Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Clean power: A market in transition

Clean power infrastructure has moved beyond simply “build more renewables”. The sector is now driven by a more complex interaction where dispersion is rising by country, by technology, and by contract structure. Here, expertise is increasingly rewarded, and specialist underwriting is critical.

Navigating power market divergence

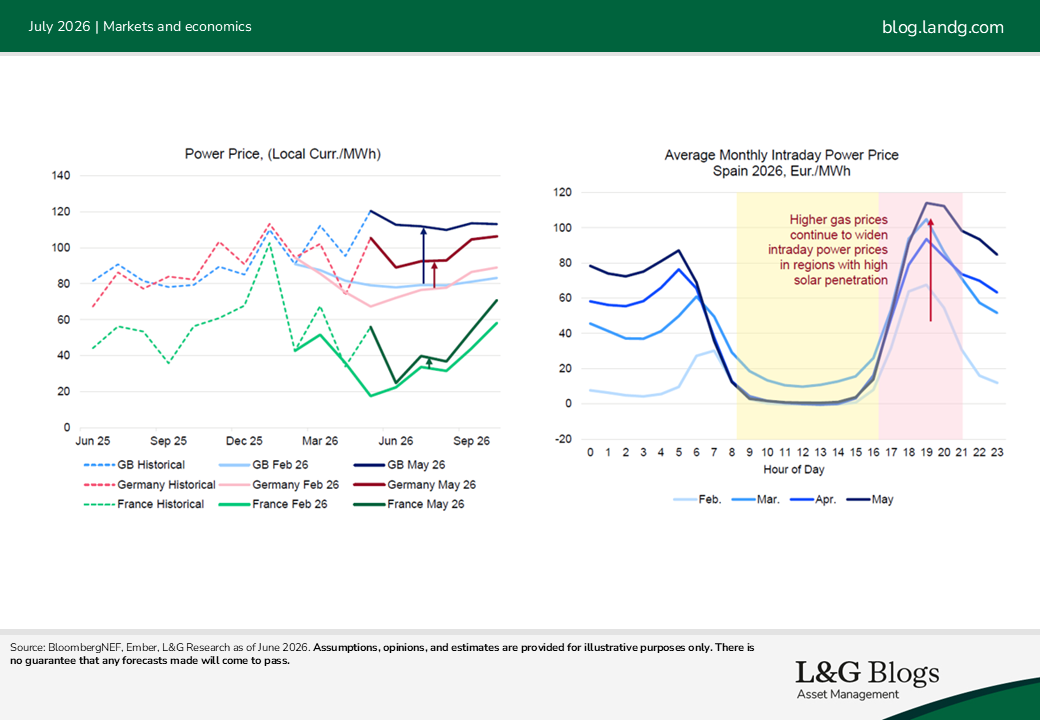

European wholesale power prices have achieved a relative stability on a rolling yearly basis over the last two years. Rising volatility, however, still resides underneath.

Solar capture rates have fallen in several markets as rising penetration has compressed midday power prices.[1] Wind has been more resilient with a more evenly distributed generation profile. Early 2026, however, did show cold conditions affecting Nordic assets, highlighting growing climate impacts on investment returns.

The war in the Middle East has led to a higher cost of gas, lifting forward power prices most in markets where this energy source frequently sets the power price, such as the UK and Germany. This is less pronounced in nuclear-heavy France.

This dynamic selectively supports merchant renewables: wind, batteries and hybridised[2] assets should benefit more than solar assets, in our view. The war has also raised the strategic need for European energy security independent of any de-escalation scenario.

The levelised cost of electricity (LCOE) is still declining, but at a slower pace. Batteries are expected to see the fastest cost reductions, supporting hybrid projects. Elsewhere, gains for wind and solar are becoming more incremental.

With financing costs still elevated, future LCOE improvements may depend more on cost of capital, and returns increasingly dependent on power market conditions. Battery buildouts are more incentivised as LCOE falls and power price volatility rises, which we expect could lead to benefits for solar assets as the ‘duck curve’ (see above) [3] is more effectively smoothed.

Negative pricing is becoming more common as rising intermittent renewable supply coincides with softer demand and limited grid capacity. We see this as challenging for merchant solar, but supportive for batteries. We still see potential opportunities for capital deployment into solar assets, but these are more market-selective and increasingly need expertise.

Daily price spreads have risen through 2026 to-date, improving the economics of battery storage. As intraday spreads widen and falling battery capex enables development, storage is becoming a larger share of installed capacity. Market selection remains critical, however, since an oversupply of storage can arbitrage away revenues.

Forward markets also highlight forecasting challenges. Early 2025 curves overestimated summer 2025 prices. Conversely, the war shock pushed later forward curves higher. These point to a widening of the range of potential outcomes for renewable assets and may increase the equity risk premium required for merchant assets.

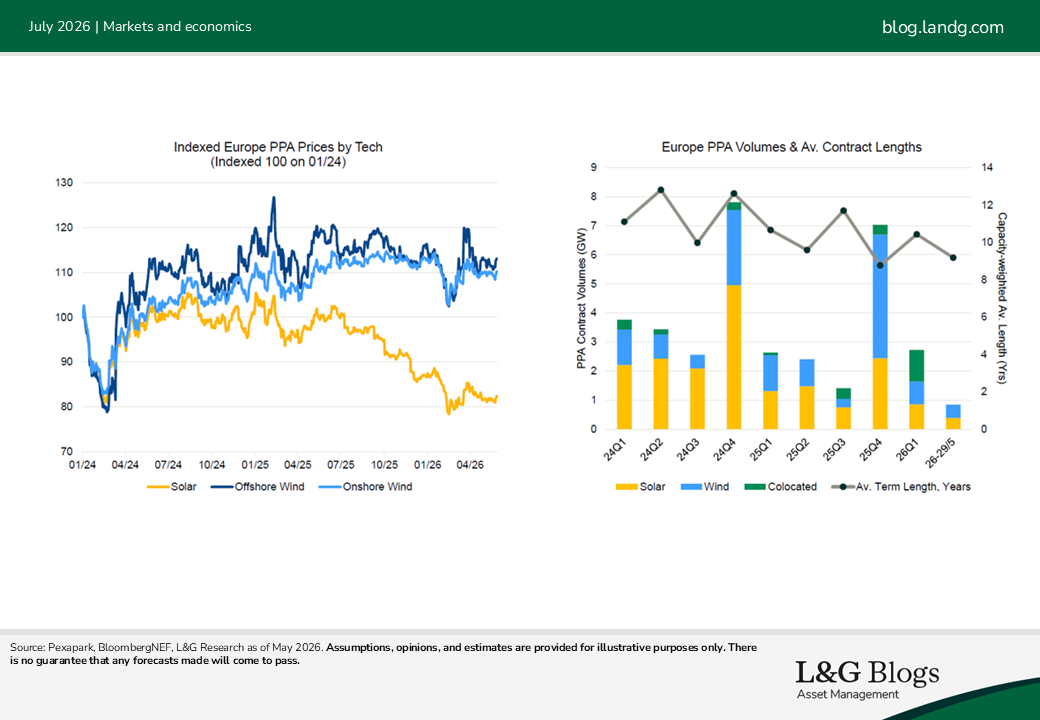

Power purchase agreement (PPA) markets reflect these dynamics. Solar PPA prices fell through 2025, while wind prices were more resilient. PPA volumes for solar have softened, and average contract lengths have shortened, suggesting buyers and sellers are less confident in long-term price forecasts.

The role of governments

Government-backed auctions remain central, in our view, to clean power investment, particularly as merchant power price visibility declines. If merchant prices remain volatile, or are insufficient to support new-build economics, then auctions and incentives will become more important to sustaining investment in renewables.

Recent auctions show strong demand for long-term contracted cashflows, with indexation returning and hybridisation rising. EU efforts to reduce reliance on Chinese clean-tech supply chains may raise project costs and with them auction prices. In Germany, strong competition in onshore wind auctions has pushed prices towards low-case LCOE levels, potentially compressing project returns. In the UK, recent auctions have been more supportive, though we see grid challenges potentially impeding the development of those assets.

Regulatory intervention following the war in the Middle East has so far been relatively limited. The EU’s response has focused on targeted and temporary measures rather than major new funding.

The UK has raised the Electricity Generator Levy from 45% to 55%, reducing upside for merchant-exposed generators. The impact on base-case investment returns, however, appears limited for well-hedged portfolios and assets with power-price forecasts below the levy threshold. It has also proposed a scheme to move eligible low-carbon generators onto fixed-price contracts, reducing merchant exposure and providing cashflow stability.

Importantly, both the UK and EU continue to implement the merit-order market design[4], likely reducing a tail risk for investors.

The entry environment

Recent returns show the market adjusting. EMEA renewables returns dipped in Q3 2025, linked to weaker capital growth as solar capture rates fell and realised prices disappointed versus forwards. Returns recovered in Q4, suggesting cannibalisation risks may now be better reflected in valuations.

Listed renewables funds have also repriced. Appraisal-based discount rates inflected upward towards the end of 2025, while market-implied discount rates rose as listed funds traded at discounts to NAV.

We see these market-implied rates as reflecting both higher risk-free rates and a higher market-implied equity risk premium. At the same time, take-private activity has continued at meaningful premiums to listed prices, offsetting public market discounts and suggesting to us that private investors still see long-term value in the asset class.

Capital deployment

The clean power market is becoming less homogenous. In our view, the winners will not simply be ‘renewables’ broadly, but strategised combinations of market, technology, contract and grid position.

Solar may be challenged where cannibalisation is worsening, yet attractive where risks are now priced. Wind appears more resilient. Batteries are structurally supported, but only where power price spreads persist.

We believe capital deployment will increasingly reward expertise. The sector still has powerful long-term drivers: electrification, data centre demand growth, energy security, and decarbonisation. However, underwriting must now be more granular.

In this environment, certainty has value, flexibility has value, and market and technology selection matters more than ever.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass.

Past performance is not a guide to the future.

[1] Solar is strongly supplying more of the power demand but only does so during periods of the day with sufficient sunlight. The low marginal cost of solar production leads to lower power prices.

[2] Clean power generation assets with collocated battery storage.

[3] The U-shaped intraday power curve shown in the Intraday power price figure that results from high solar penetration lowering midday power prices.

[4] The merit order ranks power plants by cost, with the last plant needed to meet demand setting the electricity price.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.