Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

UK Single Family Rental: balancing fundamentals and market timing

In this blog, we explore the Single Family sector’s underlying fundamentals and investment characteristics, as well as how current market timing is potentially impacting the sector.

The state of the UK Living market

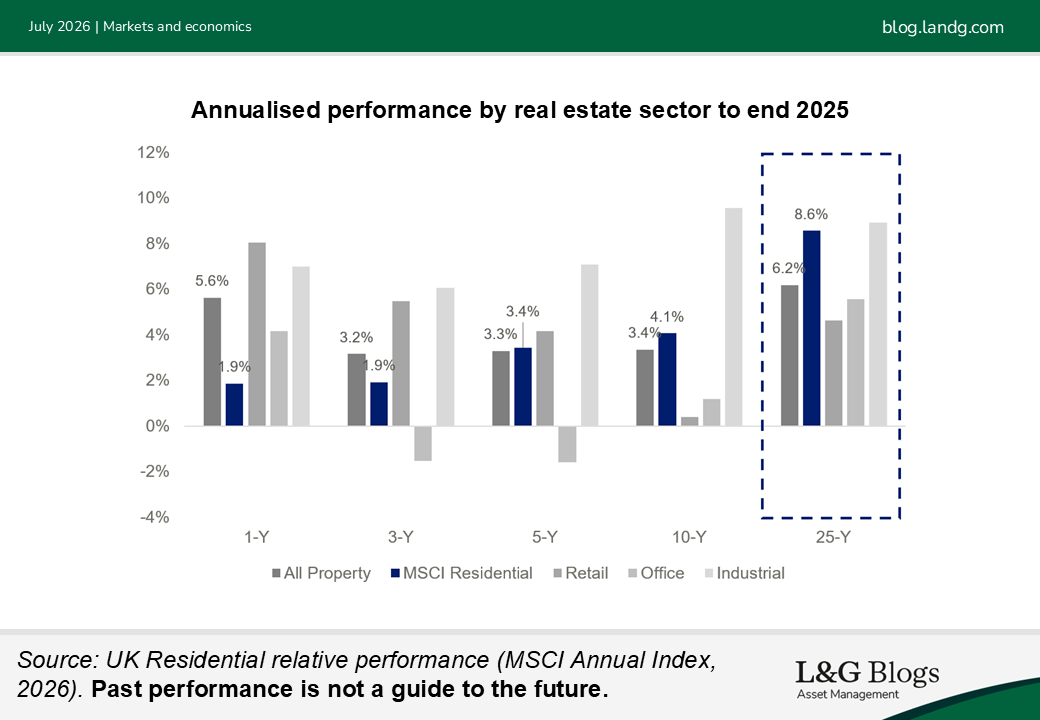

UK Living real estate performance has traditionally been characterised by its more stable returns profile relative to commercial sectors, underpinned by inflation-beating rental growth and resilient occupancy through the cycle.

While Residential was more resilient than commercial real estate during the 2022 correction in UK property values, recent performance has lagged, with rental growth impacted by pandemic-related swings in demand and regulatory costs directly affecting capital values.[1] The combination of moderating rental growth and relatively tight yields has contributed to a squeezed risk premium for the sector, resulting in a slowdown in performance relative to commercial sectors.

While recent performance has lagged, the long-term relative performance of Residential has been strong, underpinned by households renting for longer and persistent under-supply.

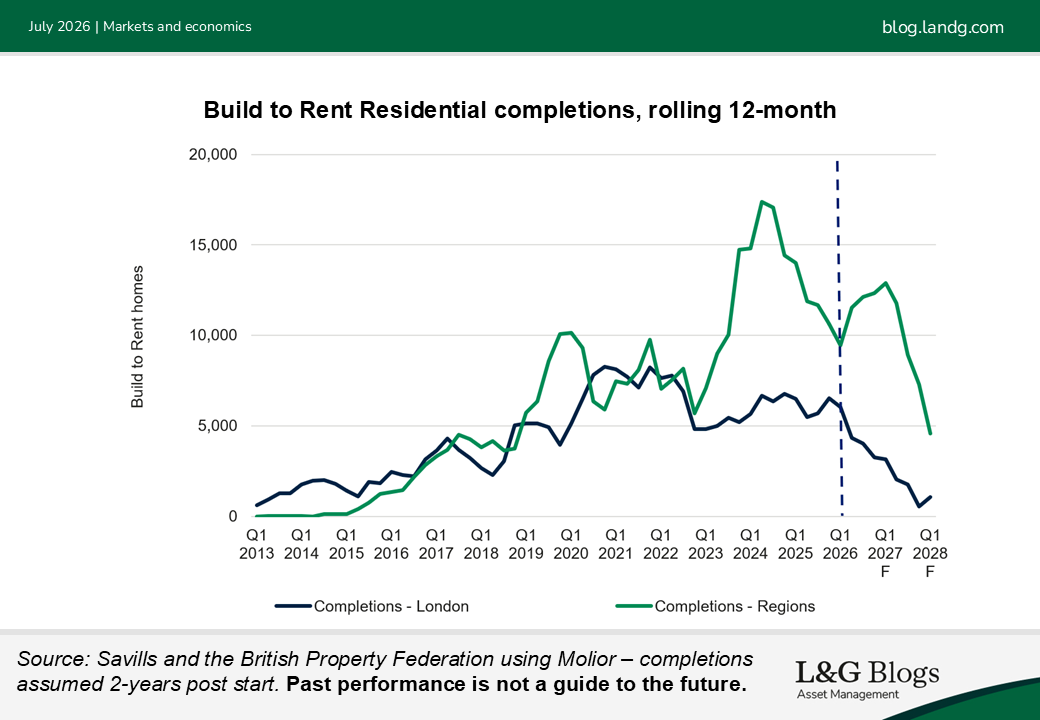

A challenging development environment, which is likely to result in a sharp decline in Build to Rent completions post H2 2027, combined with persistent pressure on Buy-to-Let landlords, has exacerbated existing supply constraints in the sector. When combined with resilient demand, we believe the fundamentals of the sector remain intact.

In our view, near-term pricing pressure should be balanced against the enduring strength of the long-term fundamentals of the UK Living sector. We believe this may present opportunities for new capital looking to access the sector at an attractive entry point.

Single Family Rental: Fundamentals and investment characteristics

The investment opportunity set in UK Living is broadening. This may enable investors to allocate across segments and investment styles according to their tolerance for different risks – including development risk, liquidity, operational complexity, political intervention and desired social impact.

Within UK Living, Single Family Rental[2] has gained traction. Investors have been attracted by its lower operational intensity and capex demands, broadly stable resident base, smaller lot sizes and a more streamlined development process in the Building Safety Act[3] era. Single Family has grown from 9% of UK Build to Rent transaction volumes in 2022 to 55% in 2025.[4]

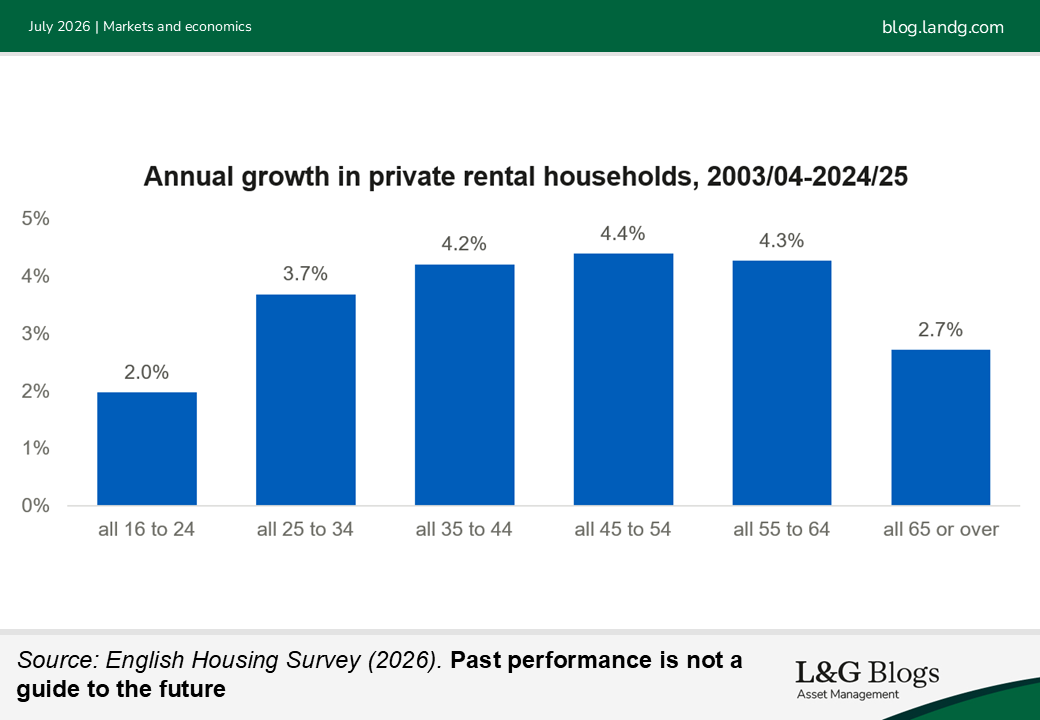

We believe increased activity in the segment is underpinned by resilient fundamentals. In recent years, the growth in demand for private rental housing has been strongest among middle-aged households and families, which remains the core demographic for Single Family housing.

Barriers to homeownership in the form of first-time buyer deposits and mortgage costs remain sizeable, particularly given the step higher in interest rates over 2026[5], with the age of first-time buyers increasing as a result.

While we expect homeownership to remain the preferred tenure for many UK households, we believe the financial rationale for homeownership is less compelling than in the past. Lower house price growth expectations, combined with higher interest rates and longer mortgage terms, means homeowners are building less equity in their homes. This in turn increases the ‘opportunity cost’ of tying up significant capital in homeownership via deposits and moving costs.

Meanwhile the Renters’ Rights Act provides greater security of tenure for renters. As a result, we think more prospective homeowners may make the intentional choice to delay entry into homeownership and skip a step on the traditional ‘housing ladder’.

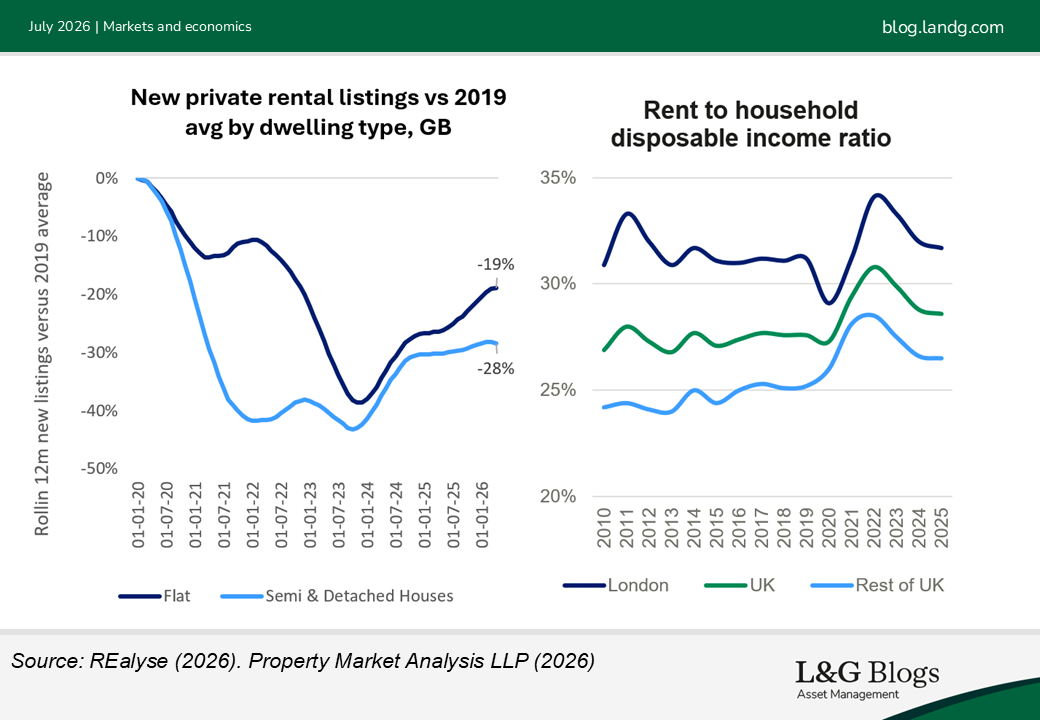

The case for Single Family is underpinned by tight supply, with rental listings remaining significantly behind pre-COVID-19 levels and improving affordability. On average, private renters in suburban locations spend 26% of their gross household income on rent versus 30% in urban areas.[6]

Operating model

Living is an operationally intensive asset class. We view scale as an increasingly important differentiator, with larger platforms able to benefit from economies of scale via investment in technology, operations and data.

We note a relative lack of stabilised Single Family stock in the UK to date. However, standing stock in the UK, alongside data from more mature Single Family markets in the US and Netherlands highlights more stable occupancy and lower running operational expenditure associated with Single Family, with gross-to-nets[7] typically sitting closer to 20%. This compares to 25-30% in Multifamily, 25-35% in Purpose-Build Student Accommodation and 30% plus in Co-living. Lower running costs are driven by less complex M&E, alongside fewer communal areas and amenities. Single Family capital values are more closely aligned with the for-sale market, providing added liquidity optionality on exit and, in theory, value stability.

Given a macro environment increasingly characterised by periodic bouts of higher inflation, we see the lower exposure to operational and capital expenditure of Single Family as beneficial. When combined with the above-inflation rental growth historically delivered by UK residential, we believe the segment has the potential to provide greater resilience in higher inflation environments.

Market timing

The primary method of accessing the Single Family Rental sector is through forward funding schemes with housebuilders, alongside a limited but growing pool of stabilised stock. The price at which investors can fund schemes relative to their for-sale value is an important driver of returns.

Recent increases in mortgage rates have exacerbated pressure on the for-sale market. A relatively slow for-sale market, combined with expectations of rental growth outstripping house price inflation in the near-term, often makes Single Family Rental bidders more price competitive with housebuilders. This can allow Single Family investors to deploy into the sector at a discount to open market sales values, while in turn allowing housebuilders to de-risk prospective schemes despite a lacklustre sales market. As housebuilders continue to recycle capital into new projects, the overall delivery of new homes across tenures is supported, with SFR an increasingly important component of the tenure mix.

Risks and the role of SFR within a diversified UK Living portfolio

The primary risk facing the Living sector, in our view, is around yields. Single Family yields have remained stable over 2026. While we would anticipate some modest upwards pressure on yields across UK real estate, we expect the lower cost base and more liquid lot sizes of Single Family to provide greater insulation.

Despite some concerns over political instability, we retain the view that the growing role of institutional investors in delivering new housing in the UK will persist. The example of Scotland is instructive; Scotland saw annual additions to the BTR pipeline fall from 3,334 in 2022 to 568 in 2025 following the temporary introduction of rent controls in 2022.[8] As a result, the Scottish Government recently made Build to Rent and Mid Market Rent exempt from future rent controls.

Conclusion

Single Family Residential is not immune to higher rates, policy risk or execution challenges. We expect a combination of structural demand, constrained supply, lower operational intensity, and a favourable funding environment to support stronger performance from the Single Family sector over the medium- and longer-term relative to the ‘All Property’ average. We believe the segment can form a meaningful component of a larger, more diversified exposure across Living sectors within broader real estate allocations.

[1] Multiple Dwellings Relief (MDR), a Stamp Duty Land Tax (SDLT) relief for purchases of more than one dwelling, was abolished for transactions completing on or after 1 June 2024

[2] MSCI defines Single Family Build to Rent as detached, semi-detached and terraced houses / bungalows residential properties with a construction year after 2010 and having at least 30* units and not being ground rent, student, social or affordable housing

[3] The Building Safety Act (2022) was introduced to improve fire safety and construction quality for high-rise buildings.

[4] Knight Frank (2026). Build to Rent investment encompasses Single Family, Multifamily and Co-living.

[5] This is reflected in the RICS residential survey’s net balance of new buyer enquiries falling from -15% in January to -34% in May 2026.

[6] ONS, 2025

[7] ‘Gross-to-net’’ refers to operating costs as a proportion of gross rental income.

[8] Source: Rettie (2026)

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.