Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Private credit: Pockets of resilience

Why investment-grade private credit and asset-backed finance stand out in today’s tougher landscape.

The challenges in sub-investment grade direct lending have been well telegraphed during the first half of 2026 and are likely to continue to dominate headlines for the rest of the year.

The wider macroeconomic backdrop may weigh on high-level private credit performance. In this environment, it’s likely investors will seek to bolster portfolio resilience. We also see more constructive dynamics across resilient areas of private credit that we believe merit closer attention.

Investment-grade (IG) private credit and asset-backed finance (ABF) stand out as areas of greater potential resilience. We see both benefiting from stronger underlying credit quality, while ABF can also offer diversification* away from traditional corporate drivers.

Making the grade

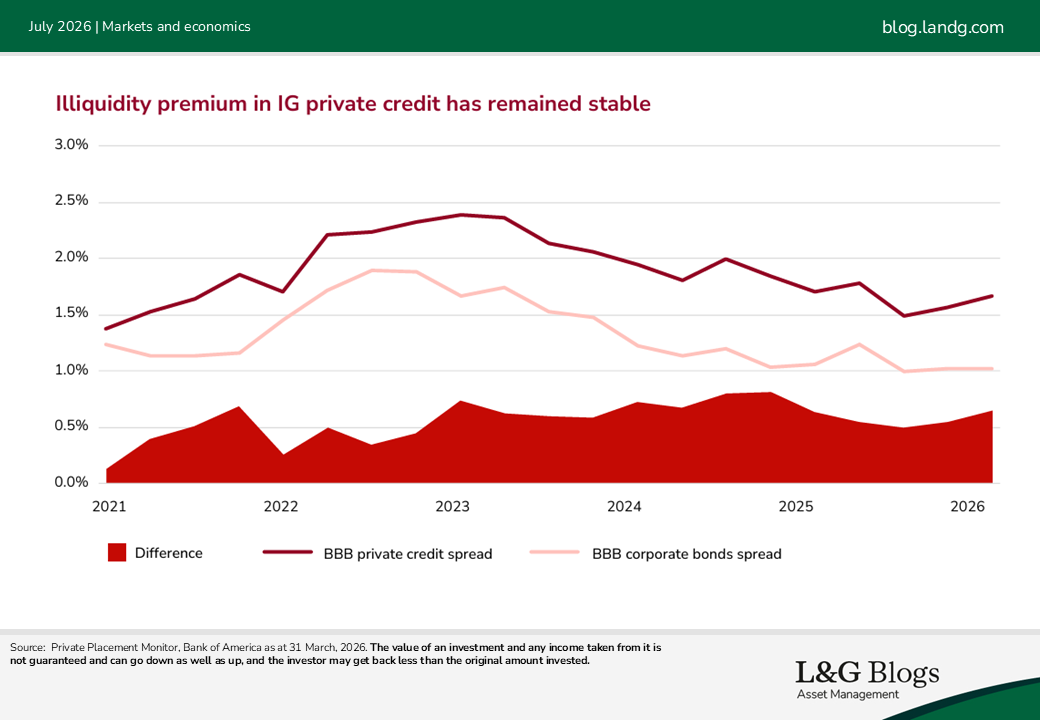

IG private credit has proven notably robust through bouts of geopolitical volatility, including the recent conflict in the Middle East. Activity has remained healthy, with Q1 2026 transaction volumes in private placements – one of the core segments of the IG market – running more than 30% higher year-on-year[1].

Importantly, yields remain above long-term averages, supported by elevated base rates. We believe this combination of income and credit quality will continue to underpin the asset class’s appeal.

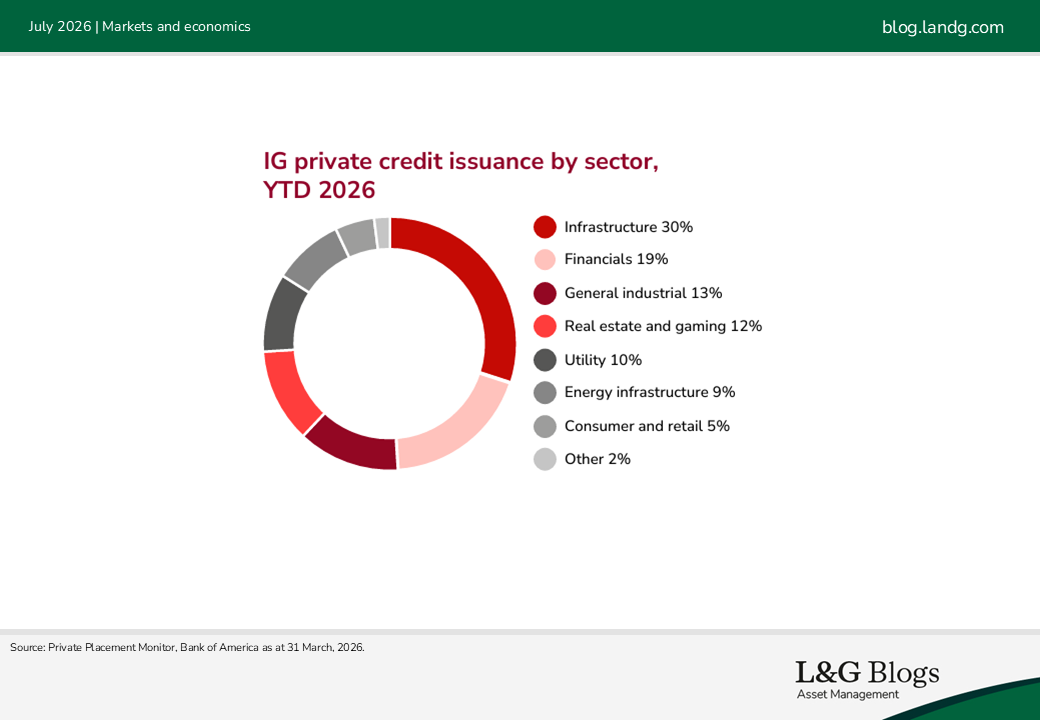

Sector activity has been most pronounced across infrastructure, industrials and financials. Within this, we believe digital infrastructure financing is an increasingly important theme. This has largely played out in the public credit market so far, but private credit is seeing growing supply across project finance, construction finance and specialist areas, such as GPU financing. Data centres form a significant share of this demand, alongside the fibre networks that connect users, data facilities and cloud computing infrastructure.

While larger national operators still dominate, we have observed a clear increase in financing opportunities for regional platforms, many of which are benefiting from structural growth in data consumption alongside the AI-driven expansion in compute demand.

ABF attributes

Asset-based finance is an area of alternative credit that we view as an increasingly important and evolving segment of the private credit universe. It’s characterised by lending secured against often diversified pools of assets, receivables or contractual payment streams.

While definitions vary across the market, ABF is commonly understood as spanning both public and private credit markets, bridging traditional securitised assets and privately originated opportunities.

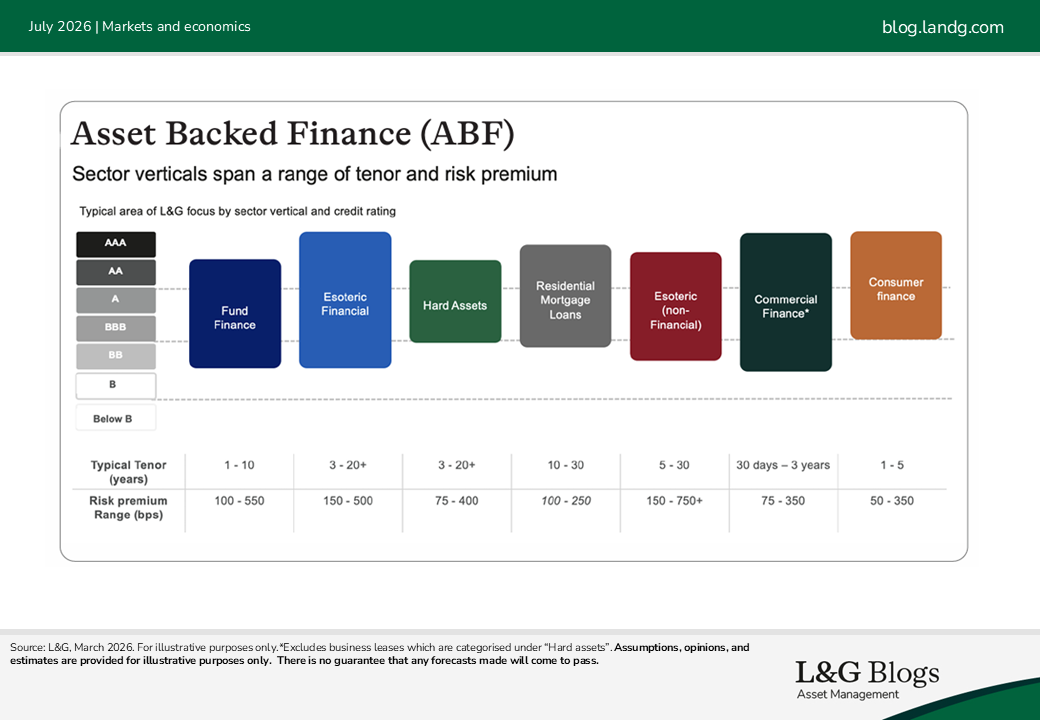

We believe it is possible to adopt a broad and pragmatic definition of private ABF. This involves segmenting the opportunity set into fund finance, hard assets, consumer finance, commercial finance, residential mortgages, and esoteric strategies (both financial and non-financial). We see this as a framework that reflects the diversity of underlying collateral, risk drivers and structuring approaches across the asset class.

In today’s environment, we believe ABF may offer a compelling combination of attributes for investors. It can deliver enhanced returns through illiquidity and complexity premia, with the potential to mitigate downside risk through asset-backed structures, amortising cash flows and lender friendly terms.

One factor we see as particularly important is that ABF returns are less directly linked to corporate balance sheets, potentially offering diversification benefits relative to traditional credit.

The chart below shows the considerable span of tenor and risk premium across each of the sub-sectors we identify.

Within this universe, we are particularly attracted by fund finance and certain esoteric opportunities, such as emerging market debt.

Assessing BDC risks

Fund finance is one area that received attention in H1, with focus on business development companies (BDCs) and their potential vulnerabilities given exposure to US software companies.

However, it is worth noting there is a range of risk across BDCs as well as the broader sector. For instance, one of the most attractive parts of the fund finance market, in our view, is capital call facilities – short-term lending to private market funds, secured on LP commitments. These are typically AA / A rated and, with tenors of less than a year, could well be an attractive addition to investors’ liquidity toolkits.

Elsewhere, in esoteric finance, private emerging market debt offers the potential for both insured and structured opportunities, often supported by multilateral development banks or Development Finance Institutions. These may offer compelling risk-adjusted returns with strong credit enhancement while mobilising capital for positive outcomes.

Strategies and segments

In conclusion, the headlines surrounding direct lending are unlikely to go away during the second half of the year. However, we stress that private credit, like any asset class, covers a range of strategies and segments.

Selectivity remains key, but there are areas of resilience which we believe may offer investors many attractive attributes.

*It should be noted that diversification is no guarantee against a loss in a declining market.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass. Past performance is not a guide to the future.

[1] Private Placement Monitor, as of April 2026

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.