Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Is tokenmaxxing the strongest signal yet for AI demand?

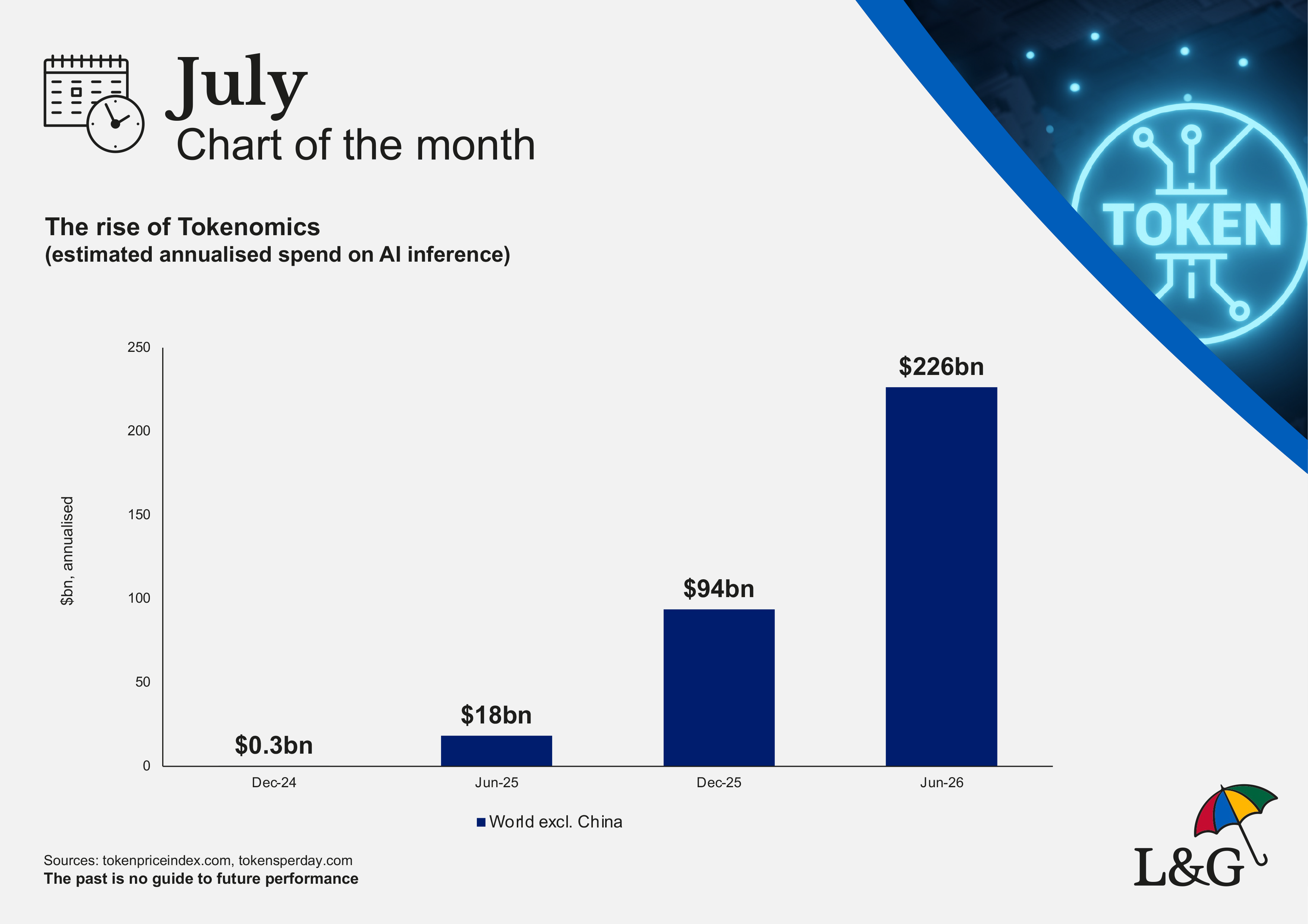

For July’s chart of the month, we explore the rise of tokenomics. We look at the incredible growth in direct artificial intelligence (AI) revenues in the last 18 months and ask whether it’s enough to justify the huge capital expenditure that is underway.

Total enabling capital expenditure for the AI revolution is set to be somewhere in the region of $8 trillion over the next six years[1]. That includes compute, data centres, power infrastructure and industrial supply chains. Expenditure on that scale can only be justified if someone is willing to pay to use the underlying technology. On conservative assumptions[2], AI model providers need to generate around $2.5 trillion of revenue per annum by 2030 to pay back that investment.

Is that plausible? One way to tackle that is to ask how much is already being spent, and how rapidly it’s growing. To do that, we dig into the world of tokenomics.

Tokens are the units of data that an AI model processes. Every time you ask Claude to help with writing code, or ask ChatGPT for directions, you are consuming tokens. Tokens are used when AI models digest inputs provided by users, and again when AI models produce outputs for users. As a rule of thumb, 750 words in plain English text constitutes 1000 tokens.

China’s AI ecosystem is separate from the rest of the world, so we consider the world ex-China for this exercise. In the last couple of years, global token consumption outside of China has exploded to a mind-bending 300 trillion per day[3]. The price charged for processing each token has drifted higher to an average cost of $2 per million[4].

If we combine the volume of tokens used and the unit cost, we can get a handle on the total revenues now accruing to the providers of AI models as shown below.

Current revenue looks like it’s running at over $200 billion annualized, a tenfold increase since mid-2025. There's no sign in the numbers yet of the shift away from ‘tokenmaxxing’ or the incorporation of cheaper models making a dent in revenues. As a consistency check on those numbers, we note that Anthropic*[5] reported annualized revenue approaching $50 billion in May 2026. It feels plausible that Anthropic constitutes a quarter of the total market as things stand.

To reach $2.5 trillion by mid-2030 requires compound annualized growth rates of 80% per annum over the next four years[6]. That sounds like a high hurdle rate but, consistent with the standard S-curve of new technology adoption, it would be a sharp slowing from the 500% annualized growth rate of the last six months. We’ll be following these numbers closely: we believe tokenomics is likely to be as important as economics in determining the market outlook over the months and years ahead.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] Tracking Trillions: The Assumptions Shaping the Scale of the AI Build-Out | Goldman Sachs

[2] 5-year useful life of the capital goods being deployed, 15% internal rate of return, 50% gross margins.

[3] Tokens Per Day · the AI inference demand index

[4] AI Token Price Index

[5] Anthropic raises $65B in Series H funding at $965B post-money valuation \ Anthropic

[6] Source: L&G and Bloomberg as of 30 June 2026. Past performance is not a guide to the future.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.