Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Emerging market debt: resilience in a fragmenting world

Recent market behaviour suggests emerging market debt (EMD) has entered a new phase – one defined not by fragility, but by structural resilience.

The following is an extract from our Q3 2026 ETF outlook.

Key takeaways:

|

The escalation in Middle East tensions – and specifically the Iran conflict – has provided a real-time stress test for global fixed income markets. Historically, geopolitical shocks have triggered broad risk-off moves and acute drawdowns across EMD.

Yet the experience in 2026 has been markedly different. The defining feature of the asset class has been resilience – both in market behaviour and in the structural evolution underpinning emerging economies themselves.

A measured market response

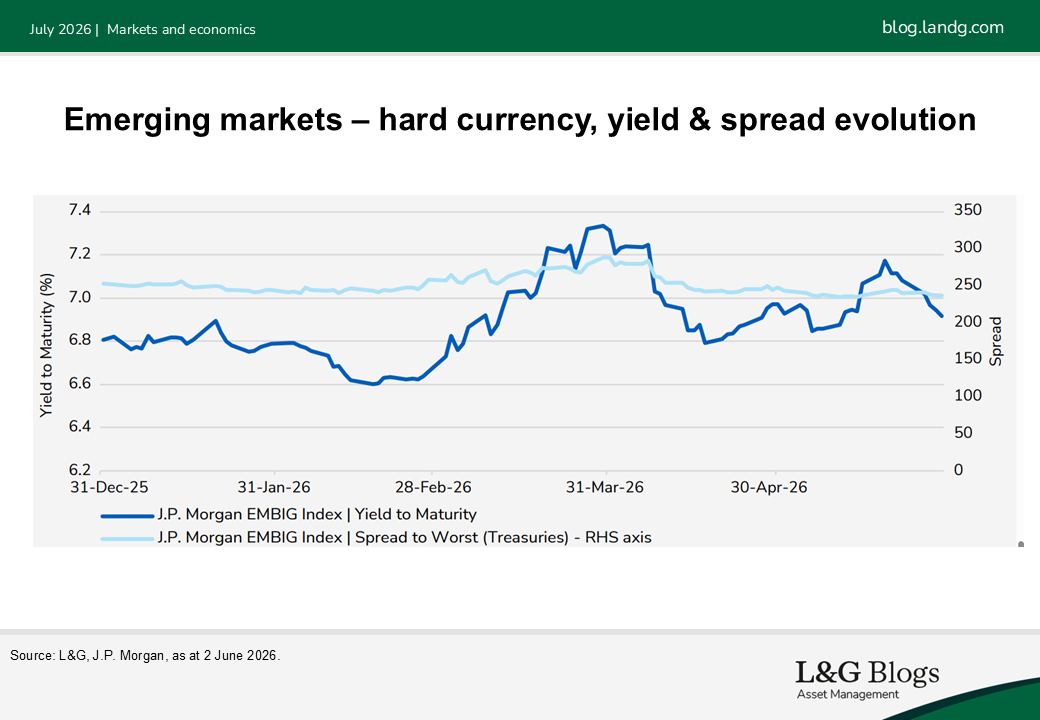

Initial market reactions were notably contained. Hard currency spreads widened modestly at the onset of the conflict before partially retracing as markets reassessed the risk of escalation. This response looks particularly benign in historical context: EM hard currency spreads are currently around 240 basis points (bps) – levels that compare favourably to c.750bps during the Global Financial Crisis, c.630bps during COVID-19, and c.550bps following Russia’s invasion of Ukraine.[1]

Since the start of the Iran War, yields moved higher in parallel, reflecting a temporary repricing of risk rather than a systemic shift in sentiment.

Crucially, this behaviour contrasts with previous episodes, where EMD experienced indiscriminate sell-offs. Instead, the recent period has been defined by differentiation, with dispersion across countries and sectors rather than broad-based weakness.

At the same time, developed market bonds remain under pressure from structurally higher yields and fiscal concerns. Against this backdrop, EMD is increasingly behaving not as a high-beta extension of global risk assets, but as a differentiated and fundamentally supported asset class.

Resilience by design: deeper local markets and stronger fundamentals

The key driver of this resilience is a structural shift in how emerging markets fund themselves. Over the past decade, EM sovereigns have moved away from reliance on external debt towards local currency issuance, supported by deeper domestic capital markets and more stable investor bases.

This shift has materially reduced exposure to currency mismatches and capital outflows that historically amplified EM crises. It has also reshaped the asset class itself. While hard currency indices such as the JPM EMBI represent a ~$1- 1.5 trillion market, they are now complemented by a significantly larger multi trillion local currency universe, captured by the GBI EM.

Importantly, this is not just about scale. Local markets are increasingly anchored by domestic investors – including banks, pension funds and insurers – providing a more stable demand base. Evidence suggests that countries with deeper domestic investor bases exhibit more stable yields and liquidity during periods of global stress.[2]

Across regions, this structural resilience is clear. Countries such as Brazil, Mexico, Indonesia, South Africa, Poland and Malaysia combine well-developed local bond markets with improving macro fundamentals, forming the backbone of the GBI EM universe. Within this broader framework, large markets such as China and India provide an additional layer of stability through deep domestic savings pools.

The result is a fundamentally different EM landscape: one where local markets act as shock absorbers rather than amplifiers of volatility.

Commodities and dispersion: from vulnerability to support

Commodity dynamics have also reinforced resilience. Higher energy prices – traditionally a source of stress – are now supporting fiscal balances and external accounts across key exporters such as Brazil, Mexico, Malaysia and Indonesia, which together account for a meaningful share of the GBI EM index.

This has driven a clear divergence within the asset class, with commodity exporters outperforming more oil-dependent importers. Importantly, this reinforces a broader structural trend: returns in EMD are increasingly driven by country-specific fundamentals rather than broad market sentiment. The combination of commodity exposure and domestic market depth highlights the multi-dimensional nature of resilience across EM.

Resilient performance in practice

Performance trends reinforce this narrative. Following an initial sell-off in March (EM hard currency -3.3%, EM local currency -5.6%), EMD rebounded strongly in April, with both segments posting gains (EM hard currency +2.9%, EM local currency +2.8%).[3] Year-to-date returns remain positive at +2.6% for hard currency and +1.3% for local currency, demonstrating the asset class’s ability to recover quickly from periods of stress.[4]

More broadly, EMD has continued to hold up comparatively well despite heightened geopolitical volatility, supported by strong carry and improving underlying fundamentals.

Positioning for resilience: a selective approach

In this environment, resilience is not uniform – it requires targeted exposure, in our view.

- EM corporates (USD) offer a balance between credit and duration, supported by improving credit quality and a strong investment-grade base. Their shorter duration profile provides a buffer against rate volatility.

- Short-duration hard currency (one to five years) provides a defensive entry point, limiting sensitivity to higher US yields while maintaining attractive carry – offering interest-rate protection alongside resilient spreads.

- Local currency EMD (GBI EM) increasingly represents the core of the resilience story. Broad-based across regions, these markets benefit from domestic funding and reduced reliance on external capital. Within this, countries such as India and China further anchor the asset class through deep local investor bases and evolving policy frameworks.

- Structural developments – such as China’s efforts to promote renminbi-denominated commodity trade – also point towards a gradual shift to a more multi-currency global system, reducing dependence on USD liquidity over time.

Outlook: resilience as a structural feature

Looking ahead, geopolitical risk is likely to remain elevated. However, recent market behaviour suggests that EMD has entered a new phase – one defined not by fragility, but by structural resilience.

Improved policy frameworks, stronger balance sheets, deeper domestic markets, and greater dispersion across countries mean the asset class is potentially better equipped to absorb shocks.

Combined with attractive yields and potential diversification[5] benefits, EMD – across corporates, short-duration hard currency and local currency markets – could offer a compelling allocation for investors seeking stability in an increasingly uncertain world.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

[1][1] Source: L&G, J.P. Morgan, as at 2 June 2026.

[2] Source: https://www.imf.org/-/media/files/publications/gfsr/2025/october/english/ch3.pdf

[3] Source: JPM EMBI and GBI EM indices via Bloomberg as at 2 June 2026.

[4] ibid

[5] It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.