Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Stablecoins: disruptive potential vs. reality

What are stablecoins? How they could disrupt banks and payment networks, and what’s holding back mainstream adoption?

Imagine moving money across borders in seconds, 24/7, at near-zero cost. Stablecoins promised this revolution. Yet despite the hype, their impact on mainstream banking and payments has so far been limited. Real-world adoption remains underwhelming.

What are stablecoins and why are they disruptive?

Stablecoins are digital assets designed to maintain a stable value, typically through a 1:1 peg to a fiat currency such as the US dollar. They usually achieve this stability by being backed with high-quality, short-term assets like cash and US Treasury bills. Unlike volatile crypto assets such as Bitcoin, stablecoins aim to maintain a steady price, potentially making them suitable as a medium of exchange or store of value in a way that speculative crypto isn’t.

They enable peer-to-peer transfers without traditional intermediaries (banks or card networks). So, in principle, they offer near-instant settlement, 24/7 availability, and lower potential costs through reduced intermediation. Cross-border payments are potentially a particularly attractive use-case, as traditional remittances remain costly and inefficient. For example, sending $200 abroad costs around 6% on average, according to the World Bank. Stablecoins, by contrast, can enable near-instant transfers at minimal cost.

Regulatory developments

Regulation is increasingly shaping the trajectory of stablecoins. Early growth took place in a largely unregulated environment, but policymakers have moved quickly to establish clearer rules around issuance, reserves and investor protection.

In the US, proposals such as the GENIUS Act aim to formalise stablecoins as fully backed payment instruments, with strict requirements on reserve quality and redemption. In Europe, the Markets in Crypto-Assets (MiCA) framework has already introduced a comprehensive regime, requiring authorisation, robust reserve backing and limits on the ability of issuers to offer yield.

Stablecoins are being positioned as payment instruments across different jurisdictions rather than deposit substitutes, with safeguards designed to target financial stability and limit direct competition with the banking system.

While this could increase confidence in the asset class over time, it also creates short‑term friction. Regulatory fragmentation, evolving rules and differing approaches across regions remain a barrier to seamless global adoption.

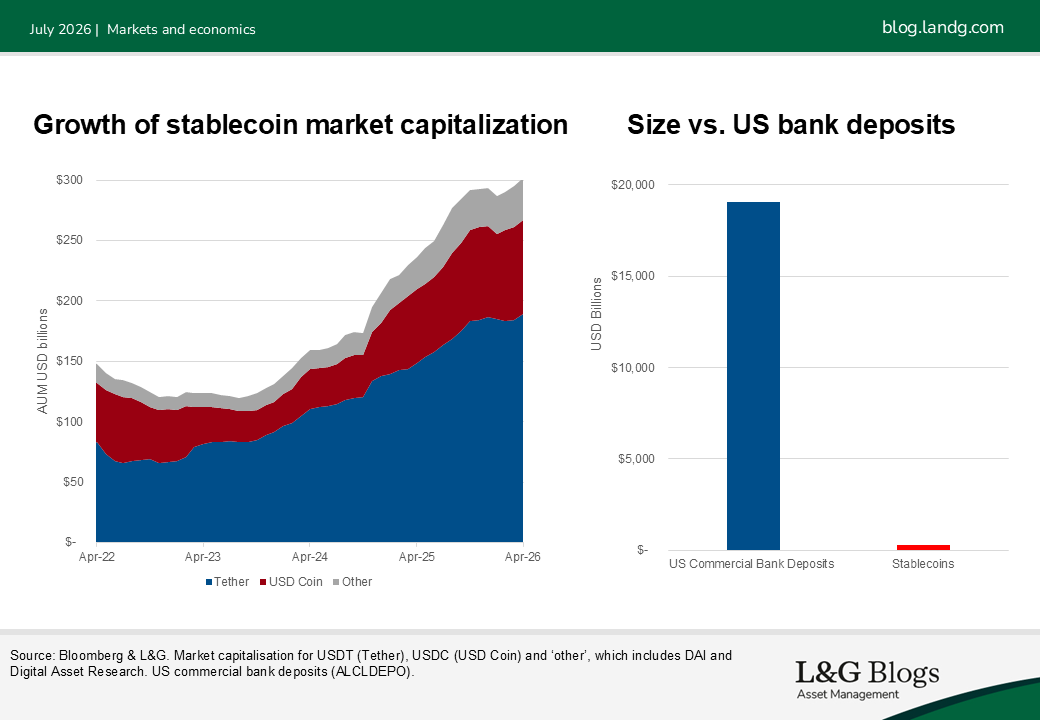

Adoption of stablecoins vs. traditional money

Despite rapid growth from a standing start, stablecoins remain small relative to traditional money. As of mid-2026, the total outstanding value of all stablecoins globally is around $300 billion. By comparison, U.S. commercial bank deposits alone exceed $19 trillion.

Why has stablecoin uptake been slow?

Despite their theoretical advantages, stablecoins have struggled to move beyond niche use cases into everyday payments.

Several practical and behavioural factors help explain this gap. First, existing payment systems already work well for most users. For the majority of consumers and businesses, bank payments and cards are fast, reliable and widely accepted. History suggests that shifting entrenched payment habits is difficult unless the alternative offers a clear and tangible improvement.

Second, onboarding and usability remain a barrier. Using stablecoins typically requires converting fiat into tokens and back again, often via exchanges or intermediaries. This introduces additional steps, cost, and operational complexity compared with traditional payment methods.

Third, there are trust and risk considerations. Unlike bank deposits, stablecoins generally do not pay interest and do not benefit from deposit insurance. This can make them unattractive as a store of value for households and corporate treasurers, particularly in a higher-rate environment.

Finally, the competitive advantage of stablecoins is narrowing. Historically, lower cost and faster cross-border payments were key differentiators. However, banks and fintechs have continued to invest in improving payment infrastructure. Initiatives such as enhancements to SWIFT and real-time payment rails have significantly reduced settlement times and friction in traditional systems.

Banking economics: deposit displacement implications

Stablecoins are not bank deposits but claims on issuer reserves. When deposits are converted, funds move off bank balance sheets and into assets such as US Treasuries, with a portion returning via issuer deposits. This represents a form of partial deposit disintermediation.

If adoption scales, the main implication is a potential reduction in stable, low-cost retail funding, which could modestly constrain credit creation. However, the effect is not one‑for‑one, as some funds are recycled back into the banking system.

The more important shift may be in the composition of funding, with banks relying less on granular retail deposits and more on larger, concentrated institutional balances linked to stablecoin issuers. This could increase funding volatility and alter liquidity dynamics, particularly in stress scenarios.

Stablecoins could also, in theory, bypass traditional card networks in some use cases, particularly for cross-border payments. In practice, near-term disruption appears limited, given the importance of familiarity, trust, and consumer protections. A more likely path is integration rather than displacement, with incumbents already exploring the use of stablecoins for back-end settlement.

What should we make of stablecoins?

Stablecoins clearly have disruptive potential, but we believe any shift in banking and payments is likely to be gradual rather than abrupt. A more realistic outcome is a hybrid system, where privately issued stablecoins, bank-issued tokens and central bank digital currencies all coexist, each serving different use cases.

In practice, stablecoins are more likely to complement the existing system than replace it. They could prove particularly useful in areas such as 24/7 cross-border wholesale settlement or as on-chain collateral, while banks continue to play their core role in deposit-taking and credit creation.

For adoption to accelerate meaningfully, a few things would probably need to fall into place. End users would need clearer incentives to switch, regulation would need to become more consistent across jurisdictions, and stablecoins would have to be integrated more seamlessly into everyday financial workflows.

In the meantime, both regulators and incumbents are preparing for a range of possible outcomes. Stablecoins could form part of the future monetary landscape, but as one component within a broader financial ecosystem rather than a wholesale replacement for banks and existing infrastructure.

Sources:

https://remittanceprices.worldbank.org/

‘Stablecoins – risks and opportunities’, Barclays February 2026

‘Its not all about stablecoin’, Barclays December 2026

‘Stablecoins 2030 Web3 to Wall Street’, September 2025

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.