Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Affordable Housing: a bright spot for UK housebuilding

Greater regulatory certainty and funding for Affordable Housing can provide a much-needed boost for UK housing delivery.

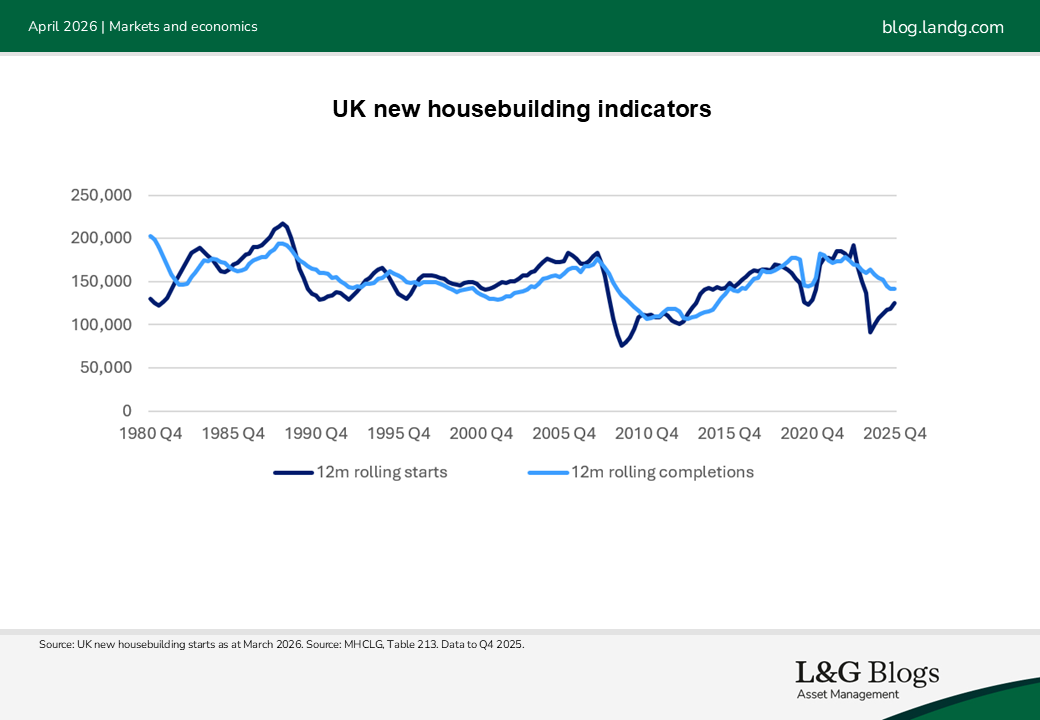

The UK government’s long-stated and enduring ambition to deliver 300,000 new homes per annum in England faces many macro-economic and regulatory headwinds.

For the most recent full year, net additional dwellings in England totalled 208,600[1], a -6% decline on the prior year. With new starts weak over 2025, and viability challenges likely, in our view, to be further exacerbated by renewed inflationary and cost of capital pressures, we anticipate that the imbalance between supply and demand in UK housing is likely to get worse before it gets better.

Addressing the need

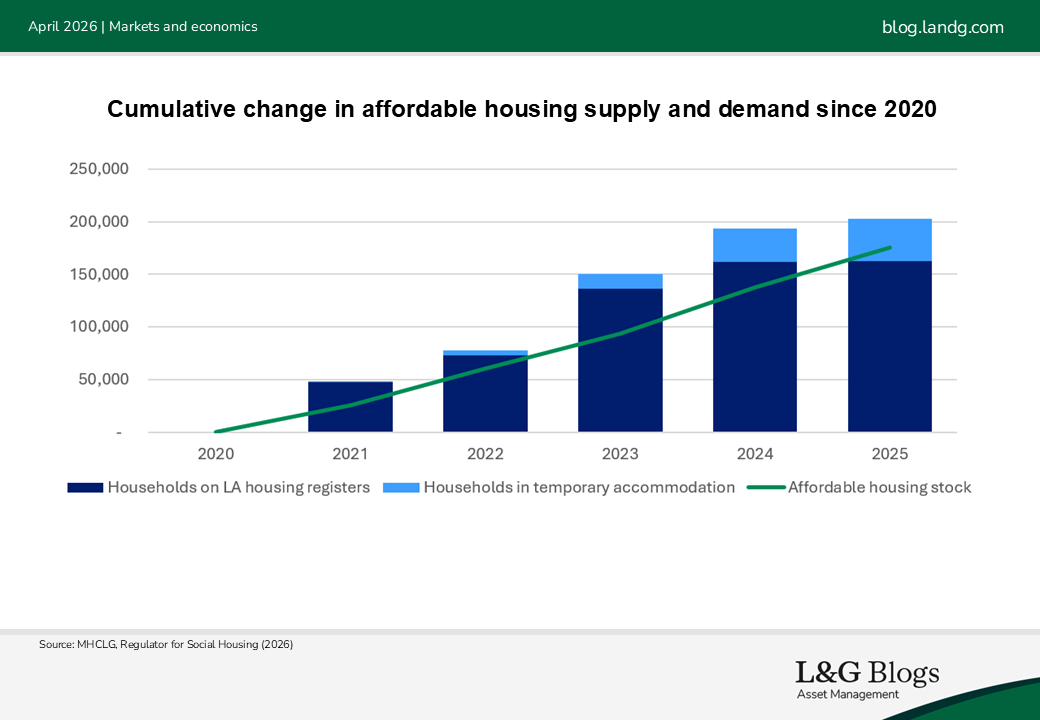

A weakening in housebuilding comes at a time when the under-supply of Affordable Housing is particularly acute. As of 2025, the number of households on Local Authority housing registers (i.e., waiting lists) was at its highest level since 2014. Households in temporary accommodation have also reached record highs. In short, the need for Affordable Housing is outpacing delivery.

A worsening structural shortage of adequate Affordable Housing not only multiplies the social and wellbeing challenges for those individuals living in unsuitable accommodation, but also adds to pressure on the public purse, with local government liable for a projected 65% increase in temporary accommodation costs to nearly £4 billion by the end of the decade[2].

This imbalance is particularly acute in London. The capital accounts for 25.5% of households on Local Authority housing registers and 56% of households in temporary accommodation[3], its highest share on record. Affordable Housing starts in London totalled 4,522 for FY2024-2025, -66% behind the 10-year average of 13,334 and representing just 11% of the GLA’s estimate for London’s Affordable Housing need[4].

A silver lining

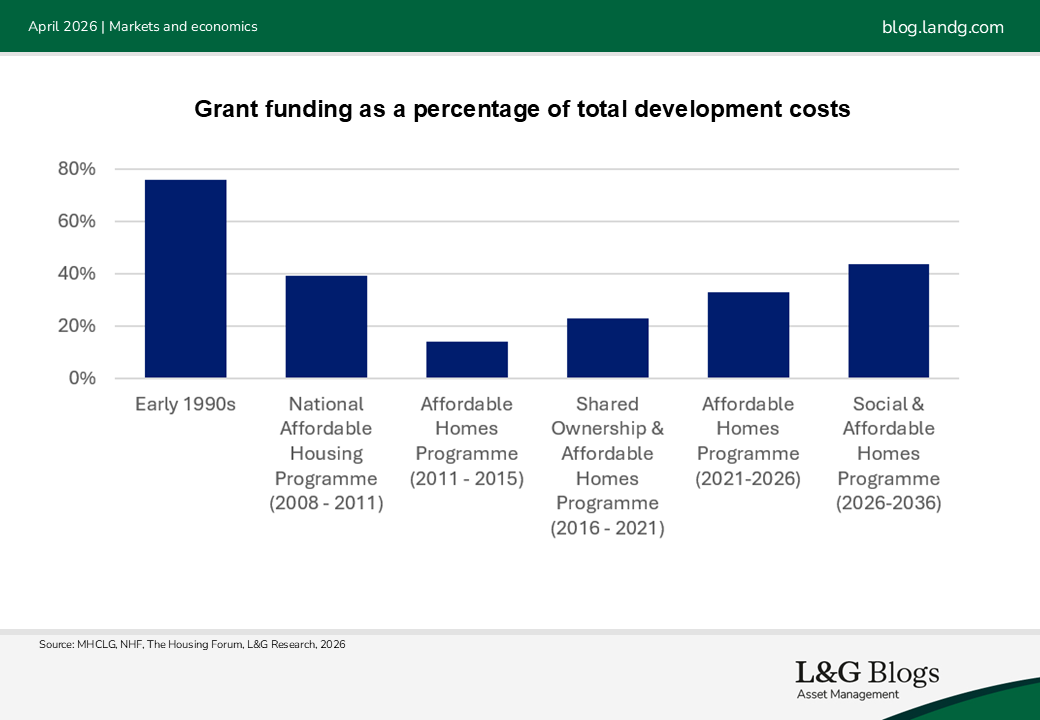

The launch of the UK Government’s Social and Affordable Homes Programme (SAHP) in April 2026, combined with the 10-year Affordable rent settlement announced in 2025[5] does, however, provide scope for renewed optimism for UK housebuilding. The SAHP, which provides £39 billion of funding targeting 300,000 new homes over a 10-year period, represents a material uplift in the funding environment, with the launch of the UK’s National Housing Bank in March providing added firepower. We believe this represents the healthiest grant environment since pre-2008[6].

Yet, a strengthened grant environment and improved regulatory clarity is only part of the solution. Building the capacity of Registered Providers to scale up delivery is critical. Many Registered Providers’ capacity continues to be hindered by shrinking EBITDA MRI[7] margins and the capital expenditure demands of upgrading existing stock to meet more stringent environmental and building quality and safety regulations.

The latest Regulator of Social Housing’s financial forecast of private Registered Providers highlights the lack of existing capacity to increase delivery, with forecast development declining from 333,000 units in 2023-2028 to 274,000 over 2025-2030. A limited number of Registered Providers bidding on Section 106[8] delivery has further weighed on broader private sector delivery.

Building the capacity of the Affordable Housing sector to develop consented schemes is therefore, in our view, fundamental to unlocking housing delivery across all tenures.

The next phase of Affordable Housing delivery

We believe new and larger sources of capital are required to increase development and unlock Section 106 delivery. While for-profit registered providers currently own 1.0% of Affordable Housing stock, their ownership has grown five-fold from under 9,313 in 2020 to over 46,555 in 2025. We expect the Mansion House Accord and LGPS consolidation to provider further tailwinds for increased institutional investment into the sector.

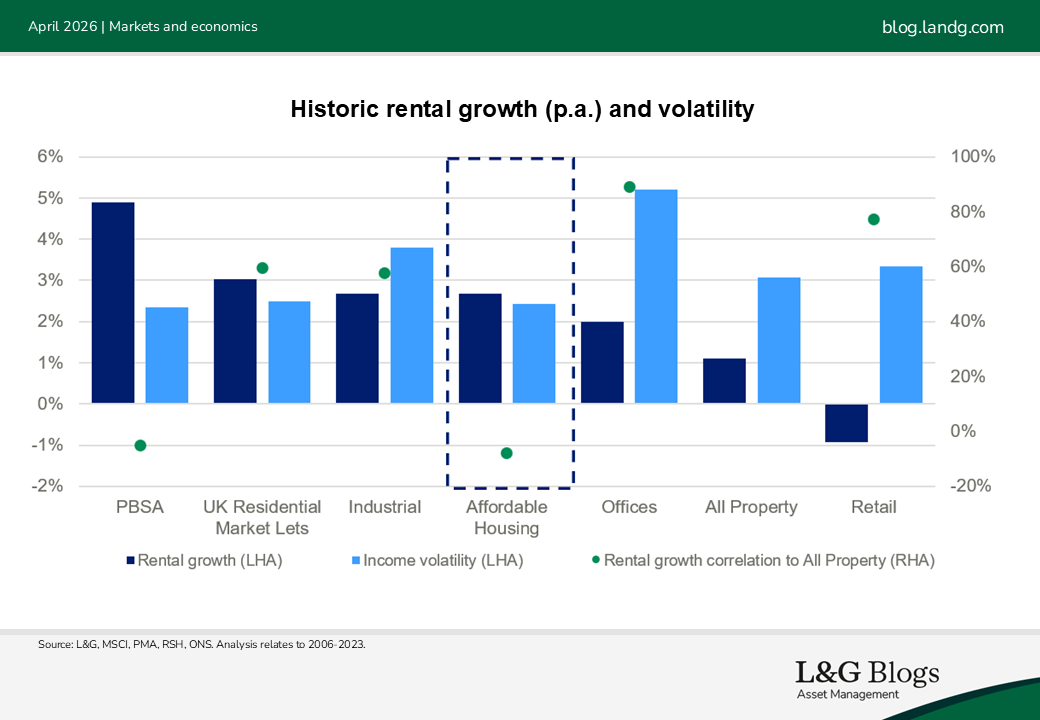

From an investment returns viewpoint, our view is that Affordable Housing may offer comparatively stable, inflation-linked returns alongside positive social impact. A resurgence in volatility and inflation expectations over recent times only serves to highlight the potential attractiveness of defensive, asset-backed cashflows with embedded inflation linkage. In addition, rental growth historically delivered by the Affordable Housing sector has been less volatile than the All Property average and has been negatively correlated to it, highlighting the inherent diversification benefits provided by the sector.

We believe the sector remains well positioned, particularly on a risk-adjusted basis, relative to other UK real estate sectors. Amid a turbulent macro environment, PMA’s March 2026 forecasts for UK real estate indicated potential returns of c.6% p.a. over 2026-2030 across All Property within the UK; we estimate the Affordable Housing sector is positioned to deliver c.7% p.a. over this period, underpinned by resilient rental growth and notwithstanding the conservative assumption that yields remain flat over the horizon.

Risks

We believe the primary risk for investment into the Affordable Housing sector is political intervention. In our view, this risk is partially mitigated by three factors:

1. The sheer scale of need for Affordable Housing, which is likely to get worse before it gets better

2. The UK government’s continued explicit desire to crowd in private capital into housing delivery, alongside the financial constraints experienced by central and local government and many Registered Providers

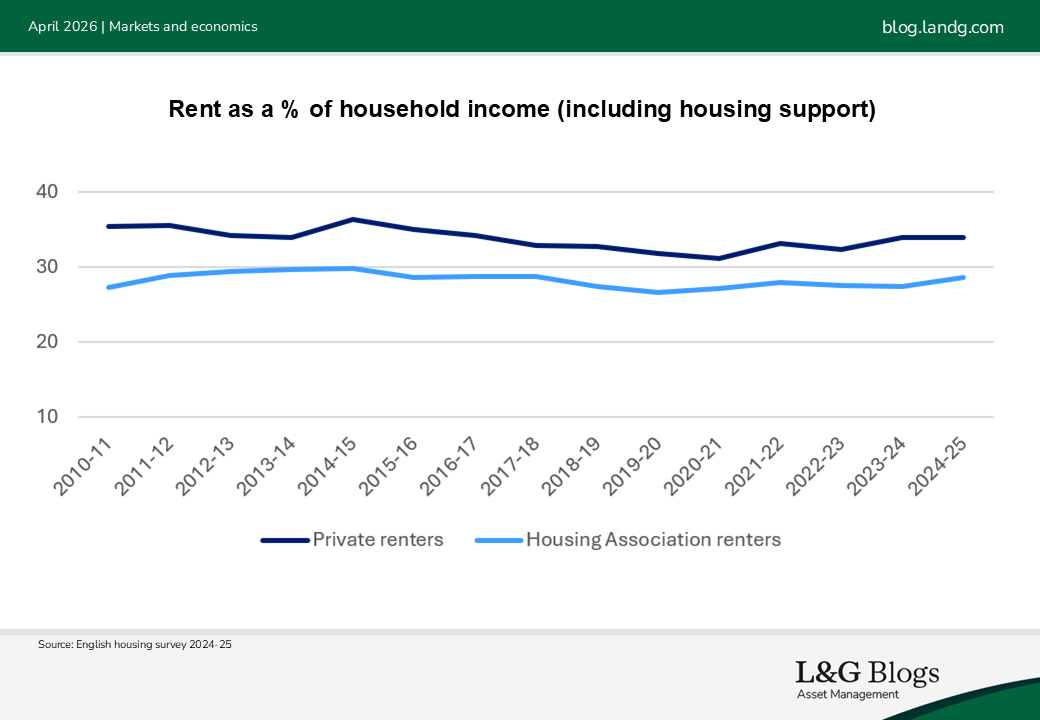

3. A potential trigger for enhanced political intervention would be a deterioration in affordability for Affordable Housing residents. As demonstrated below, affordability levels in the sector are in line with their medium-term average[9]

We believe the need for more safe, secure and healthy homes is as great as ever. Time to deliver.

Assumptions, opinions and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass.

[1] MHCLG, 1st April 2024-31st March 2025

[2] Local Government Association (2026)

[3] House of Commons Library, 2025 Temporary accommodation in England: Issues and government action - House of Commons Library

[4] GLA London Plan 2017 – annual estimate for 2016-2041

[5] In June 2025, the UK government announced a 10-year rent settlement, at CPI+1%, running from April 2026 to March 2036.

[6] Grant is typically bid for on individual projects. In April, Homes England launched a new portfolio approach for strategic partners that allows for bids across multiple sites, providing greater flexibility as schemes and costs evolve.

[7] EBITDA MRI Margin: This is the proportion of operating income that remains after the deduction of operating expenses and the cost of capitalised major repairs.

[8] Section 106 agreements are legally enforceable obligations negotiated between developers and Local Planning Authorities determining Affordable housing provision and contributions to meeting the cost of providing new infrastructure for an area.

[9] English housing survey 2024-25

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.