Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Why Aesop’s fable ‘The Hare and The Tortoise’ still matters for investors approaching withdrawal

Gradually reducing risk is often seen as the safest approach for investors nearing withdrawals. But our modelling suggests a steady allocation may offer a more efficient path — although the right answer ultimately depends on the investor.

As investors approach the point where they need to start withdrawing money, they face a familiar question: should they reduce risk over time or maintain a consistent allocation?

Traditional thinking, combined with psychological influences, tends to favour gradual de-risking, steadily shifting from growth assets into lower-risk holdings such as cash. But is that actually the most efficient way to manage a portfolio in the years leading up to withdrawal? Or is there a better way to allocate risk over time for a given target outcome. Our modelling suggests that, in this context, a steadier approach to risk, more akin to the tortoise than the hare, may offer a more efficient path.

The question investors get wrong

Research by my colleague John Southall explores this trade-off in detail, which you can find here. For the purpose of this blog, I will outline the theory behind his work below.

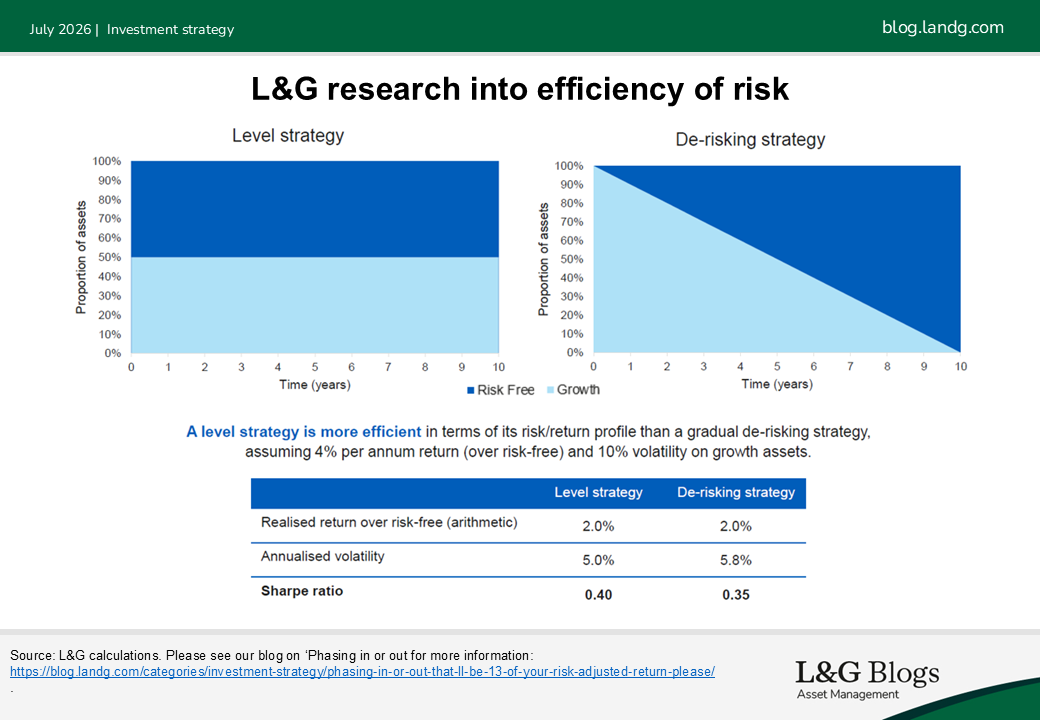

We can think about the problem in simple terms. There are two broad approaches:

- A de-risking strategy: gradually reducing exposure to growth assets over time.

A steady strategy: maintaining a consistent allocation to growth assets.

For this illustration, we assume growth assets return 4% per annum over risk-free, with 10% volatility. By comparing the expected Sharpe ratios, we can see that a steady strategy delivers a more desirable risk/return balance than gradually de-risking. For clarity, a Sharpe ratio measures how much return an investor receives for each unit of risk taken.

Intuitively, this result is surprising for many, as the idea of gradually gliding towards a lower-risk portfolio is intuitively appealing. But, there’s a simple way to explain why actually a steady level of risk taking is more efficient. It spreads risk more evenly across time, avoiding periods where the portfolio is heavily exposed to market movements followed by periods where it is significantly less. This helps reduce reliance on returns when the allocation to growth assets is higher. By contrast, a de-risking strategy approach concentrates risk earlier in the journey, leaving outcomes more exposed to market conditions during those years.

A simple way to think about this is through the familiar story of ‘The Hare and The Tortoise’. The tortoise moves at a steady pace throughout the race and finishes in 60 minutes. The hare runs quickly at the start, but slows significantly in the second half, ultimately finishing later.

Taking risks by running quicker early in the race didn’t help the hare; slowing down too much at the end ultimately cost it the race. In the same way, taking more investment risk early and less later doesn’t always improve expected outcomes.

This doesn’t mean de-risking is never appropriate. However, from a purely financial perspective, it does suggest that gradually reducing risk may not always provide the most efficient path from a risk-return perspective.

What the modelling shows

If we set aside the theory for a moment, we can explore how a steady approach might translate into real-world outcomes.

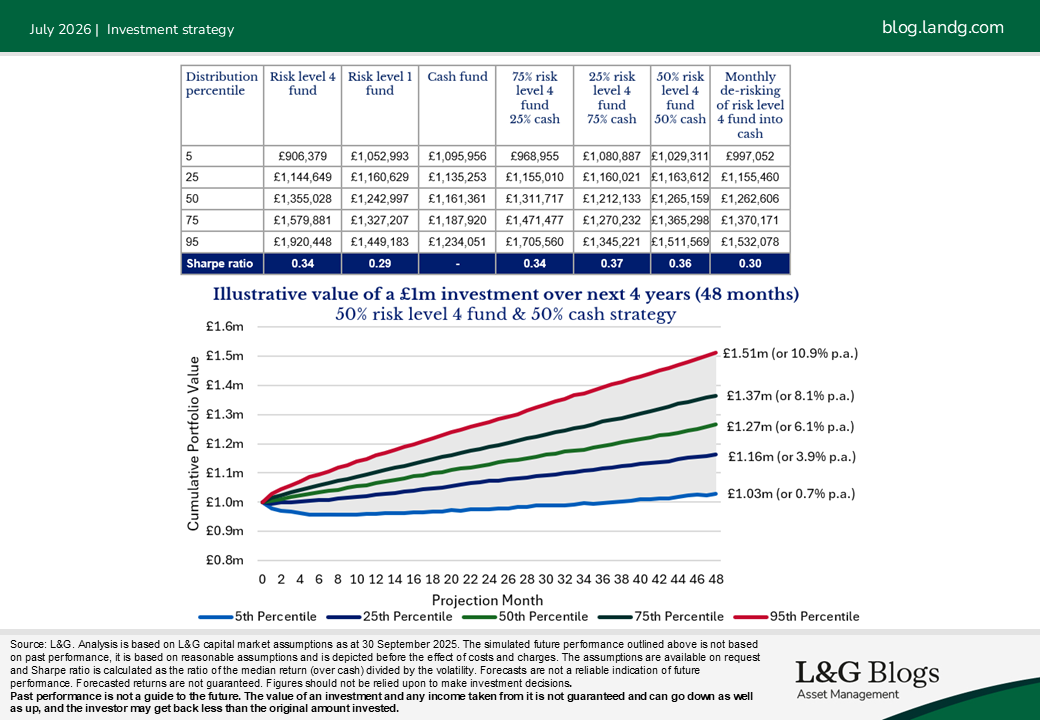

To do this, we model the potential performance of a portfolio over the next four years using different risk-targeted funds — from lower-risk (risk level 1) through to higher-risk (risk level 4), alongside cash. We then compare different ways of combining these assets, including a gradual de-risking path.

In this example, we focus on a £1 million investment and simulate a range of possible outcomes using our capital market assumptions before the impact of any costs and charges. The range of possible outcomes are displayed in the table below, with the simple 50/50 blend of growth assets and cash standing out.

We can see that across a wide range of outcomes, the 50/50 blend:

- Delivers a stronger risk-adjusted return (as measured by the expected Sharpe ratio) than a gradual de-risking approach

- Offers the strongest combination of median return and expected Sharpe ratio

- Produces a relatively narrow distribution of outcomes, providing greater peace of mind about future outcomes. In contrast, monthly de-risking strategy tends to concentrate risk earlier in the journey, therefore increasing the variability of results.

This does not mean that a single allocation will suit every investor. However, returning to the original question, how should investors approach risk as they near a withdrawal phase, the modelling points to a clear conclusion. From a purely financial perspective, maintaining a consistent blend of growth and defensive assets can offer an attractive combination of risk-adjusted return and outcome stability.

Why it isn’t the whole story

However, real‑world investment decisions rarely rest on financial efficiency alone as psychological factors are often at the forefront of investors’ minds. Individual investors may place a higher value on certainty and peace of mind closer to retirement or a large withdrawal when monitoring their savings more closely, therefore assigning greater non‑monetary value to lower‑risk strategies. Institutions, on the other hand, typically have professional advisers and governance structures in place, which can make it easier to look through short‑term psychological uncertainty and prioritise efficiency.

There are also important contextual factors to consider. A portfolio built gradually over time, such as through regular contributions to a DC pension pot, may be treated more cautiously than a one-off windfall like an inheritance. Similarly, an investor’s willingness to take risk will depend on whether this portfolio represents their entire savings, or just one part of a broader financial picture. Accounting for these additional sources of assets, may help with overall risk management when it comes to derisking decisions.[1]

These considerations illustrate just a fraction of the psychological and contextual factors that influence real-world decision making. Once we acknowledge these complexities, it is clear that there is no one-size-fits-all solution when it comes to de-risking portfolios.

Key takeaway: when it comes to managing risk, the tortoise may have the edge:

For investors approaching a withdrawal date, a steady blend of growth assets and defensive assets may offer a more efficient path than gradually reducing risk – but the best approach will always depend on the investor’s individual circumstances and comfort with risk.

[1] For example, in a previous blog, John Southall outlines that ‘human capital’ (the present value of future contributions to DC pension ports) close to retirement is bond-like in its risk profile. As the investor approaches retirement, the ‘human capital’ shrinks towards zero and the retiree’s holistic risk profile can increase unless they choose to derisk their investments. DC glidepaths: a random dog walk down Wall Street

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.