Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Tech issuance is reshaping the IG credit market

The sheer scale of issuance to fund AI capex is changing the dynamics of the investment grade (IG) market, highlighting potential downsides of standard market cap credit indices.

Key takeaways

|

Since September, tech has been the dominant source of IG supply. Market conditions have been supportive, demand has remained deep, and mega‑cap issuers have moved quickly to lock in large, long‑dated funding for AI and data infrastructure.

Meta* set the tone in October with a $30bn financing[2], the largest corporate bond deal of 2025. Public tech IG issuance exceeded $200bn over the year[3], with hyperscalers behind most of the largest transactions.

Investor demand has been heavy throughout, with Alphabet’s* latest USD deal drawing more than $100bn of orders, allowing the transaction to grow from $15bn to $20bn.[4]

The scale of AI‑related capex is reshaping the supply mix. Borrowing linked to AI infrastructure across tech, utilities and data centres has accelerated sharply. Issuance tied to this theme rose from $17bn in 2024 to $245bn in 2025[5] as companies race to secure power, land and compute capacity.

Europe steps up

Europe has become a much more important part of the funding story. Issuers are increasingly capitalising on the depth of demand outside the US, while also securing attractive funding levels and avoiding saturation of the USD market.

Google’s 100‑year GBP tranche highlights the long‑end sterling demand, a tenor typically reserved for governments and utilities and supported by structural UK liability matching flows. The company also completed a five‑part CHF transaction, tapping Swiss institutions that continue to favour high-quality corporate credit.

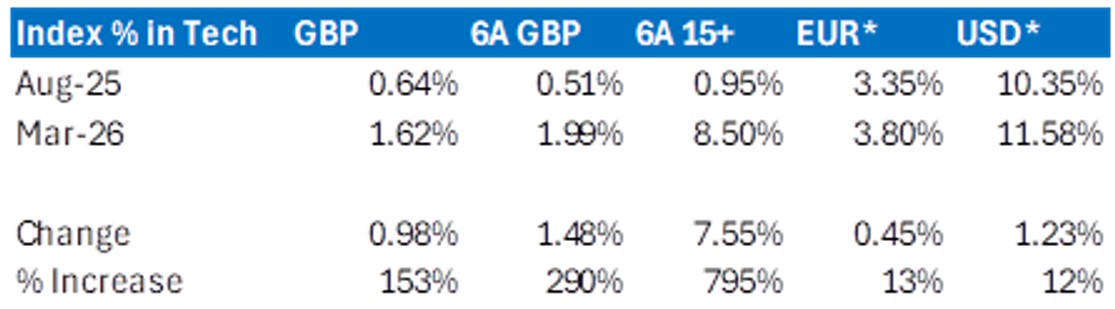

Amazon* added further momentum by issuing the largest-ever EUR corporate bond deal at €14.5bn, underlining both the scale of AI‑driven funding needs and the strength of European demand from investors that have historically been starved of tech risk. Europe now plays a more central role in funding plans rather than acting as a marginal alternative to USD markets, a shift that is clear in corporate credit index composition, as shown in the table below:

Source: GBP (iboxx GBP non-gilt index), EUR and USD Bloomberg corporate indices as at 24 March 2026. *Note – AMZN added from Consumer cyclicals.

More complex funding structures emerge

Beignet Investor LLC* highlights how large tech issuers are turning to more sophisticated financing structures to fund AI infrastructure at scale. The special-purpose vehicle (SPV) was created to finance Meta’s Hyperion data‑centre project in Louisiana, with $27bn issued with a 2049 maturity supporting the company’s long‑term compute needs.[6]

By using a standalone project structure, Meta was able to secure long‑dated financing without bringing the debt onto its balance sheet, while retaining economic exposure to the asset. Blue Owl*, via Beignet, owns 80% of the project, with Meta holding the remaining 20% through an indirect subsidiary. The A+‑rated issuance was supported by Meta’s role as anchor tenant and its guarantee of cost overruns, with PIMCO* anchoring the deal with an $18bn order.

This kind of structure reflects a broader shift in IG markets, where the scale and duration of AI spending is driving greater use of hybrid solutions that sit somewhere between traditional corporate bonds and project finance.

Equity-style dynamics in credit

Another consequence of the jump in tech issuance is that public credit markets are beginning to reflect a familiar equity concern: the growing dominance of a small number of US mega cap technology issuers.

Hyperscalers now account for a much larger share of IG supply, increasing concentration within credit indices in a way that investors will recognise from equity benchmarks. This shift has been reinforced by the growing ease of corporate bond trading through portfolio trades, which has improved liquidity and added another equitisation style feature to IG markets.

While credit concentration remains modest compared with equities, periods of heavy issuance from large technology firms mean they increasingly shape marginal supply and index dynamics. As credit indices become more tech heavy and more responsive to broad risk sentiment, this brings into focus whether traditional market cap benchmarks still deliver the diversification investors intend, or whether alternative approaches such as equal‑weighted exposures deserve greater consideration.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] It should be noted that diversification is no guarantee against a loss in a declining market.

[2] Bloomberg as at 30 October 2025.

[3] Bloomberg as at 31 December 2025.

[4] Bloomberg as at 11 March 2026.

[5] Bloomberg as at 31 December 2025.

[6] Bloomberg as at 16 October 2025.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.