Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

London calling: Why London’s industrial real estate market remains a capital choice

While returns since 2022 have been a little underwhelming, we believe there’s now a compelling case for London’s industrial real estate assets.

Dipping into the sector

Multi-let industrial real estate in London – that is estates of small industrial units occupied by a variety of small businesses, household name trade park operators, and urban logistics firms – delivered terrific returns over the 10 years to June 2022. Total returns were 19.2% p.a. relative to All Property’s 8.5%, according to MSCI, and within this was rental growth of 6.3% p.a.[1].

The last few years, however, have been less compelling. The 2022 correction hit lower-yielding industrial hard while higher rental values exacerbated concurrent occupier affordability challenges. Namely, the 2022 energy crisis pushed producer price inflation to almost 25%[2].

As a result, capital values of London multi-let industrial fell by ~30% in less than a year and remain 24% off 2022 peaks[3]. There are now renewed concerns over input costs given the energy price spike amid the ongoing conflict in the Middle East.

This point on occupier pressures has led to greater investor scrutiny. There has been concern that rents have been pushed too far for too many, choking off growth potential and even risking occupier solvency. Last year’s confirmed business rate revaluation added to these worries. A vacancy rate almost doubling from 6.2% in 2021 to 12.1% this year[4] has been cited as a symptom of this.

A focus on rents

So where are rents now? Since 2010, London multi-let industrial values have grown 19% more than neighbouring South-east locations and 80% more than Scotland[5] - something of a laggard in this sector.

In real terms, however, rental values are still only around where they were in the late-1980s. This is not to claim that there is unrealised ‘value’ in the sector, but does weigh against more sensational reporting.

We also know that rental performance correlates highly with vacancy (85% correlation with an r-square of 71% over 20 years). We are confident that all-time low levels of development activity, coupled with an occupier market that seems more confident to transact now the 2025 budget is firmly in the rear-view mirror, will bring this vacancy significantly lower – and we believe this will happen soon.

Meanwhile, yields of 5.4% remain 205bps higher than they were in early 2022[6] which, coupled with a more modest but still outperforming rental growth expectation, positions expected returns for London multi-let industrial ahead of the All Property average.

A structural approach

Despite expected cyclical improvements, we think the more interesting story is structural:

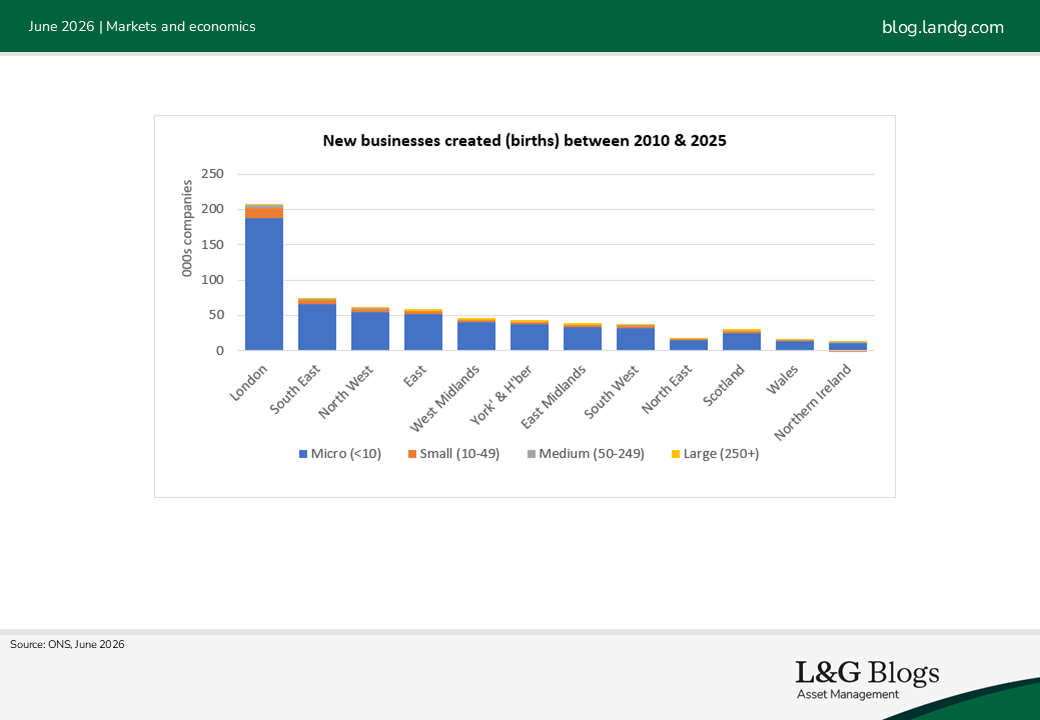

1. New business creation: Real estate investors are always well-advised to invest where demand grows organically rather than relying on occupiers moving around when leases expire. Across all business types, London has created 206,000 businesses over 15 years; 180% higher than the next strongest region and representing roughly a third of all net new business growth in the UK since 2010[7]. Not all these occupiers require industrial property, but the dominance of SMEs within these growth statistics aids confidence in the London occupier story.

2. Population and economic growth: Greater London’s population of 9.0 million is expected to grow to 10.3-10.5 million by 2050. There are 3.4 million households in London, expected to grow to 4.3m by 2050. London’s GDP per capita is £69,000 compared to a UK average of £39,000. This additional population and income supports e-commerce spend, housing renovation, and demand for other services provided by multi-let industrial occupiers[8].

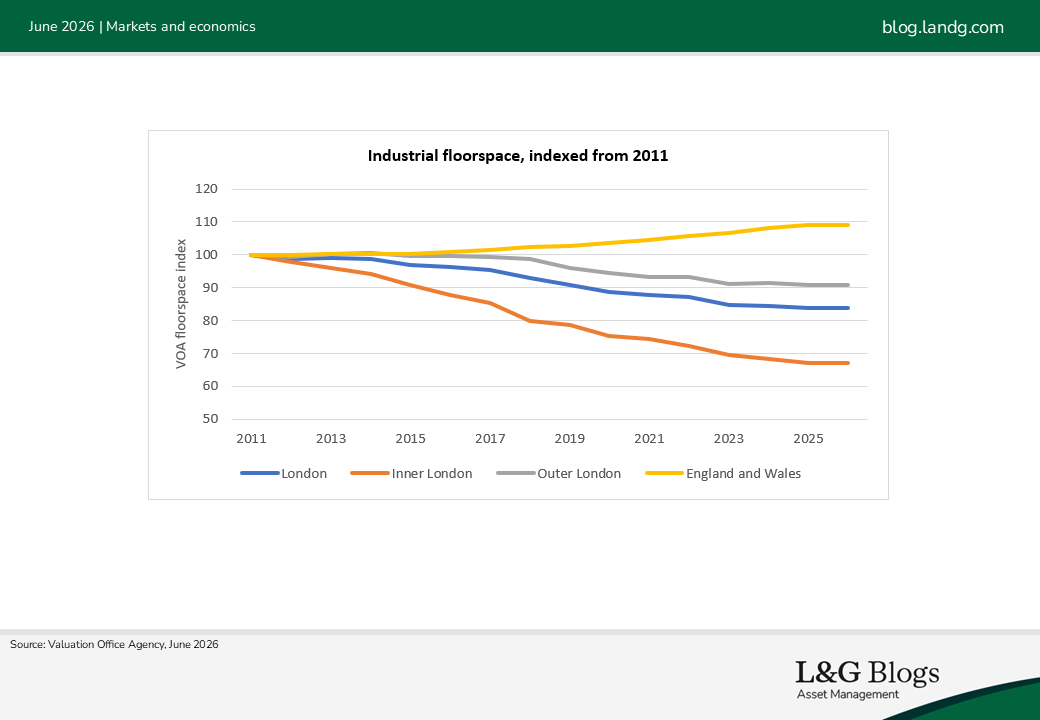

3. London industrial stock has fallen significantly: Valuation Office Agency numbers suggest a 33% decline in Inner London floorspace since 2011 and 9% in Outer London, compared to 9% growth across England and Wales. At 210 million sq ft, there is 62 sq ft of industrial floorspace per household in London. Without development this would be 49 sq ft by 2050.

4. Development: Across the UK multi-let industrial market development is at an all-time low. London’s situation is exacerbated by perpetual pressure on land from housing, despite the GLA’s best intentions, and economic rents – the rents required to make development viable – at levels which challenge occupier affordability.

5. Megatrends: Industrial is well positioned to benefit from the intersection of global structural change: decarbonisation, digitalisation, deglobalisation and demographics. We believe this is particularly true of sustainable urban logistics formats serving growing digital-savvy populations.

We see three clear strategic implications of the above trends:

1. London is not one market: Vacancy rates and starting yields vary widely across boroughs. Comparing the two can give clues to mispricing – for instance markets with a relatively low current vacancy and high starting yield look well placed to outperform compared to the opposite. Tilting portfolios to these geographies, enabled by on-the-ground expertise, may be a potential way to maintain a London exposure with greater growth potential.

2. Asking prices: Although we are less concerned than many about rental levels, both in real terms and as a proportion of occupier costs, a competitive advantage can emanate where quality development can be created at an economic rent under prevailing asking prices. This is possible through advantageous off-market site selection and acquisition and experience in delivery across the supply chain.

3. Overspill: In 2022, the gap between asking prices in London and the wider South East was the widest it has ever been at 22%. This supported a strategy of ‘occupier overspill’ – i.e., capitalising on displaced London occupiers by providing cheaper space in markets 10-20 miles outside the city. We believe this remains valid but has faded. The rental gap has narrowed over the last two years and, when fuel and other mileage costs are considered, the overall costs savings to a logistics firm still serving inner London may become more negligible.

In conclusion, although we acknowledge recent cyclical pressures, we believe these are broadly in the past. We expect near-term outperformance to strengthen and, longer term, we remain confident in London’s ability to grow demand. All this means we believe experienced, well-connected investors with granular local knowledge are well-placed to capitalise on potential opportunities.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass.

Past performance is not a guide to the future.

[1] MSCI Quarterly Digest Q1 2026. Past performance is not a guide to the future.

[2] ONS PPI measure

[3] MSCI Quarterly Digest Q1 2026

[4] Ibid

[5] Ibid

[6] ibid

[7] ONS data as at May 2026

[8] Data sourced from ONS and GLA as at May 2026

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.