Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

The rising tide of buybacks in UK equity markets

More companies are conducting buybacks, with increased scale and frequency. What was once an occasional capital management lever is fast becoming a structural and fundamental element of corporate financial strategy.

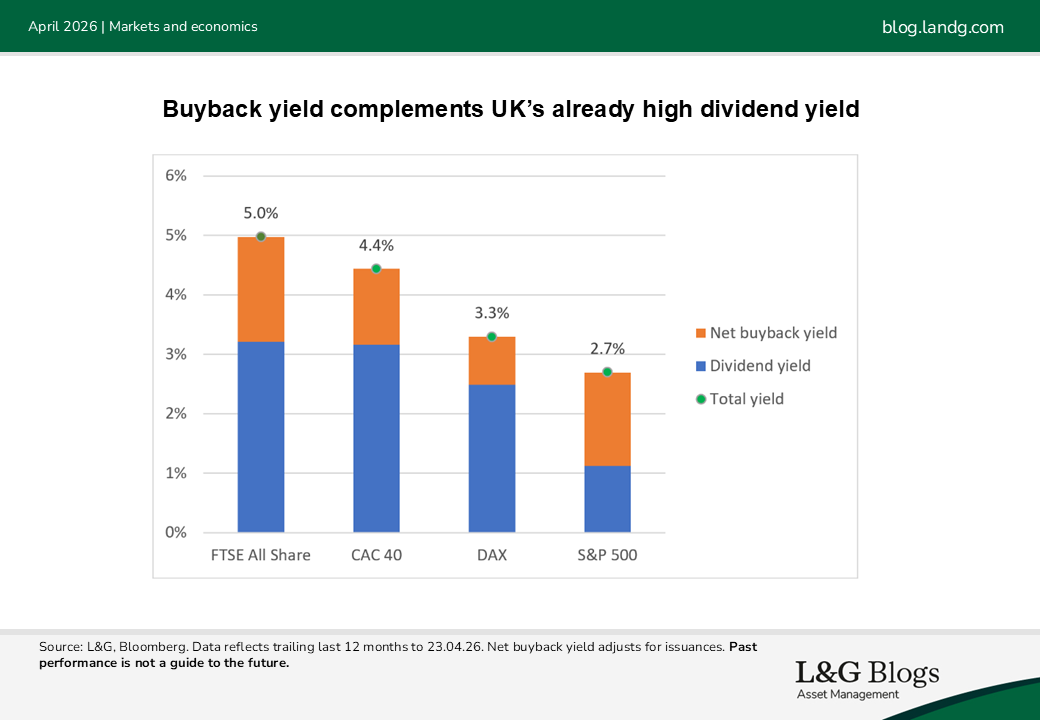

A particularly notable shift in UK equity markets over recent years has been the growing use of share buybacks as a core component of total shareholder return (TSR). So much so that the UK equity market now leads developed peers in the proportion of companies buying back more than 1% of shares outstanding. It is expected that more than £60 billion of UK share buybacks were conducted in 2025, over double the amount in 2019.[1] As a result, the UK has the highest total yield versus developed market peers.

Broadening participation, deepening commitment

Across sectors – from financials to telecoms to consumer businesses – an increasing number of listed companies are actively repurchasing shares. But it’s not just breadth that is increasing; the quantum is too. Companies are committing substantial sums (often billions) to buyback programmes with announcements that dwarf what was typical even a few years ago. Equally important is the cadence. Some buybacks look more like recurring programmes embedded within long-term capital allocation frameworks, and less like one-off, opportunistic actions. Prudential* is a good example: strong operating surplus generation is enabling regular, repeatable buybacks under its improved capital return strategy. This shift from episodic to ongoing activity signals a deeper philosophical change in how management teams view capital returns.

The forces powering the shift

There are several drivers behind this buyback boom. First, suppressed valuations and share price weakness make buybacks a potentially attractive deployment of capital —particularly for companies with healthy balance sheets and strong cash generation. Foreign ownership now dominates UK listed shares[2], with US investors accounting for over half of overseas ownership of UK quoted companies.[3] Naturally they draw on their domestic market experience as a blueprint, where buybacks typically outweigh dividends by around 60/40. Therefore this increasing influence has resulted in a shift in UK capital allocation frameworks.

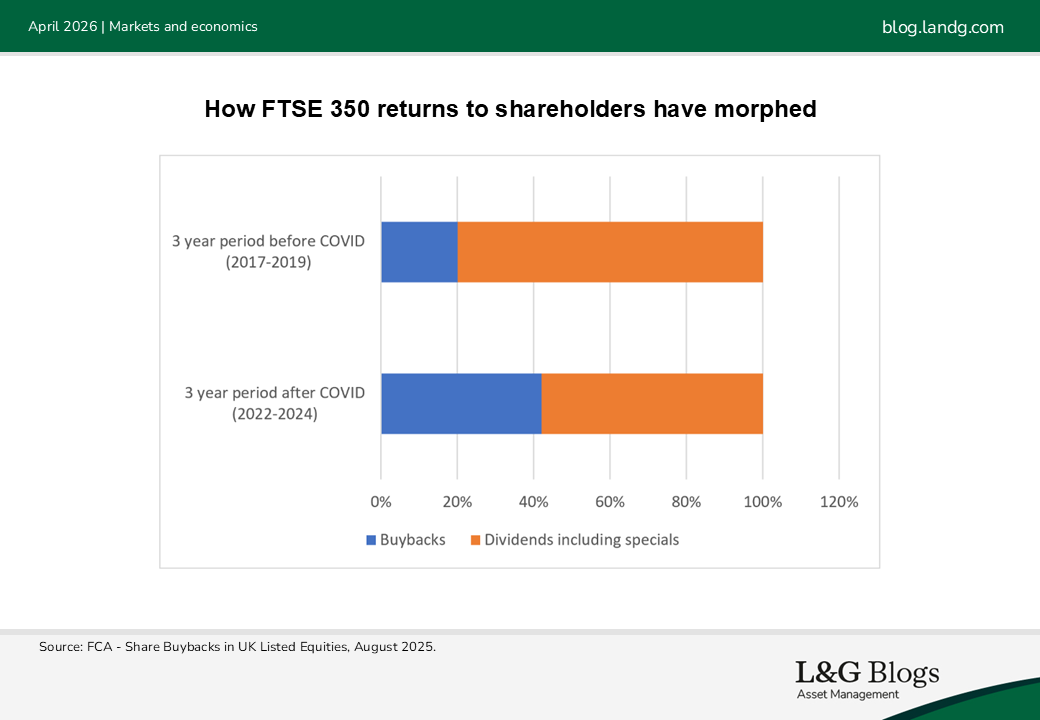

Second, buybacks are more flexible than dividends and can be adjusted without the signalling effects of cutting a payout. We have observed this play out through the visible shift in the capital allocation strategies of UK companies towards a greater mix of dividends plus buybacks, versus the pre-COVID-19 era of a more singular focus on dividends. This diversion of capital from distributions to repurchases is one of the contributing factors towards the improvement in UK dividend cover versus ten years ago[4]. Additionally, special dividend payouts in 2025 were about half the 10-year average, which again points to this pivot.[5]

In some cases, buyback capacity is being boosted by structural tailwinds. Market-wide, companies have lower future pension obligations versus years before, freeing up free cashflow. Different sectors have their own stories too. For example, recently reduced Common Equity Tier 1 (CET1) constraints by the Bank of England has enabled UK banks to increase buyback programmes thanks to ‘surplus’ capital[6], supported in some cases by the unwinding of deferred tax assets.

Financial logic and strategic appeal

Buybacks provide companies with a mechanism to return capital while being aligned with investors through potentially supporting valuation via reduced share count. During cycles of depressed equity valuations, the financial logic of buybacks, even using modest leverage, can be compelling. They can tarfet an attractive opportunity relative to alternative uses of capital. By going down this route, it can be perceived as a signal of a company’s implicit confidence that its shares are undervalued.

They can be switched on and off more easily than dividends, offering optionality in uncertain environments. For companies with substantial excess capital and robust balance sheets, buybacks can be a rational outlet in periods when growth investments or M&A do not meet return thresholds.

When discipline slips

Given the trend, some management teams may feel obliged to initiate buybacks even when it is not the best use of capital – a capital allocation version of ‘fear of missing out’, perhaps?

One small-cap management team we spoke to admitted that investor pressure to commit to a buyback policy has curtailed them. Despite being a useful instrument in a CFO’s toolkit, an over‑commitment to returning capital may constrain companies at precisely the wrong moment; it could limit their ability to pursue investment or M&A opportunities which would have been in the long-term interests of shareholders.

Another criticism we have is when capital allocation frameworks are not always well-articulated, leaving investors guessing where buybacks sit in the hierarchy of priorities and concerned that management may continue buybacks irrespective of the share price. Conversely, specific comments from management about share price levels they would or would not buy shares at can send unintended signals about their perception of intrinsic value. We would call out Next* as a good example for being clear with investors about the price discipline it applies and the rate of return it is seeking, leaving the market under no illusion as to when it will halt buying back shares.[7] This contrasts with other companies that continue regardless of valuation.

Clarity in capital prioritisation

Overall, buybacks have evolved from seldom used, occasional tools into more commonly seen, embedded parts of corporate capital allocation frameworks. For investors, they increasingly form a meaningful component of potential valuation upside, particularly in a world where capital efficiency and disciplined financial management are prized. However, understanding the motivations, sustainability and strategic context behind buybacks has never been more important. Buybacks are not the right decision for every company, or at all points in a company’s cycle; so we believe it is crucial to seek clear articulation from management teams on their capital allocation policy, which remains a core building block of our investment process.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] Computershare UK Dividend Monitor, Q4 2025, which is the latest report. ‘We project total UK share buybacks were £63.6bn for the year’ UK Dividend Monitor Q4 2025

[2] London Stock Exchange Putting UK Equities in perspective | LSEG

[3] Office for National Statistics, Ownership of UK quoted shares: 2024

[4] In 2015, dividend cover for FTSE 100 stocks was below 1.5x, but in 2025 it is expected it was above 2x. AJB_Q1-2026-Dividend-dashboard.pdf

[5] Computershare UK Dividend Monitor Q4 2025

[6] On 2nd December 2025, the Financial Policy Committee of the Bank of England set out its decision to lower system-wide capital benchmarks, resulting in Tier 1 capital requirements reducing from c14% to c13% of Risk Weighted Assets – equivalent to a CET1 ratio of around 11%. Financial Stability in Focus: The FPC’s assessment of bank capital requirements | Bank of England

[7] See results reports for more information e.g. 29th October 2025 Trading Update which explained that the share price is higher than their buyback limit, and buybacks are subject to achieving a minimum 8% Equivalent Rate of Return, hence surplus cash would likely be returned to shareholders via a special dividend instead. Q3 2025/26 Trading Statement

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.