Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

From capex boom to transmission risk – AI and portfolio resilience

With AI linkages to equity and credit markets deepening, how can portfolios respond to concentration, valuation and operational risks?

AI is reshaping industries, and it’s also reshaping capital markets.

The Bank of England (BoE)’s December 2025 Financial Stability Report[1] highlighted stretched equity valuations – especially in AI‑focused names – and noted that debt‑funded infrastructure is deepening connections to credit markets and increasing interdependence.

At the same time, public bond markets have absorbed roughly $300 billion a year in AI and data centre financing, and analysts expect high grade credit spreads to be modestly wider in 2026 as capex-driven net supply builds, underscoring how deeply the AI buildout is woven into broader credit markets.[2]

How does this affect how investors should think about portfolio resilience? We believe the answer may lie in multi‑dimensional diversification.[3]

Stress‑testing valuations

Recent analysis illustrates the optimism embedded in current pricing.

At the company‑specific level, HSBC’s* analysis of OpenAI* suggests that even assuming billions of users and over $200bn of annual revenue by 2030 cumulative free cashflow could remain negative, leaving an estimated $207bn funding gap by 2030.[4]

J.P. Morgan* estimates that achieving a 10% return on AI capex through 2030 would require ~$650bn of annual revenue in perpetuity – around $35/month from every current iPhone user worldwide – framing the scale of monetisation needed to validate today’s investment pace.[5]

Goldman Sachs* argues that US equities are priced for a long‑term AI capex boom; if long‑term growth expectations revert to early‑2023 levels, they estimate 15-20% downside from multiple compression alone.[6]

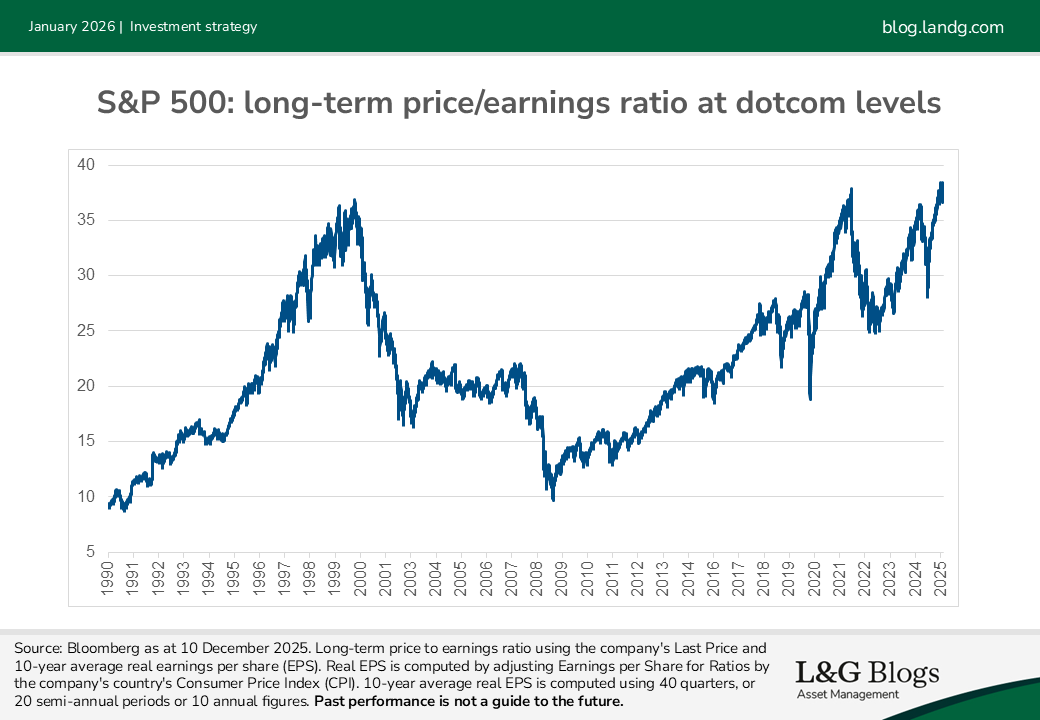

The chart below shows the long-term price-to earnings-ratio is now comparable to that seen during the dotcom era of 2000.

This isn’t a call for doom; it’s a reminder that even powerful themes can travel a bumpy road. What feels steep (or modest) today may prove ordinary once business models and utilisation rates become clearer.

Prepare, don’t predict: illustrative pathways

“Far more money has been lost by investors preparing for corrections than has been lost in corrections themselves.” – Peter Lynch

That admonition isn’t a licence to ignore risk; it’s a reminder to frame it. In markets where equity leadership is concentrated, financing is interconnected, and capex is rewriting credit supply, preparation highlights mapping transmission channels rather than trying to time the turn.

This is not a forecast, but one way that stress could travel if optimism fades:

- Equities: A capex reset like that described by Goldman Sachs* could drive multiple compression, with growth‑heavy leaders underperforming.

- Credit: AI‑linked issuance concentration could widen spreads in a risk‑off turn, especially at longer maturities as markets digest ‘lumpy’ supply

- Rates: A slowdown may extend duration demand but would interact with term premia and fiscal dynamics, as flagged by the BoE

- Market plumbing: Circular financing structures could transmit stress across suppliers, cloud platforms and private credit, amplifying moves

Themes behind the theme

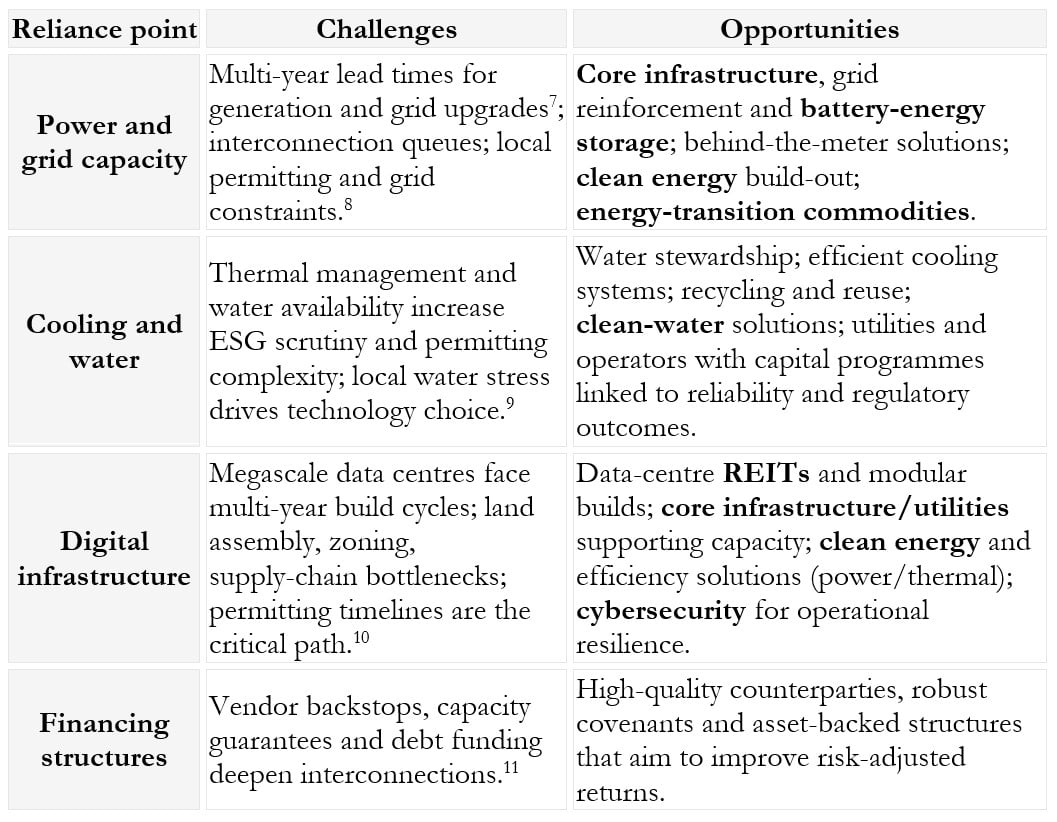

To approach AI with resilience, break the industry into its operational components.

Several points of reliance in the AI buildout map directly to investable themes, creating avenues for contracted, long‑duration cash flows while highlighting potential execution risks.

Multi‑dimensional diversification

In an era of concentrated leadership and systemic leverage, diversification across multiple dimensions may help manage risk.

- Asset classes: Blend equities, fixed income, real assets and alternatives to avoid single‑path dependency.

- Sectors: Balance technology with industrials, healthcare and utilities – all potential beneficiaries of AI‑enabled productivity and capex spillovers

- Regions: Pair US exposure with Europe, Japan and emerging markets to mitigate index concentration

- Liquidity profiles: Combine listed markets with private allocations (infrastructure, housing) to smooth path dependency

- Risk premia: Add quality, value and low‑volatility tilts to offset growth concentration and reduce drawdown sensitivity

Asking the right questions (and a timely memo)

The AI revolution is here, but its path remains unknown. Howard Marks’ new memo – Is It a Bubble? – is timely because it separates bubbles in company behaviour (excessive spending, overbuilding, unrealistic operational expectations) from bubbles in investor behaviour (excitement and speculation, FOMO and valuations that assume perfection).

His central message is uncertainty: none of us can know which firms will be the long‑term winners.[12]

It’s a reminder that transformational technologies can change the world without every investment around them becoming a winner; many innovations were funded by bubbles.

The conversation around AI will keep evolving, and we believe diversification belongs at its centre.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

Sources

[1] Source: https://www.bankofengland.co.uk/financial-stability-report/2025/december-2025

[2] Source: JP Morgan’s 2026 Outlook

[3] It should be noted that diversification is no guarantee against a loss in a declining market.

[4] Source: https://www.ft.com/content/23e54a28-6f63-4533-ab96-3756d9c88bad

[5] Source: https://www.ft.com/content/59133fa3-3071-47b4-8761-c6922d07c34e

[6] Source: https://www.aol.com/finance/ai-inevitable-slowdown-comes-could-103851543.html

[7] Source: https://about.bnef.com/insights/commodities/power-for-ai-easier-said-than-built/

[8] Source: https://impact.economist.com/projects/the-solutionist/power-brokers

[9] Source: https://www.bloomberg.com/news/newsletters/2025-05-08/thirsty-ai-creates-another-climate-risk

[10] Sources: BNEF and Economist articles cited above.

[11] Sources: https://www.bankofengland.co.uk/financial-stability-report/2025/december-2025 and https://investors.coreweave.com/news/news-details/2025/CoreWeave-Closes-2-6-Billion-Secured-Debt-Financing-Facility-Strengthening-Market-Position-as-AI-Cloud-Leader/default.aspx

[12] Source: https://www.oaktreecapital.com/docs/default-source/memos/is-it-a-bubble.pdf?sfvrsn=d4a92866_3

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.