Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

GDP hallucination

AI could have a profound impact on GDP and productivity. But will it show up in traditional macro indicators?

Key takeaways:

|

Artificial intelligence is distorting America's most-watched economic number in multiple directions and it is extremely difficult to estimate the effect in real time. Building AI models could make GDP look bigger and more durable than the underlying value justifies. Using them probably makes real GDP look smaller than the value people actually get. The result is strong business investment that overstates how solid today's growth is while understating how much better off AI is making us.

Neither is a glitch. Both follow from what GDP measures — market output, at market prices when it changes hands. Ultimately economists care about producer and consumer surplus (the latter is the value of everything we consume). We love our apps and AI will create loads more for “free” which are not part of GDP. Broadest of all is happiness, but let’s not get into the Easterlin Paradox or the liabilities from social media and cybercrime here!

Building the models flatters the number

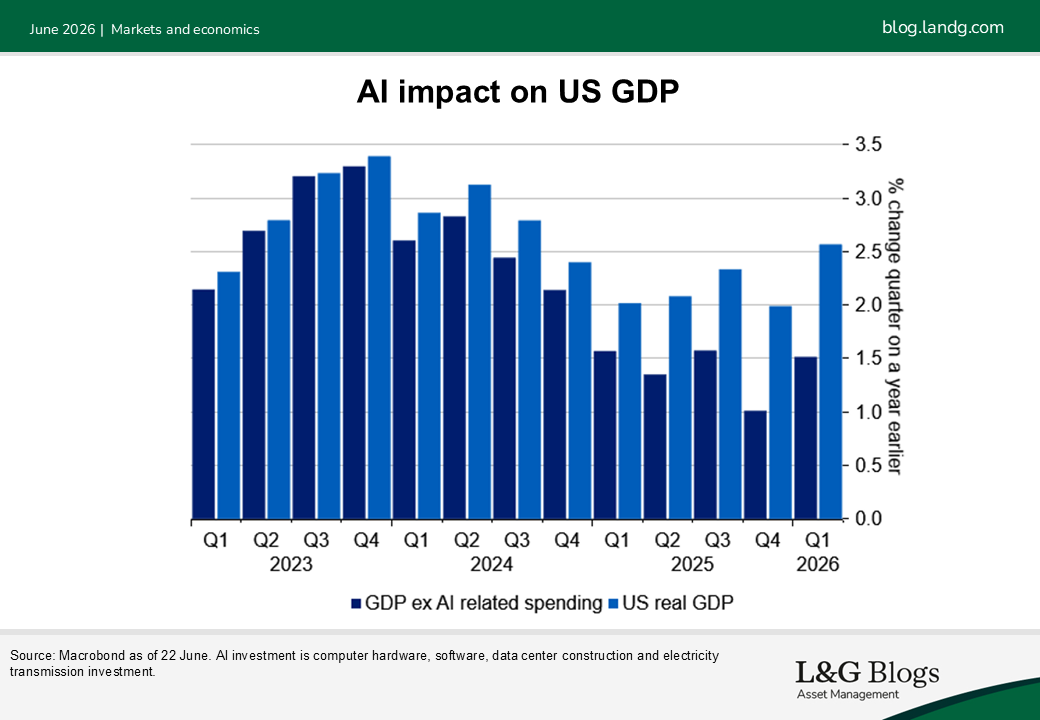

The scale of investment is staggering. By broad definitions (including all software), AI-related capital spending now runs near 5% of US GDP, a share KKR* likens to the late-1990s tech boom. Epoch AI puts data-center, compute, and networking investment alone at roughly 0.8% of GDP in early 2026. If we exclude imports, AI capex has added around one percentage point to US GDP growth over the last year.

This narrow growth driver could be a problem. Because data centers employ few people once running (relative to a hospital or factory), the usual chain from investment to jobs to wages to spending is weak, so a strong headline can mask a softer economy. Much of the hardware is imported, and imports subtract from GDP, so gross capex overstates the domestic contribution.

Statisticians must also decide whether money spent developing a model is investment or an intermediate input. GDP is a measure of value added which subtracts intermediate consumption. To avoid double counting, one way of measuring it is to calculate total spending on final goods and services. But this is smaller at present compared to the cost of the AI infrastructure build out and is reflected in the negative earnings from the model developers.

Also, because AI is changing rapidly, it can become obsolete quickly. Assuming overly long asset lives mismeasures depreciation and the capital stock. However, older semiconductors can still be used for inference, so perhaps their usefulness can be extended even if no longer used for frontier models.

The subtlest issue is price. Real GDP is nominal output divided by a price index, so if the deflators don't track AI's plunging cost per unit of capability, real growth is understated. This is not new. The late-1990s computing boom produced exactly this worry: the 1996 Boskin Commission concluded that the Consumer Price Index overstated inflation by about one percentage point a year, largely by failing to capture quality improvements and new goods. Overstated inflation means understated real output. AI is that same quality-and-novelty problem the Boskin Commission flagged, now at potentially greater scale and speed.

Finally, GDP counts spending whether or not it pays off. Is the vibe coding and token spend producing anything useful? Will a chunk of this buildout prove to be an overbuild? The late 1990s fiber optic cable glut is the obvious parallel. AI enthusiasts retort the problem today is a lack of compute so we should worry less about overinvestment.

Using the models hides the value

Flip to the demand side and the distortion reverses: most of the value never touches GDP. This is the old "free goods" problem — search, maps, Wikipedia — supercharged. Stanford's 2026 AI Index estimates US consumer surplus from AI tools reached about $172 billion a year by early 2026, up from $112 billion a year earlier, with most tools still free — dwarfing the few billion in actual AI revenue, because the benefit flows to users, not income statements. GDP only sees the revenue and misses the surplus.

AI features bundled into existing products at unchanged prices register as no extra output. When free tools displace paid software or services, measured GDP can fall even as welfare rises. Value migrates into unpaid household tasks which GDP already ignores. The internet enabled searches for holidays that previously travel agents were paid to source. Now AI is likely to help with tax returns and contract drawing, reducing the cost and measured output for basic legal and tax advice.

Why it matters

Without good GDP statistics, inferences about productivity become meaningless – a key barometer of whether there will be a societal return on all the AI investment.

The Peterson Institute has a huge upper bound estimate of the GDP distortion of 4 percentage points last year. Their work highlights some of the quality adjustment problems, but their figure massively exaggerates the effect because they are capturing intermediate inputs rather than GDP. There are also distributional concerns. If AI shifts income from labour to capital, output can climb while the median worker's experience diverges.

The statisticians are aware of the shortcomings but are always struggling to keep up with changes in the economy. New Federal Reserve Chair Kevin Warsh has launched five taskforces, one will focus on data. Perhaps this will draw on Brookings's "Counting AI," and the Stanford Digital Economy Lab's proposals like "GDP-B". These all aim to build complementary gauges. But flaws will remain. Initially AI might score as a cost and only when firms identify how to use it effectively and re-organise will we see the benefit in productivity.

In the meantime, central banks will analyse the labour market and a range of other surveys and alternative data sources to assess the economy’s speed limit when taking interest rate decisions. They might not talk much about GDP!

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.