Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Q2 2026 Asset Allocation outlook: Adapting to uncertainty

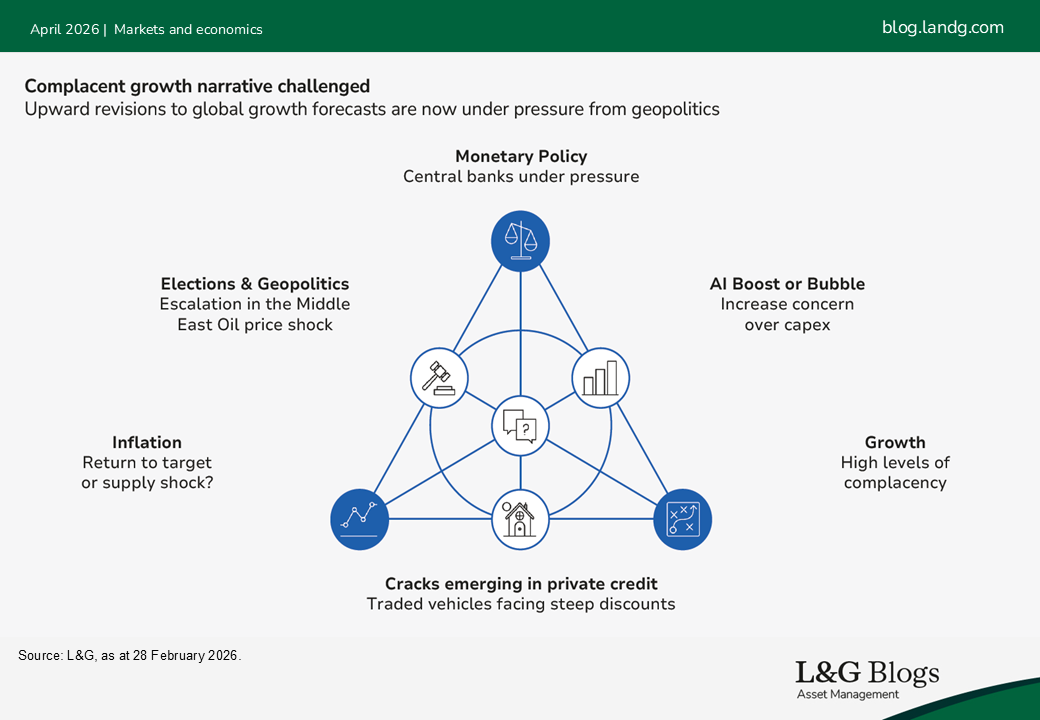

The conflict in the Middle East has raised profound and unsettling questions about geopolitical and commodity market stability.

The following is the introduction to our Q2 2026 Asset Allocation outlook

Investor attention remains firmly on the Strait of Hormuz and the implications of its recent closure for the global supply of oil, gas, and fertiliser. Bond and equity markets have started to worry about an inflation shock reminiscent of that seen in 2022 or, for those with longer memories, the twin oil crises of the 1970s.

However, it is important to remember the very human tendency to overstate the challenges of the here and now. “May you live in interesting times” is often quoted as an ancient Chinese proverb. It’s not.

Instead, it comes from a speech by a British politician at the end of the 19th century. The fuller quote highlights the recency bias which makes it difficult to place things in their appropriate historical context: “We are living in most interesting times … I never remember a time in which our history was so full … of new objects of interest, and new objects for anxiety” (Joseph Chamberlain, 1898).

Commodity prices intensify concerns

When investing, we need to fight the kneejerk tendency to always worry about ‘new objects for anxiety’ and instead focus on the implications of recent events for the fundamentals. Trying to forecast the outcome of the conflict is inherently difficult. However, the sharp backwardation in major commodity markets (i.e. prices in the near future being significantly higher than prices in the distant future) points to a time-limited interruption to global energy supply. Calibrating ‘time-limited’ is the key challenge.

As an asset allocation team, we came into this conflict significantly underweight credit in our dynamic funds. We have long held the view that the market offered thin compensation for credit risk. However, the market was lacking a catalyst for worrying about downgrade and default risk. No longer. Commodity prices add to the nascent concerns on both artificial intelligence (AI)-related disruption and the potential vulnerability of some private credit providers to the software sector.

Holding the line on the dollar

Our biggest changes over the quarter have been on equities and duration. Supply shocks have the potential to upend the negative correlation between equity and bond returns that helps mitigate risk in multi-asset portfolios. Accordingly, we reduced duration in the early days of the conflict moving from a positive tilt back to neutral. On equities, geopolitical flashpoints typically resolve in higher prices after an initial period of distress. Towards the end of the quarter, we judged that distress to be sufficient to upgrade our score from neutral to positive.

On FX markets, we were reluctant to embrace the pervasive negativity on the US dollar in the second half of last year. Among other things, that drove us to be underweight emerging market local debt. We haven’t seen sufficient position-squaring yet to change that view. The conflict has been a reminder that the greenback remains a safe haven currency under times of stress. When markets stabilise, almost certainly return to the fore, but that is a debate for another day.

In focus this quarter

The usual update on the macro landscape from Tim Drayson, our Head of Economics, discusses how high energy prices have unsettled what looked like a calm year for growth. Our capital markets assumptions article from John Southall, Head of Strategic Research and Dash Tan, Quantitative Associate introduces our quantitative dynamic tilting framework that uses valuation and risk signals to tilt portfolios.

Finally, we have two pieces that unpick the logic behind some of market’s new favourite acronyms: TPA and HALO.

Chris Teschmacher, Fund Manager and Head of Asset Allocation Specialists dives into the debate on the advantage of adopting a Total Portfolio Approach when managing assets. Robert Griffiths, Global Equity Strategist and Patrick Greene, Strategist, dig into the logic underpinning the equity market’s recent obsession with Heavy Asset Low Obsolescence companies and sectors that are likely to be somewhat immune from disruption to their business models.

I hope you enjoy the articles my team has put together for this quarter, and they provide you with useful insights for your client conversations.

Read our Q2 2026 Asset Allocation outlook

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.