Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Private credit goes public: What are BDCs telling us about market conditions?

In this blog, we dive into some of the headlines around BDCs and look at what the broader message for debt markets might be.

Private credit has grown significantly over the past decade, becoming an established and important complement to public markets. The asset class spans a broad spectrum of strategies and risk profiles, from investment‑grade private lending to higher‑yielding middle‑market direct lending. This article focuses on the latter. Business Development Companies (BDCs), which specialise in middle‑market lending, represent a distinct subset of the private credit universe and provide one of the few real‑time, market‑based indicators of investor sentiment and underlying credit conditions in this segment.

Recent developments, including the widening of BDC bond spreads, discounted equity valuations, and rising redemption activity, suggest investors are becoming more cautious about private credit fundamentals. We view these signals as worth watching closely.

What are BDCs?

BDCs trace their roots back to the 1980s, but their modern relevance stems from the period following the 2008 Global Financial Crisis. In the wake of the GFC, banks faced tighter capital and regulatory constraints and so retrenched from lending to small and mid‑sized companies. That gap was increasingly filled by non‑bank lenders.

BDCs emerged as a key conduit for this financing. They provide capital to private, middle‑market US companies that lack access to public bond markets or traditional bank credit. Over time, as bank retrenchment persisted, BDCs became a core pillar of the private credit ecosystem.

Publicly listed BDCs are closed‑end vehicles with permanent capital, meaning shareholder activity takes place in the secondary market and does not directly affect the capital base of the BDC itself. Alongside these, perpetually non‑traded BDCs, which offer periodic liquidity through controlled redemption mechanisms have grown rapidly in recent years. It is these have recently drawn attention, with several reaching their contractual withdrawal limits. Both publicly listed and non‑traded BDCs are subject to public filing disclosure requirements which means they offer one of the clearest public windows into the opaque world of private credit.

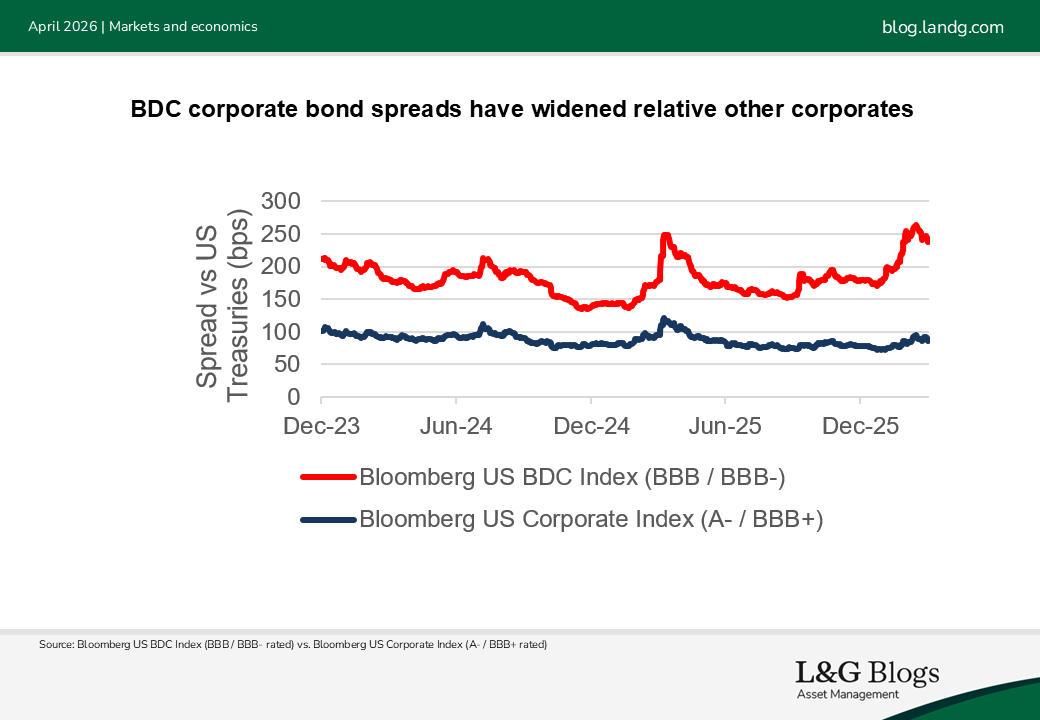

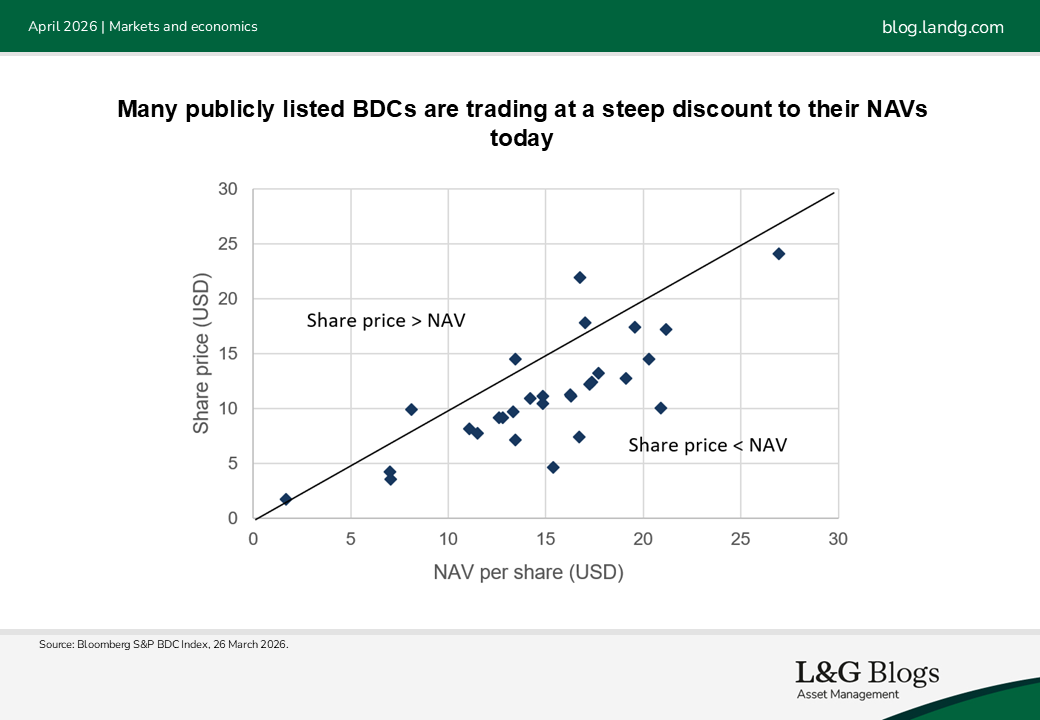

Recent market moves have been striking. BDC bond spreads have widened meaningfully, materially underperforming investment‑grade credit more broadly. At the same time, many publicly traded BDC equities are now trading at deep discounts to reported net asset value.

A key driver of this repricing has been exposure to software and technology‑related borrowers. Software is a core sector for BDC lending, reflecting its historically stable cash flows and asset‑light business models. However, the rise of generative AI has added a new dimension of disruption risk, particularly for lower‑quality, highly leveraged software issuers with limited pricing power.

While it is too early to point to evidence of AI‑related credit deterioration, any signs of disruption will be closely watched for over the next several quarters. More broadly, some credit quality indicators are beginning to soften for BDCs. Non‑accrual rates (loans on which borrowers have ceased paying interest) are edging higher, though from historically low levels following the COVID-era stimulus.

At the same time, the use of payment‑in‑kind (PIK) interest has risen as some borrowers defer cash interest by capitalising it into loan balances. The uptick in PIK interest is largely concentrated in smaller borrowers, though some larger companies have also opted for PIK structures, often result of competitive underwriting rather than outright distress.

Finally, Net Investment Income (NII) coverage of dividends is also weakening though this appears to be driven primarily by lower base rates, given that BDC portfolios are predominantly floating rate.

The regulatory framework, and why it matters

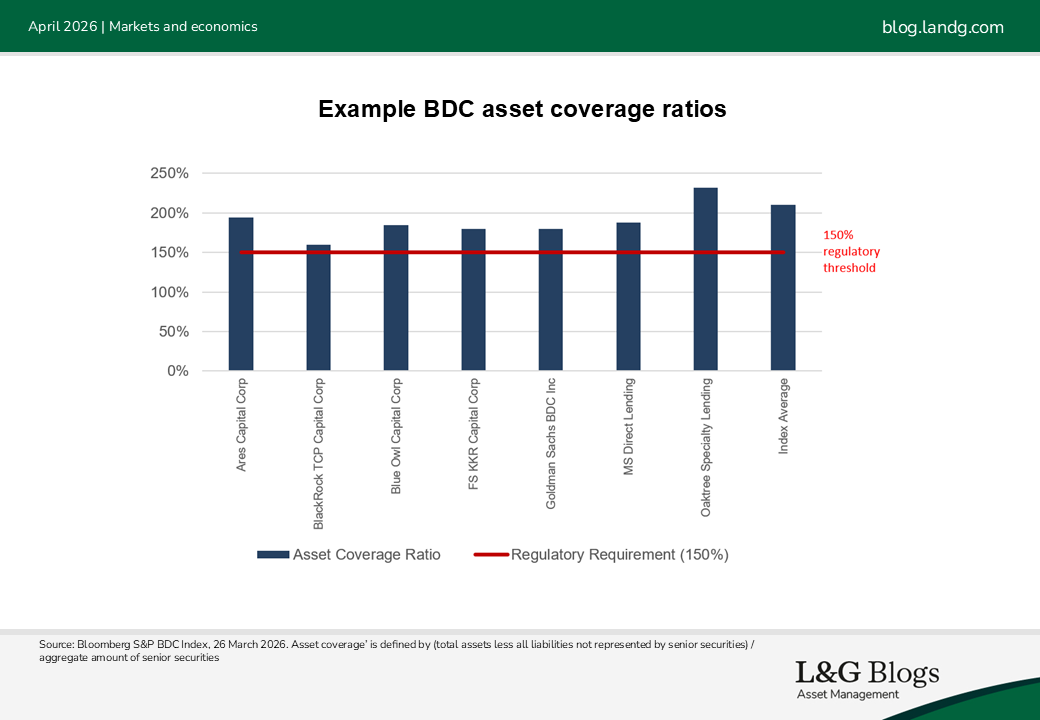

BDCs operate under a defined regulatory regime. A central feature is the statutory minimum asset coverage ratio of 150%. In simple terms, this limits leverage to roughly 2x debt‑to‑equity. Importantly, if a BDC breaches this threshold, it cannot issue new debt, it cannot pay dividends, it must deleverage or raise equity and it loses its tax status.

The average asset coverage ratio across the BDC bond universe is currently well above this minimum – in excess of 200% – providing a meaningful buffer for bondholders. These constraints act as an automatic stabiliser, forcing early balance‑sheet repair rather than allowing leverage to compound unchecked.

Why are BDCs capping withdrawals?

Recent headlines around redemption caps have unsettled markets, as several semi-liquid BDC structures have limited investor withdrawals to their contractual 5% quarterly cap. It’s important to emphasise that these gates are design features, not signs of distress. They exist to protect remaining investors by preventing forced asset sales from inherently illiquid portfolios. In that sense, the enforcement of these caps can be viewed as a credit-positive mechanism. However, their activation is nonetheless a meaningful signal: it reflects growing investor caution around valuation uncertainty, portfolio composition, and the resilience of underlying private credit assets under stress.

Conclusion: A signal worth watching

BDCs do not represent the entirety of the private credit market, but they remain one of the few areas where public markets continuously price risk. The combination of wider bond spreads, discounted equity valuations, and gated redemptions all point to a market that is reassessing risk. Private credit is a very broad asset class, and strong underwriting discipline and proactive risk management will drive differentiated returns, while investment grade assets are generally more insulated from downside risk.

Recent signals do not imply a systemic problem with private credit, nor does it suggest that BDCs themselves have fundamental issues. Rather, BDCs provide a useful early barometer, particularly for the middle-market direct lending segment, reminding investors to be attentive to signals that may indicate late‑cycle credit risk.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass.

Past performance is not a guide to the future.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.