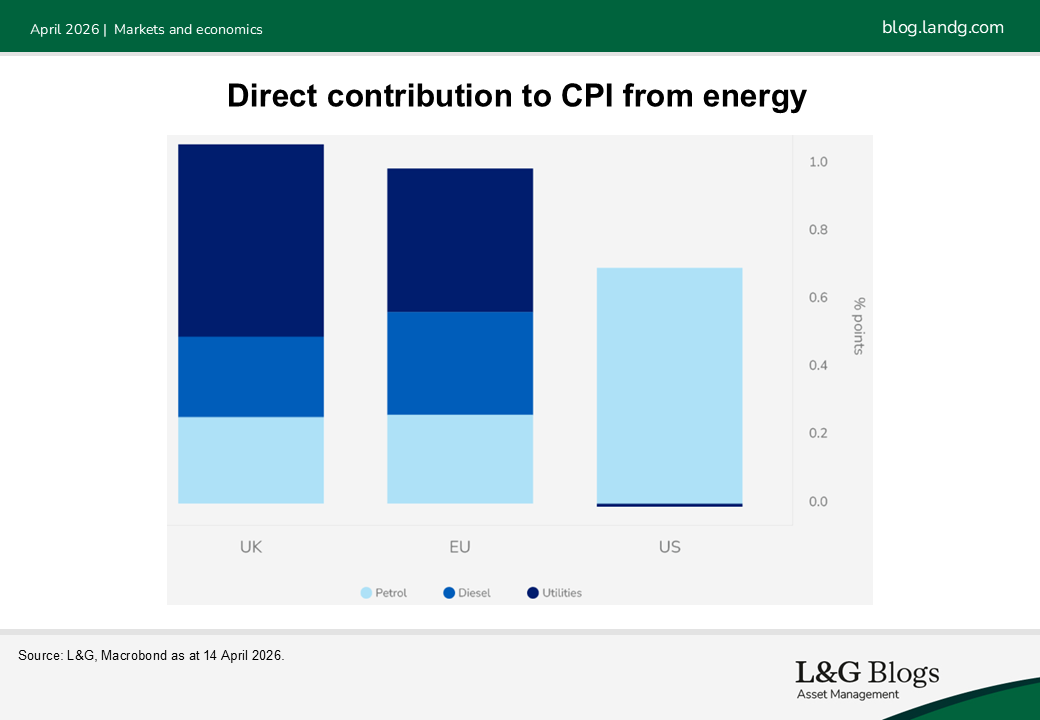

Energy shocks passthrough at different speeds. Petrol pump prices adjust quickly, and in the very near-term, the US is suffering the most from a surge in gasoline prices. However, utility bills should be unaffected as the US has an abundance of natural gas that cannot be exported and hence remains low in price.

Gas utility bills will likely rise across Europe, but the link between electricity and gas prices is much stronger and quicker in the UK than in the EU. Most UK consumer utility bills reset every three months, so this change would show up in July CPI, without offsetting government intervention. Germany and France have longer lags.

We are concerned consensus could be underestimating the overall inflation impact. Rather than just commodities, flows through the Strait of Hormuz also include finished products such as diesel, jet fuel, fertilizers and even helium, which is used to cool semiconductors. Global memory prices have already surged by 1% of GDP on the AI investment boom[1]. This cost shock could raise broader goods prices.

Growth concerns

The rise in energy prices has led to a tightening in financial conditions, especially in Europe where markets have been pricing in varying amounts of rate hikes.

We think hiking rates more than a token amount to maintain inflation fighting credibility will ultimately prove to be a policy mistake. There is concern about a repeat of 2022, where inflation expectations and wages rose in response to the supply shocks and central banks scrambled to raise rates to bring inflation back under control.

The crucial difference in 2022 was incredibly strong demand aided by a huge policy stimulus and post COVID-19 pent up spending. Employment growth was rapid and firms were forced to raise wages amid a shortage of workers. Today, labour markets are much weaker. Hiring has stalled and job openings have fallen sharply. We think workers will be more concerned about keeping their jobs than securing wage hikes. On the basis that energy prices remain elevated, the risk is higher inflation squeezes real incomes and consumer spending, and growth disappoints.

Amid all the uncertainty, the response of consumers and businesses to the shock will require careful monitoring. There could be some initial stock building given supply disruption fears, followed by a more pronounced dip in activity if the shock seems more persistent. We will also be watching for any signs of second round effects on wages in surveys and pay deals as that would get the attention of central banks and make rate hikes more likely.

The above is an extract from our Q2 2026 Asset Allocation outlook.

[1] Source: L&G, Bloomberg as at 24 March 2026

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.