Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Investors want heavy assets, low obsolescence industries…

…but they’re not all the same.

The following is an extract from our Q2 2026 Asset Allocation outlook.

A rush into real world, asset intensive businesses has helped lift the FTSE 100, but defensiveness is far from guaranteed. Structural competition, geopolitical tensions and uneven earnings prospects reveal a more complicated landscape than the physical versus digital narrative suggests.

Investors unsettled by the pace of AI-driven disruption are increasingly seeking refuge in businesses tied to physical assets and real world processes. The logic is intuitive: tangible goods are harder to replicate or automate than software or data. But this instinct can be misleading.

AI is only the latest in a series of forces that have reshaped markets over the past two decades, and in many goods producing industries the most profound disruption has already come from China. Autos are the clearest example. Chinese manufacturers have not just undercut Western peers on cost; they have done so while delivering electric vehicles that are technologically sophisticated, well designed, and increasingly competitive on quality. The assumption that lower prices necessarily imply inferior products no longer holds.

That contrast matters when investors think about where genuine defensiveness lies. Some sectors are far less vulnerable to this kind of competitive leapfrogging. Copper production, for instance, remains capital intensive, geographically constrained, and slow to scale; features that make it difficult to disrupt through either AI or industrial overcapacity alone.

The broader point is that ‘physical’ does not automatically mean ‘safe.’ Investors should distinguish carefully between industries where barriers are durable and those where they are illusory. Adding to the complexity is the ongoing conflict in the Middle East, which introduces uncertainty around energy prices, transport routes, and input costs. While some producers may benefit from reduced competition, others face margin pressure from higher costs, and the duration of these effects is unknowable. In an environment shaped by multiple, overlapping disruptions, caution is warranted when seeking shelter that may not actually exist.

A resurgence in the FTSE 100, but how durable will it be? At the regional level, one of the clearest beneficiaries of this recent trend in markets has been the UK equity index. For the best part of two decades, the FTSE 100 has lagged as investors have sought exposure to asset-light businesses, tech and services. UK equities have long been overweight asset heavy sectors such as commodities, utilities, and goods, such as consumer staples. As investors have looked for refuge from AI-related disruption, the FTSE 100 has outperformed the Nasdaq by around 10% over the last 3 months and the Euro Stoxx 50 by around 5%.[1] Could this signal a durable period of UK outperformance?

There’s no question the UK is well positioned to weather a period of commodity-induced stagflation fears, but there’s also no escaping the reality that the UK market continues to offer an inferior growth profile than almost all its peers.

For 2026 and 2027, EPS growth is expected to be a couple of percentage points slower than Europe, and about 5 percentage points slower than the US next year.[2] The sustained FTSE 100 outperformance in the first decade of 2000s was driven by the emergence of the Chinese economy, which created huge commodity demand, and by the bubble-fuelled run in the UK’s financial companies. No comparable drivers seem present this time. A period of less concentrated equity performance is something which those engaged in active investment management almost all welcome. But like all narratives, the new paradigm of asset heavy, non-US assets itself faces vulnerabilities.

The hyperscalers are transforming

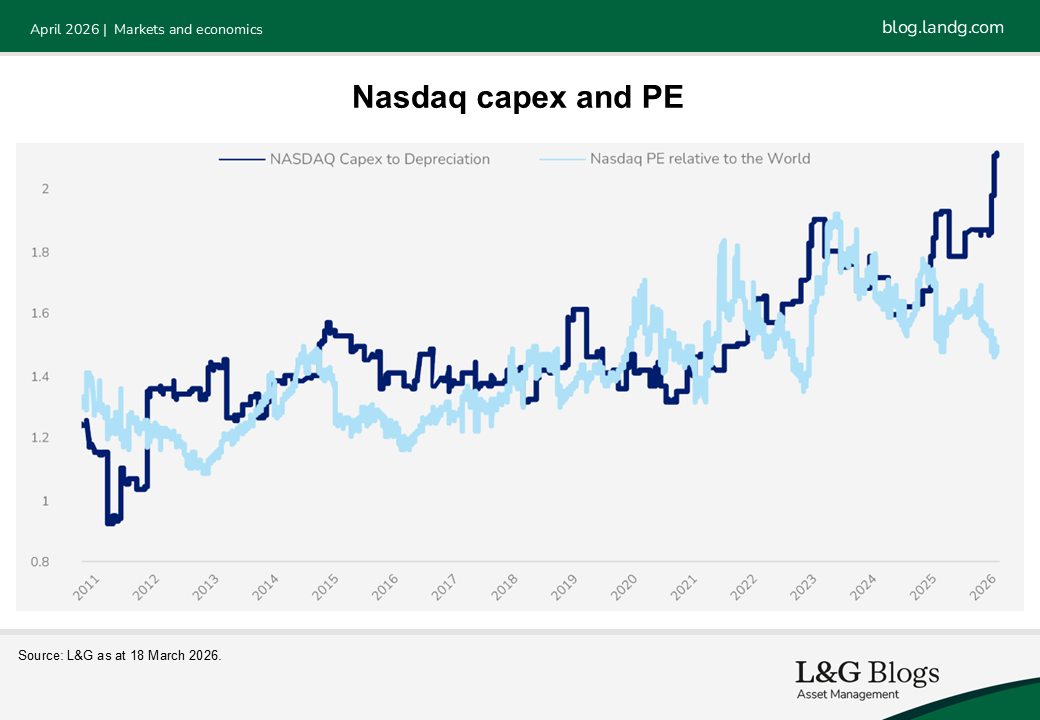

And that brings us to a final observation about the current equity market phase. There is one group of businesses that are working hard to transform their businesses from a relatively asset-light operating model, to something much more asset heavy: the US hyperscalers.

US tech’s capex to sales ratio has risen to 11%, up 4 percentage points since 2022.[3] Their competitive moats are no longer just the quality of their software or advertising reach, but sheer computing capacity, rooted in physical datacentres and the energy and cooling infrastructure required to power them. It’s a fascinating transformation. But it’s one which, to date, the equity market remains somewhat sceptical of. From around the third quarter of 2025, when the hyperscalers upsized their capex plans meaningfully, investors have sought to shift away from these businesses, ironically buying asset-heavy businesses elsewhere at just the moment the companies pivoted in this direction.

We continue to believe in the transformational power of AI, and in the businesses who will deliver that transformation. We lifted our exposure to the AI universe this quarter, taking advantage of the continued malaise in their share prices, despite ongoing strong earnings delivery.

The above is an extract from our Q2 2026 Asset Allocation outlook.

[1] Bloomberg as at 18 March 2026. Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

[2] Bloomberg as at 18 March 2026.

[3] Bloomberg as at 18 March 2026. Key risks: The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested. Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.