Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Seven factors that shape investment risk in drawdown

For many DC retirees, and likely more in the future, decumulation of their savings converts a pot into a pension. A key challenge is deciding how much investment risk to take, as this shapes both expected spending and the ability to adapt to changing market conditions.

There’s no single ‘right’ level of investment risk in drawdown. Simple rules of thumb (such as invest a percentage in equity equal to 100 minus age) may overlook the factors that influence these trade‑offs in retirement.

This blog sets out seven important – and often overlooked – aspects to consider.

1. Spending flexibility: could spending be cut if markets conditions change?

Rigid spending plans can be difficult to sustain in more challenging market environments, as outcomes are more directly linked to fund performance. By contrast, a more flexible approach to spending can help smooth the impact of changing conditions over time.

Under what we call guided income – which involves drawdown followed by later-life annuitisation - the 1-in-10 worst income experienced in retirement, excluding the state pension, is about 25% worse[1] for a retiree who follows static spending than one following a fully dynamic strategy.

In our view, the more spending can be treated as dynamic rather than fixed, the more investment risk can be tolerated, up to a point.

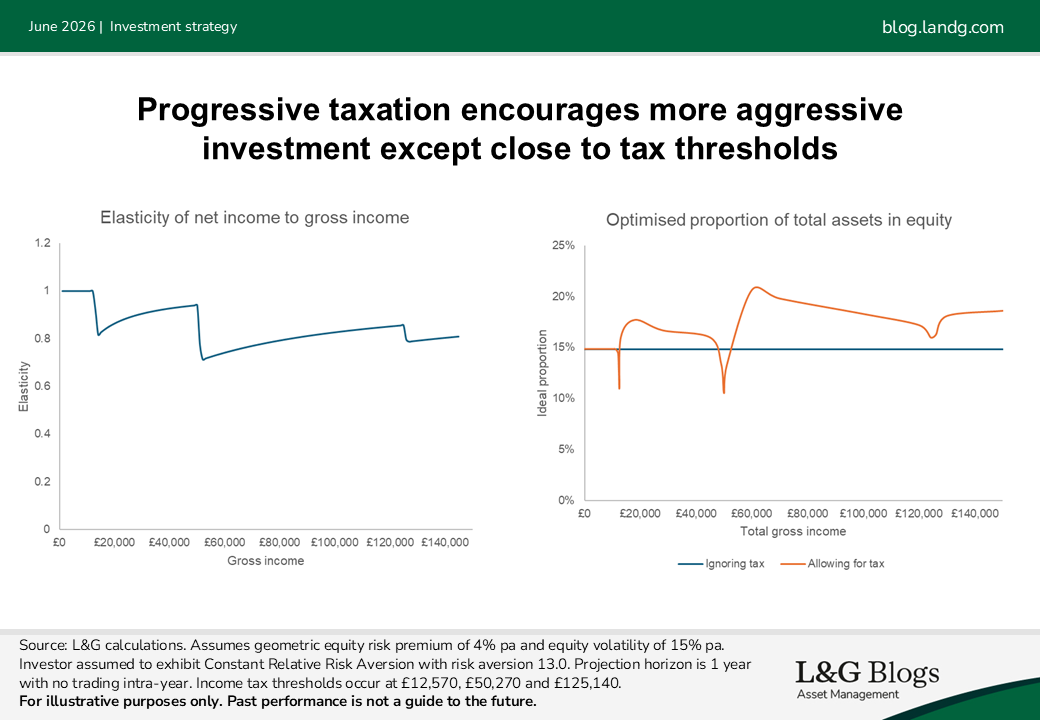

2. Progressive taxation: how much volatility is the tax system already absorbing?

With progressive[2] income tax, percentage changes in net income are dampened relative to percentage changes in gross income. For example, if gross income increases from £20,000 to £21,000 – a 5% rise – then net income only rises by 4.3%[3]. This supports more risk taking than if only looking at pre‑tax spending.[4] This is because volatility in gross income translates into a lower percentage volatility in net income.

There are offsetting effects near tax thresholds[5], but in practice most retirees won’t adjust equity exposure dynamically around them.

3. Plans for drawdown: is this really drawdown for life?

Time horizon and wider objectives matter. Where drawdown is likely to be short‑term, loss aversion can reduce tolerance for volatility; longer horizons tend to support higher risk‑taking. In practice, this can lead the same person to prefer a more defensive portfolio if they plan to drawdown their savings over only a few years. Stronger bequest motives (wanting to pass on wealth as well as spend it) could also encourage a more aggressive strategy.

4. Market conditions: how best to react?

Market conditions can matter and can be reflected in dynamic investment strategies that respond to a range of signals. This dynamism might be supported by quantitative dynamic tilting frameworks such as our MATRIX model, which is designed to adjust positioning over time.

5. Glidepath efficiency: is derisking the right move?

If leaving money behind is not a priority, a well-designed retirement solution would typically combine two features: protection against outliving your savings, through “longevity pooling”, and exposure to growth assets, depending on risk appetite.

In practice, however, most DC savers have limited access to longevity pooling, with annuities remaining the main way to secure an income for life.

This creates a trade‑off: drawdown provides growth exposure, while annuities provide longevity pooling. As members age, longevity insurance becomes more important, encouraging gradual annuitisation. But in practice, fixed expense loadings and friction may make repeat purchases unattractive for some, so annuitisation often happens in one step.

Given this constraint, the most efficient option isn’t to phase into bonds before annuitising, even if this avoids a cliff-edge change in investment strategy[6]. An annuity effectively combines bonds with protection against longevity risk. As such, when longevity risk becomes high in old age, holding a high allocation to bonds isn’t ideal – strong bequest motives aside, it may be more suitable to annuitise.

The upshot is that, subject to annuity market frictions, it can be most efficient to maintain a broadly stable percentage growth allocation[7] until the case for annuitisation becomes compelling.

6. The state and DB pensions: how much of your spending is already insured?

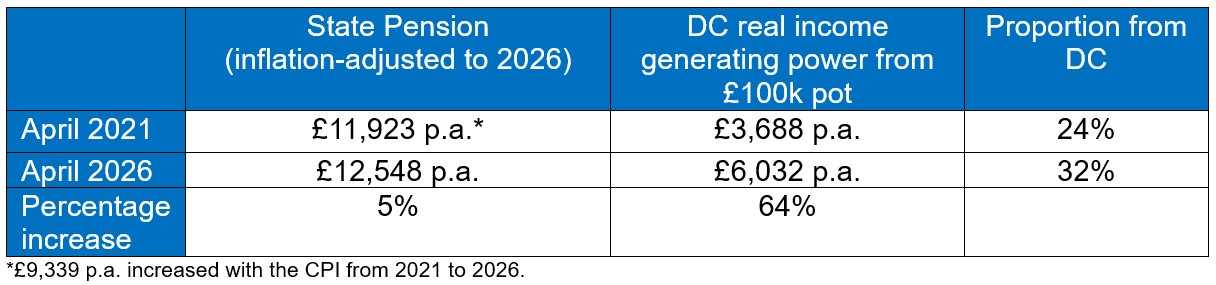

The State Pension can act as a powerful stabiliser within a retiree’s overall finances because it functions as a large annuity-like asset.

The current full State Pension is £12,548 pa, up 34% from £9,339 pa in 2021[8]. Allowing for Consumer Price Index (CPI) inflation it is up about 5%. However, thanks to a large increase in real interest rates, the real income-generating power of DC assets[9] has gone up by an impressive 64% as shown below:

The State Pension can encourage more investment risk‑taking within DC, but the implications for how its influence changes over time –or across members with different DC pot sizes – are less clear‑cut:

- Some research[10] suggests investors are willing to take risk with a broadly stable fraction of their total income. If so, the larger share of overall income coming from DC, rather than the State Pension, suggests less risk‑taking in DC than in 2021.

- Other research[11] is more consistent with a spending‑floor mindset. If the State Pension covers essentials (food, heating, housing), retirees may only be willing to take meaningful investment risk with assets intended to fund spending above that floor[12]. Under that framing, it’s less clear that DC investors should be less growth‑oriented in 2026 than in 2021.

7. Modelling outcomes: can we quantify the trade-offs?

Although how much investment risk to take ultimately depends on appetite for risk, scenario analysis helps us understand the trade‑offs from dialling investment risk up or down. This can include average spending outcomes versus their uncertainty, as well as short-term measures such as the frequency of nominal spending cuts. Watch this space for more on this.

Making sense of the choices

Deciding how much investment risk to take in drawdown is about balancing income, flexibility and resilience. Considering guaranteed income, tax, mortality and market conditions together provides a more robust basis for decisions than simple rules of thumb.

Assumptions opinions and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass. Past performance is not a guide to the future. It should be noted that diversification is no guarantee against a loss in a declining market. Risk management cannot fully eliminate the risk of investment loss.

[1] Source: L&G calculations as at 30 June 2025.

[2] Note that for a flat tax rate, the percentage changes in net and gross income are the same.

[3] From £18,514 to £19,314.

[4] In the past I’ve looked at the potential consequences of means-testing the State Pension on investment strategy, which uses similar logic.

[5] A progressive system with no thresholds, such as net = 50% x gross + £5,000 doesn’t have this offsetting feature.

[6] If anything, it is better to sell bonds first. For more on this please read here and here.

[7] Assuming dynamic withdrawals. If withdrawals are fixed it could encourage a rising glidepath. For more on this read here and here.

[8] The new State Pension: What you'll get - GOV.UK

[9] Calculated by multiplying £100k by the rate on a RPI-linked annuity available at that time.

[10] See e.g. here

[11] See e.g. here

[12] They may display Decreasing Relative Risk Aversion.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.