Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Six reasons to believe in Sub-Saharan Africa

From declining debt to prudent policy, we lay out some compelling arguments supporting the investment case for African sovereigns.

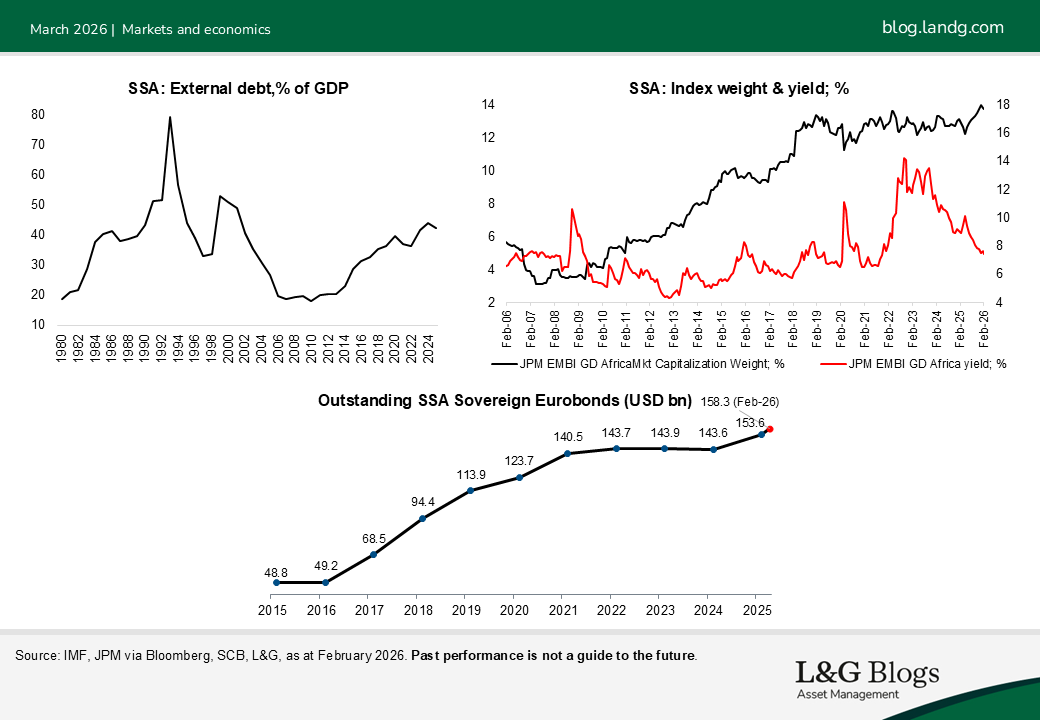

Africa’s access to global capital markets has expanded rapidly since the first external bond issues from South Africa, Tunisia and Morocco in the mid-1990s, and Egypt in the early 2000s.

Issuance from Sub-Saharan Africa (SSA), which excludes North Africa (Morocco, Tunisia and Egypt) and South Africa, took off in the mid-2000s, helped by two factors. Various multilateral initiatives over the 1990s / early 2000s helped lower debt ratios and create fiscal room to borrow. Meanwhile, the low interest rate environment following the global financial crisis lowered borrowing costs.

Starting with Seychelles in 2006 with a $200mn issue, several issuers have tapped markets over the past 20 years. Of the 45 countries that the IMF includes under the SSA region, 17 have, have had or are planning to issue Eurobonds. Resultantly, Africa’s weight in benchmark indices has increased, particularly from the early 2010s (chart below). Indeed, in just the past decade, the size of the traded float of sovereign Eurobonds has increased by over $100bn.

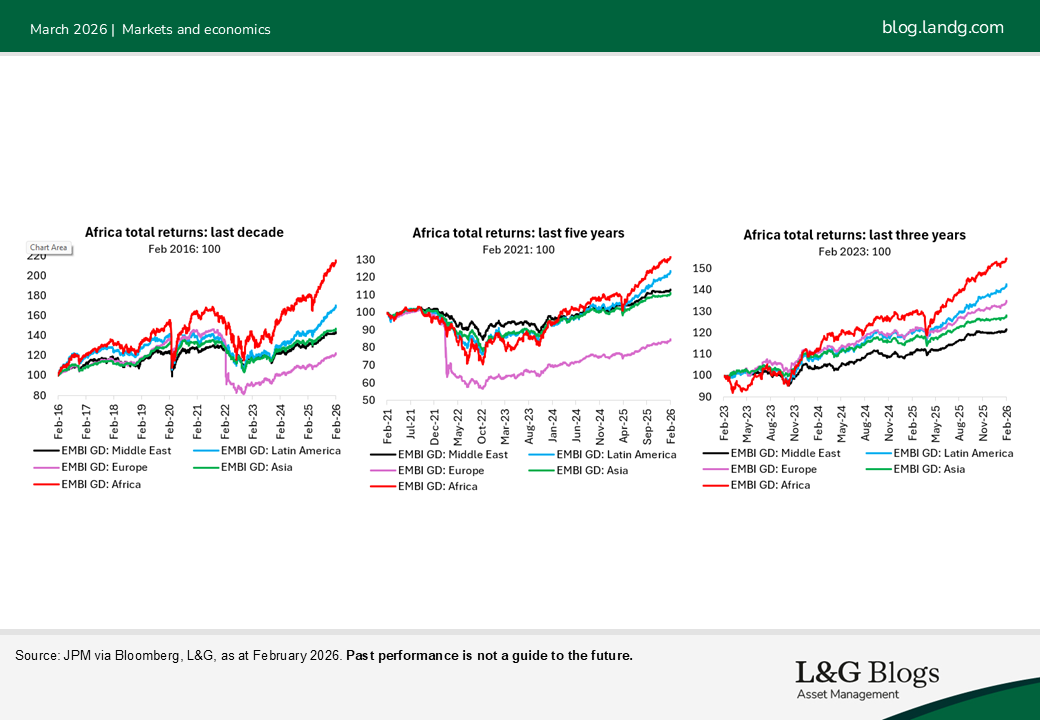

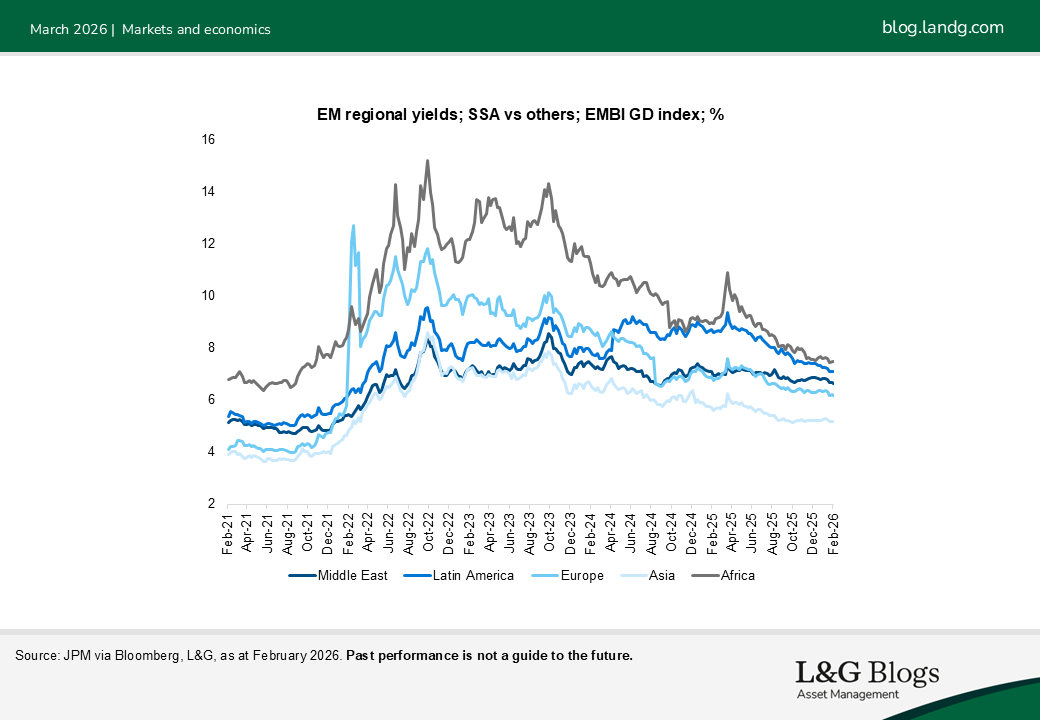

This consistent issuance reflects sustained investor interest, driven by the historical outperformance of African credit relative to other EM regions. As shown in the charts below, the Africa sub-index of a widely followed sovereign benchmark has historically outperformed all other EM regions on a three, five and 10-year basis. The performance is even more impressive given the relatively small size of ‘local’ investor demand, which we believe can help to provide many credit curves – particularly in MENA region – with greater resilience.

Why Africa?

It is easy to say that this performance reflects a virtuous cycle of investor demand for African paper, which in turn can drive return potential. Digging a little deeper highlights an improving investment case for SSA:

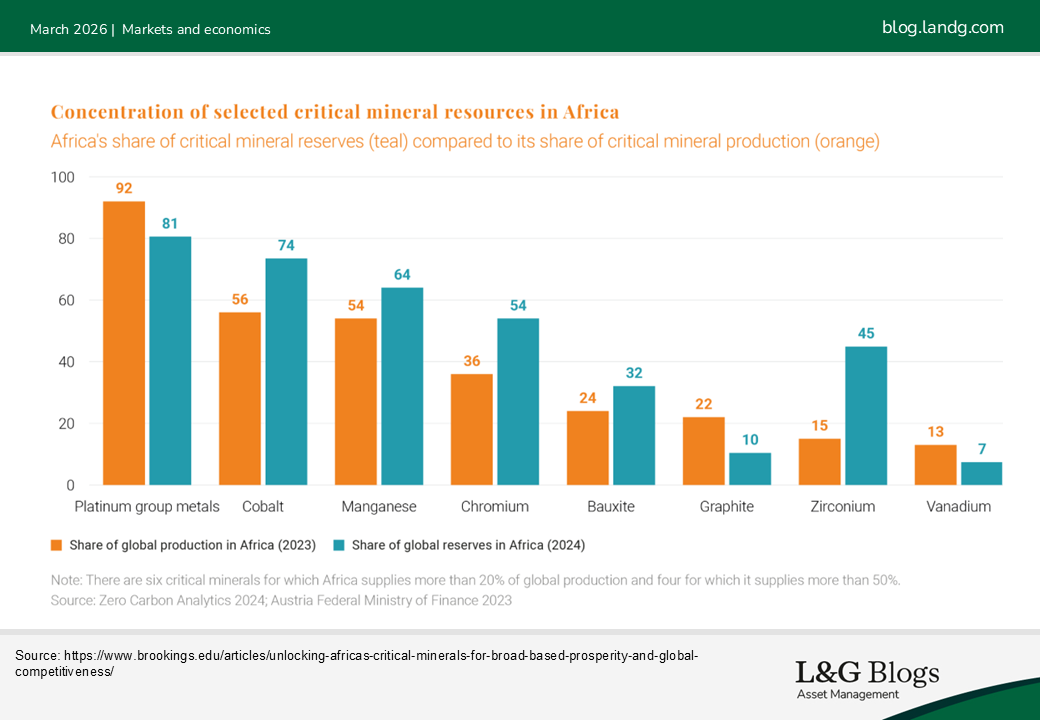

- Diversity[1]. SSA is arguably the most diverse of all EM regions. The continent includes oil exporters such as Nigeria, Angola and Gabon, metals exporters such as Ghana (gold) and Zambia (copper), countries with exports/large deposits of critical minerals (DRC, Namibia, Mozambique; chart below), significant agriculture exporters such as Kenya and Ivory Coast and aspiring O&G producers (Senegal, Mozambique).[2]

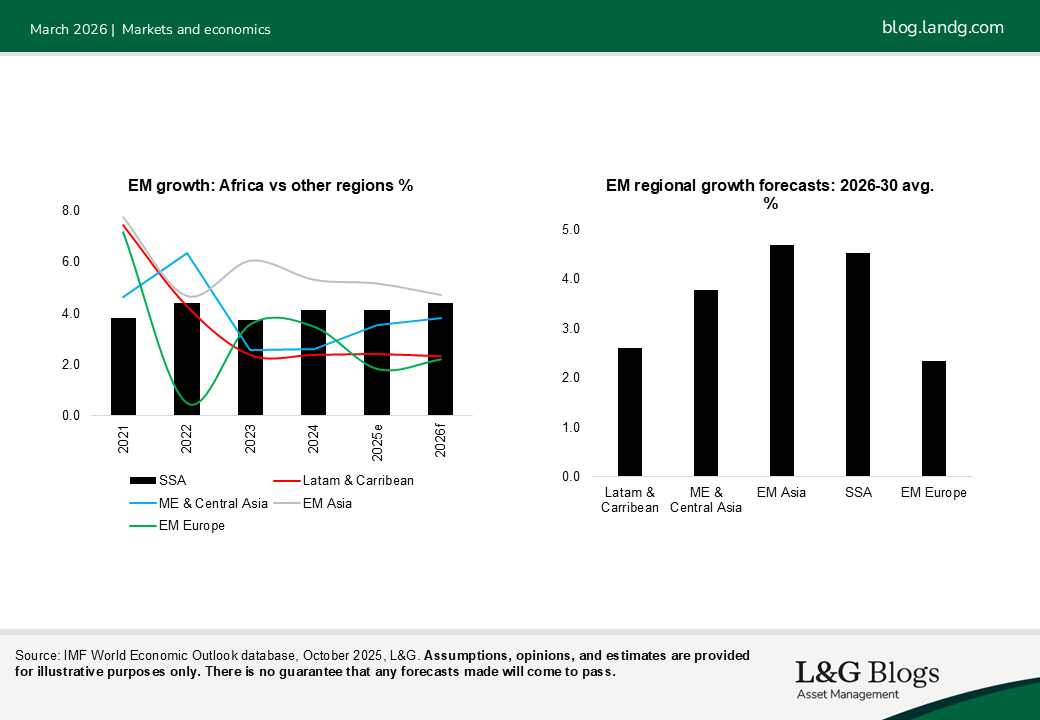

- Resilient, strong growth: barring EM Asia, where growth is driven by external demand, SSA’s real GDP growth has outpaced all other EM regions over the past few years. We believe this dynamic could persist over the near term, with growth averaging close to EM Asia levels. This historical performance came regional vulnerabilities to climate change, conflicts, coups and external shocks in the form of tariffs, retrenchment of bilateral aid and volatile commodity prices.

Underpinning these buoyant dynamics are several factors in our view, notably an expanding middle class, which has nearly tripled since 1980 to 313 million and is expected to triple again by 2060.[3] This expansion reflects both higher population growth rates aided by improving health outcomes, and a rapid pace of urbanisation. Indeed, as Africa’s population increases from 1.5bn in 2025 to 2.5bn by 2050, the number of Africans living in urban areas is projected to double to 1.4bn by 2050.[4]

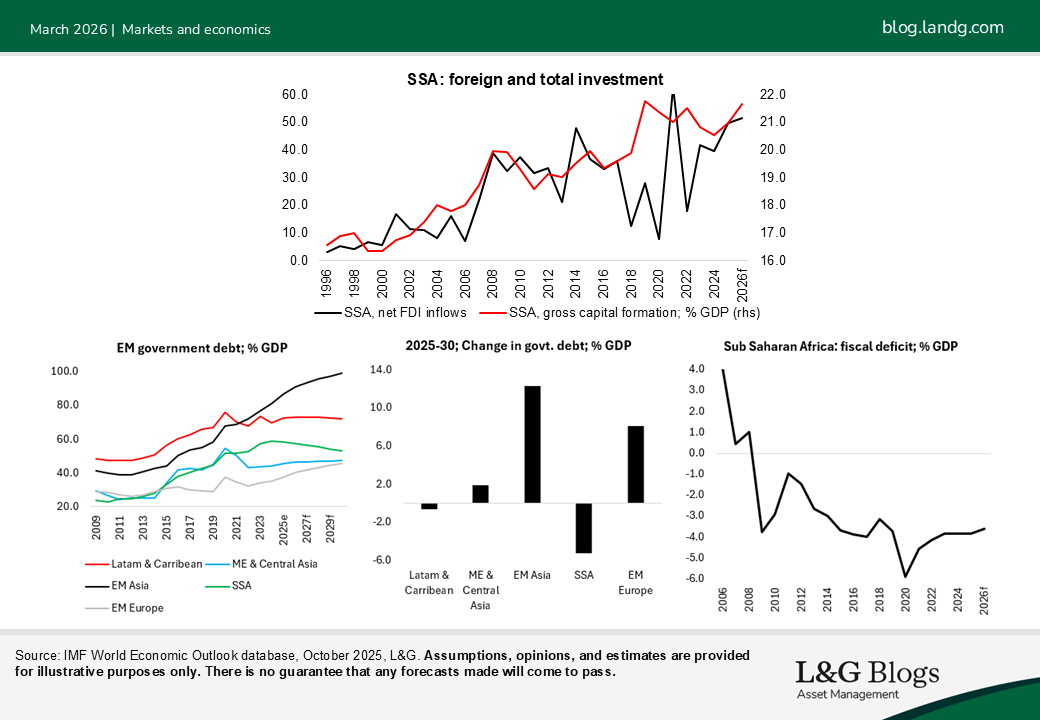

- Inflows: That investors may be recognising the potential this represents is not just reflected in the market welcoming increase Eurobond issuance out of SSA, but also in higher levels of domestic and foreign investment.

- Declining debt: Investors, however, do not invest in a vacuum. Helping anchor investor expectations is not just strong growth levels but also improved macroeconomic outcomes. One area where this is reflected is in improved fiscal dynamics: SSA is the only EM region expected to see declining debt ratios in the near term on the back of the most sustained pace of fiscal deficit reduction in at least two decades.

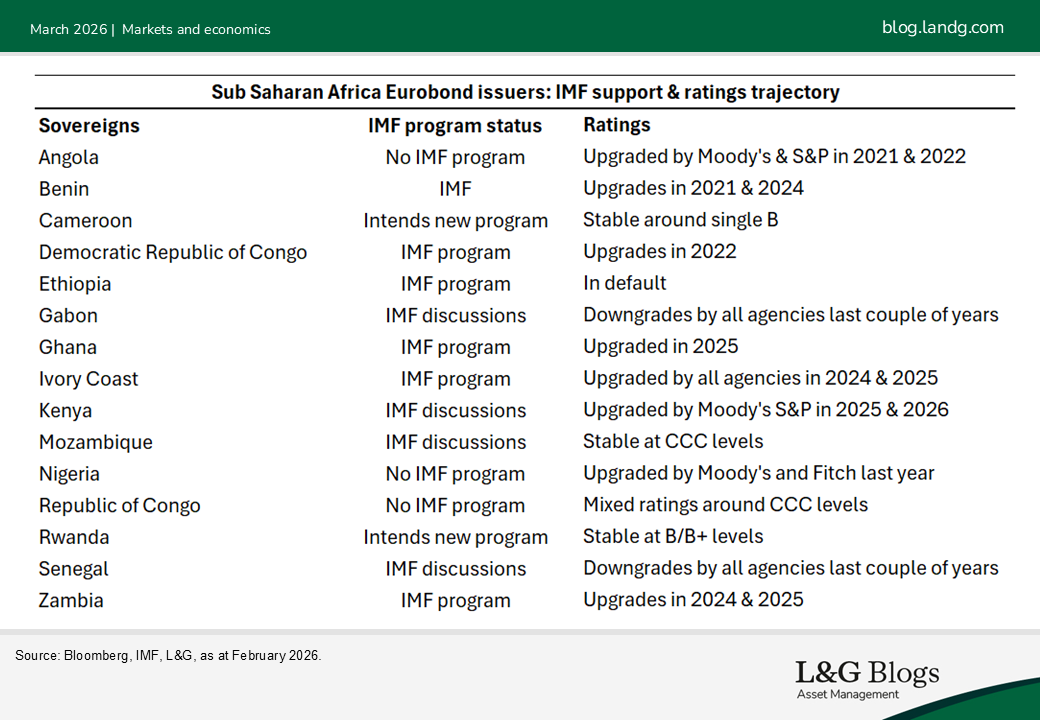

- Prudent policy: These macroeconomic outcomes and investor expectations are anchored by IMF engagement that ensures prudent policy making. The sustained nature of this engagement is delivering rating upgrades across the continent.

- Geopolitical clout: Enhanced investor interest and the investment case is also underpinned by SSA’s growing geopolitical importance. Coupled with its natural resources, Africa’s location close to Europe, the Gulf and Asia make it critical in the global focus on critical minerals for the West and China, energy security for Asia and Europe and food security for the Gulf countries.

The investment opportunity in SSA is not just about diversifying portfolios. It is multi-faceted.

Some investors will be drawn by exposure to some of the world’s fastest-growing countries, to economies rich in agriculture, diverse natural resources, and critical minerals at a time of unprecedented geopolitical focus.

Other will be drawn to countries where demographics enhance prospects of technological leapfrogging, fintech adoption and digitalisation, or simply to economies that are improving credit stories.

[1] It should be noted that diversification is no guarantee against a loss in a declining market.

[2] https://odi.org/en/insights/critical-minerals-critical-moment-africas-role-in-the-ai-revolution/

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.