Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Global economic imbalances and AI: few signs of concern

The key talking points around artificial intelligence (AI) have been on company earnings, the impact on inflation and medium-term labour market effects. Less discussed are the signs of unsustainable macroeconomic developments.

Key takeaways

|

Investors wonder whether AI is in a bubble and if it all will end in tears, but this tends to be in the context of rapidly rising stock prices. We look at AI traces in the macro economy and ask whether imbalances are starting to build. However, even if we can spot vulnerabilities, identifying the timing and nature of any adjustment remains extremely difficult.

Growth without excess

Growth is clearly affected by the AI boom. This is most visible in Taiwan which has grown by 12.5% over the past year[1]. Korea with a much more diversified production base is growing 1.3 percentage points (ppt) above its 10-year average[2] and Goldman Sachs estimates that AI is boosting US growth by 0.3ppt[3] . However, strong growth rates on their own do not augur a recession down the road; for that, one typically needs excessive investment.

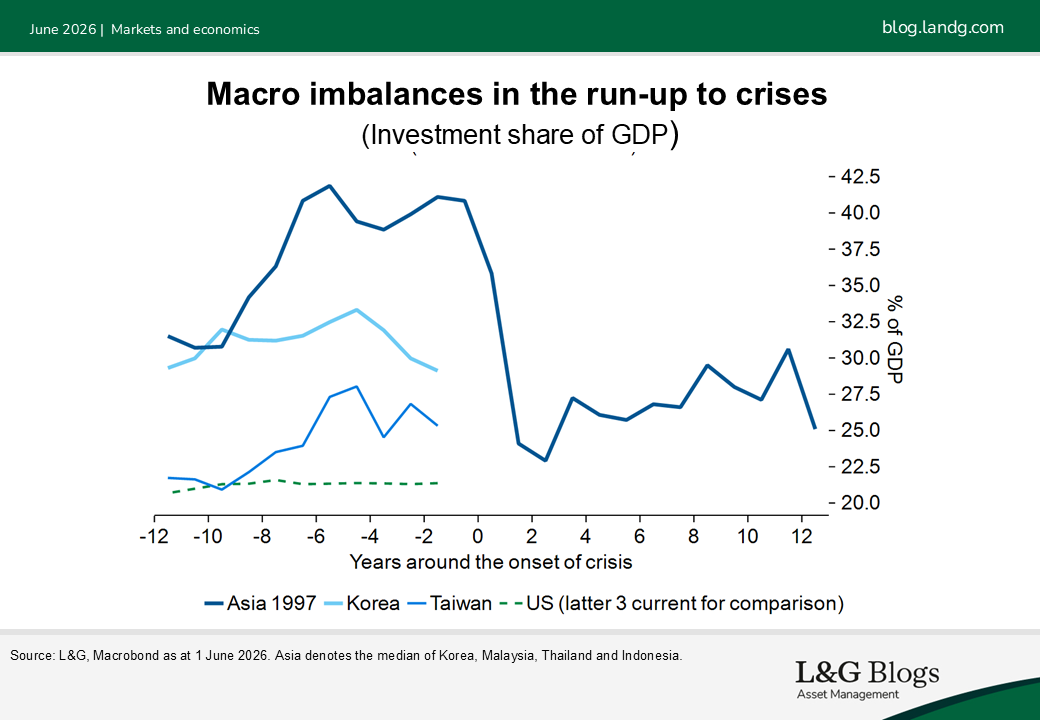

An investment overhang is far from evident in macro aggregates. Gross investment has moved sideways in the US and, if anything, is falling in Taiwan and Korea (Figure 1).[4] Compare that to the investment boom in the run-up to the Asian financial crisis. Of course, there could be pockets of overinvestment that do not show up in macro aggregates, given large increases in AI infrastructure.

The AI boom could have some impact on inflation. The median DRAM price is up 200% in 2026. Four items in the US CPI basket are directly affected by this, namely new cars, computers, smartphones and video/audio devices. Using the respective DRAM share in production costs and CPI weights, we find that DRAM prices could boost US inflation by 0.5ppt. This demand-side shock, we believe, should be more benign than the recent energy shock.

Few signs of macro imbalances

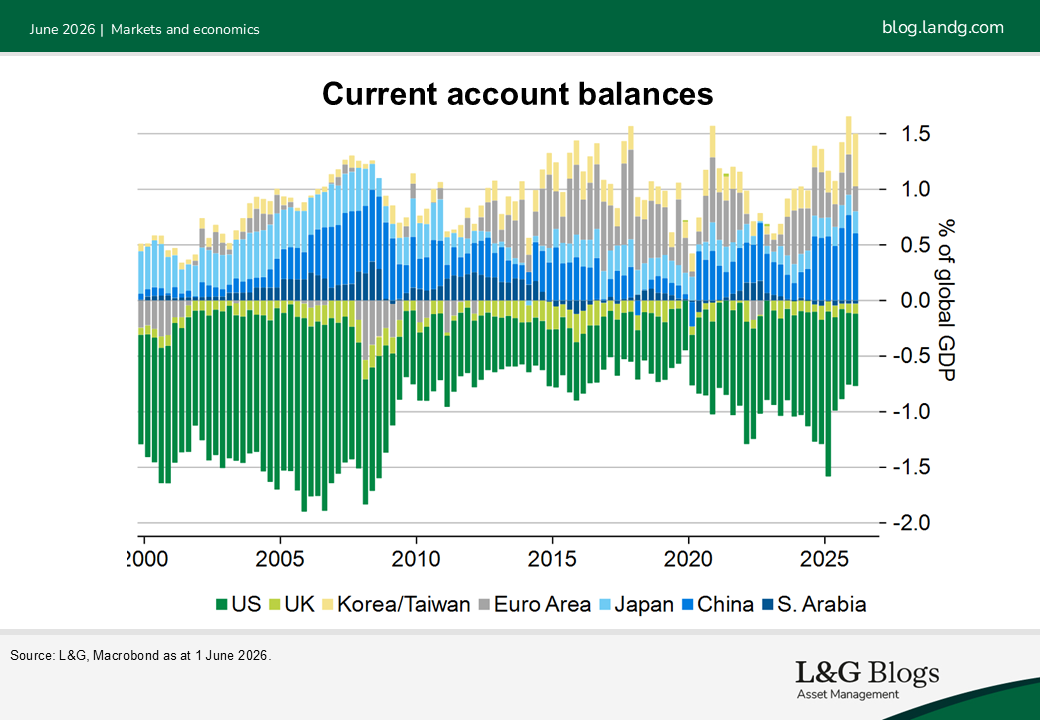

To date, the biggest effect of AI is seen in current account balances. The latest readings show both Taiwan and Korea running surpluses amounting to a whopping 25% of GDP. Taken together their current account surplus starts to rival China’s.

This has led commentators to compare the current situation to the run-up to the global financial crisis (GFC).[5] That run-up, labelled Bretton Woods II by a group around David Folkerts-Landau, was characterised by large Chinese current account surpluses. Chinese dollar proceeds were recycled back into US treasuries thereby keeping the exchange rate stable and the US external deficit elevated. This time, some believe, profits of Taiwanese and Korean chip producers are recycled back into US hyperscalers leading to a merry-go-round that is bound to collapse at some stage.

This is not a narrative we agree with. Take Korea, large current account surpluses are indeed mirrored by large capital outflows, but it is foreigners taking their money out, presumably to rebalance their equity portfolios, rather than Koreans investing abroad. In Taiwan, the offset to large surpluses are receivables, trade credits and deposits, meaning that most of the money hasn’t even arrived or is parked in FX deposits.

The contrast to Bretton Woods II becomes even clearer if we look at global imbalances (Figure 2). In the years leading up to the GFC, large surpluses were mirrored by US deficits close to 2% of global GDP. This time around, the US is running a modest deficit of 0.7% of global GDP. The next largest deficit is that of the UK at 0.1% of global GDP, meaning that counterparts to large AI surpluses are well diversified throughout the world. This makes sudden adjustments less likely.

In sum, we find few signs of macro imbalances caused by the AI boom. Of course, they could still build in the future and this does not give an all clear on recessions. The dotcom bubble did not create macro imbalances and still caused a recession when it burst. However, at this stage, the AI boom is unlikely to end in a deep, balance-sheet recession akin to the Asian financial crisis, the GFC or the European debt crisis.

Assumptions opinions and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass. Past performance is not a guide to the future.

[1] Macrobond. Data as of 1 June 2026.

[2] Macrobond. Data as of 1 June 2026.

[3] Wall Street Journal, 26 May 2026

[4] Data through Q1 2026 for the US and Q4 2025 for Taiwan and Korea.

[5] Bloomberg 21 May 2026, Circular AI Boom Goes Global as Asia Windfall Funds Hyperscalers.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.