Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Tariffs: How to manage portfolio uncertainty

Significant uncertainty remains about the outcomes of tariffs, and it’s hard to have an edge on forecasting this. However, are there approaches that multi-asset investors can take to navigate these conditions?

The news on tariffs changes daily, but there are three things we believe we can be more confident on:

- The cat is out the bag – Tariff revenues in the US are already higher this year than over the same period in any previous years in the past decade. Even the UK – one of the US’s closer allies, which has agreed a trade deal with the US – faces a 10% tariff rate on most exports. While we, and the market, may be more optimistic about the future of tariffs than we were immediately after ‘Liberation Day’, it seems highly likely that tariff rates around the world will be higher at the end of this year than they were in previous years. A recent investors survey by Goldman Sachs showed that 91% of respondents expect average US tariffs rates to be over 10% by year end, compared to 2.5% in 2024.

- The impact of tariffs is unequal – While countries like Mexico, Canada and Vietnam export in excess of 10% of their GDP to the US, other regions like Europe, the UK and China only have exports worth around 2-3% of GDP to the US. Tariff impacts will vary by region and sector, and should not be seen as having a blanket impact.

- Watch out for second-order impacts – The second-order impacts of tariffs may be more significant than the direct price impacts. The hit to consumer and business confidence has been evident in surveys. That may encourage spending and investment to be rerouted, paused or cancelled altogether. The economics world awaits hard data to see if the hit to confidence translates into true changes in behaviours.

Have you considered upside risks?

We’re wired to focus on downside risks, especially when the tariff headlines are loud and negative. But it’s important we consider upside risks. Here are some alternative takeaways:

- Behavioural bias clouds our judgment – Investors can be influenced by headlines more than hard data. It’s not all bad out there, but sometimes we need to work harder to see the good. This is particularly evident in the UK, where surveys reveal a particularly negative skew of views on the US administration, making us more susceptible to be anchored by the negative headlines around us

- Tariffs ≠ GDP drag – Tariffs are often framed as a tax on consumers and a drag on growth. But evidence shows tax levels don’t reliably translate across to GDP growth. If redistributed well, tariff revenues could even support growth, not hinder it.

- Resilient supply chains = lower volatility – If the policy trend leads to more distributed, robust supply chains, that could be a win. Less exposure to single-point shocks like COVID-19 means economies, and in turn markets, may become more stable. While free trade is optimal in theory, if supply chains become too stretched and lean they become fragile. So the trade war might potentially lead to more robust buffers against future shocks. During President Trump’s first term in the White House, we saw more bilateral trade deals signed by countries outside the US than in any other period. Even if the US starts looking more inward, the rest of the world still wants to trade.

- Disruption often births innovation – The Cold War gave us the ‘space race’. COVID-19 gave us mRNA vaccines. If current policy choices spur a new era of global competition, we could be on the brink of an innovation age. AI and deregulation could add fuel to this melting pot to further spur the innovation age. This could potentially accelerate breakthroughs, boosting productivity and growth, while easing inflation.

- Divergence may be diversification’s* comeback – It’s been a cold winter for multi-asset investors, but we are seeing early signs that regional economic divergence could be leading to lower correlations across and within asset classes – potentially reviving the diversification benefits that had faded in a globalised, synchronised world.

Accepting uncertainty

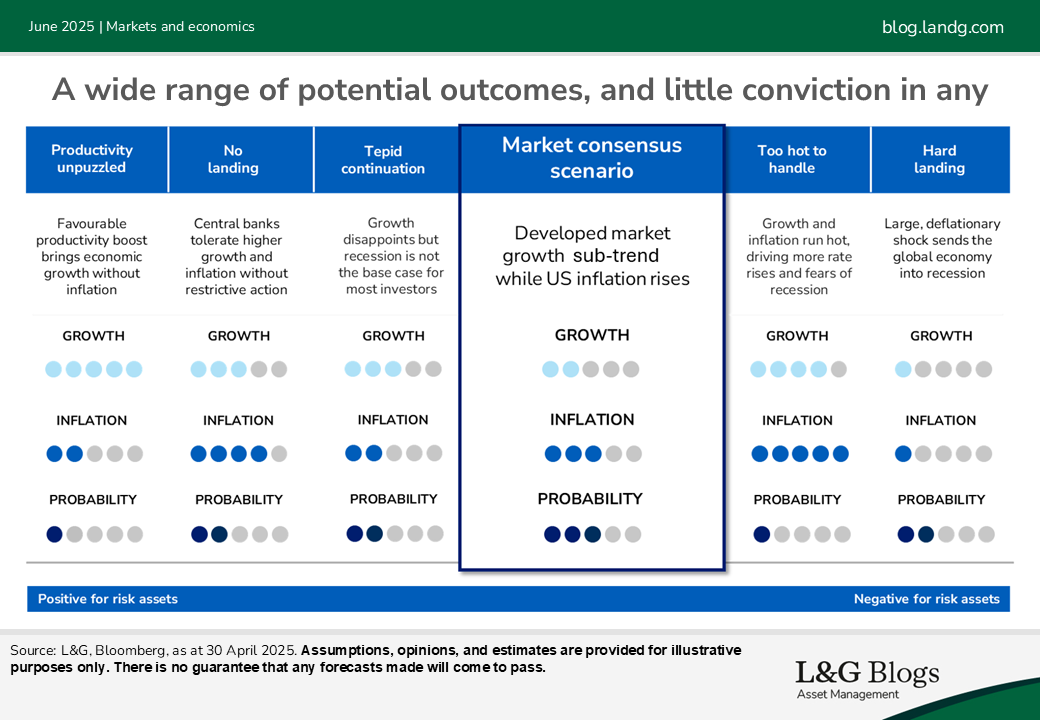

Overall, we need to step back from tariffs and recognise the broad economic uncertainty that prevails. To monitor, measure, and navigate that, the team undergoes rigorous scenario analysis.

Below is a summary of the main economic scenarios we see ahead of us over the next 12 months. This does not cover extreme tail risks, but more realistic spectrum of outcomes, with a range of inflation, growth and therefore potential market returns.

The three Ds of multi-asset investing

As multi-asset fund managers, we aim to deliver good outcomes for clients in a wide range of scenarios, rather than exceptional outcomes in just one outcome. We believe we can achieve that with diversification*, dedication and discipline.

- Diversification* – Diversifying portfolios by asset class, sector and region, we seek to minimise our reliance on any one source of potential returns. We do not aim to predict which outcome we will see over months and years ahead, but rather prepare portfolios for the inherent uncertainty that comes with investing. While we don’t believe diversification is a ‘free lunch’ in investing, we think it’s worth the price.

- Dedication – Our large team of economists, strategists and fund managers is built on the mantra of specialisation and collaboration. As a fund manager, I can rely on select specialists by region and by asset class to not just read the headlines but to dive deep into the details and share their findings. And while some specialists are looking at the attention-grabbing narratives, others continue to focus on their specific areas of expertise. This allows us to analyse the consensus narrative in markets, and identify its vulnerabilities, aiming to deliver deep and differentiated views.

- Discipline – By maintaining a disciplined process, we seek to mitigate the destructive impact of behavioural biases which can get exaggerated under stressful conditions and heightened when emotive political events rise to the top of the news agenda. We aim to do this by sticking to a system of scoring trades, following pre-defined signposts, and maintaining rigorous and regular investment debate to identify both opportunities and risks.

By following these principles, we believe we can set ourselves up for the best chances of success against a backdrop of uncertainty and change.

*It should be noted that diversification is no guarantee against a loss in a declining market.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.