Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Prepayment dynamics in a bifurcated agency MBS market

What do mortgage lock‑in and the composition of the universe mean for prepayments and convexity? We consider the implications for investors

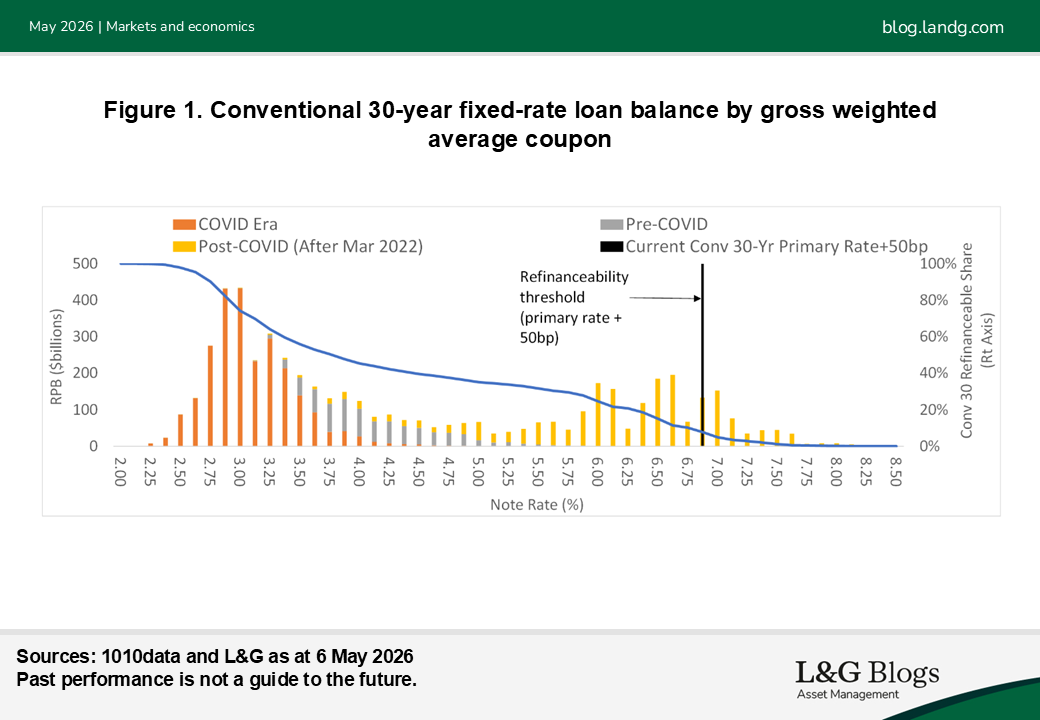

The steep decline in mortgage rates during the COVID-19 era, followed by the sharp rates selloff that began in 2022, has bifurcated the agency mortgage-backed securities (MBS) market. As shown in Figure 1, the loan universe now primarily consists of two cohorts:

1. a very large cohort of low-coupon, out-of-the-money (OTM) loans originated during the COVID-19 era, and

2. a much smaller (but growing) cohort of loans with higher note rates originated since the Federal Reserve began hiking interest rates in March 2022.

The remainder of the outstanding balance consists of a relatively small cohort of loans originated prior to the COVID-19 era (shown in grey in Figure 1).

COVID-19 era pool issuance is concentrated in 2s and 2.5s, with smaller balances in 1.5s and 3s. By contrast, post-COVID-19 era issuance is concentrated in 5s-6.5s, although builder buydowns have generated some supply in lower coupons.

At today’s[1] rate levels, refinancing risk is largely confined to the high-coupon, post-COVID-19 era loans because rates are relatively less likely to fall enough from current levels to push low-coupon bonds into the refinanceable window. Meanwhile, for deep-discount bonds, slower-than-modelled prepayment speeds[2] and extension risk remain the key focus.

Lock-in could pressure discount speeds for years

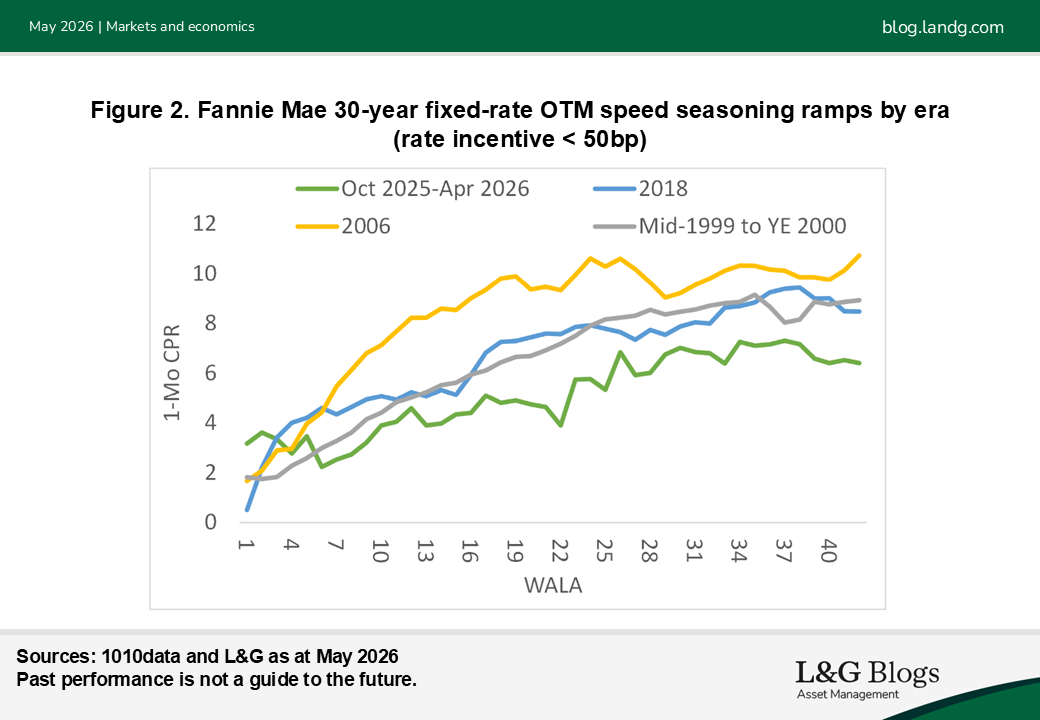

With primary mortgage rates in the mid-6s area, a large share of outstanding loans are deep out of the money, i.e., these borrowers have no incentive to prepay their mortgage loans for any reason. These borrowers are said to be ‘locked in’ to their existing mortgages, because they have a strong incentive to delay moving or extracting equity, both of which would require giving up a below-market interest rate. Similarly, it is uneconomical for these borrowers to curtail their loans. The current level of aggregate rate disincentive has not been seen in more than 40 years.

Extreme lock-in has pushed discount speeds to their lowest level in decades. Figure 2 shows ‘seasoning ramps’ (prepayment speed as a function of weighted average loan age) on out-of-the-money collateral. The chart contrasts recent behaviour (green line) with earlier periods. The chart shows that speeds on out-of-the-money collateral have been running several percentage points slower than in the past.

This is especially noteworthy given the strength of the housing market and the broader economy. Strong home price appreciation, significant accumulated equity, and a stable labour market would typically support speeds on discount collateral. In recent years, however, these factors have been less influential as the lock-in effect has dominated.

Lock-in should gradually dissipate as pent-up demand and necessity lead people to move. Turnover is in part, driven by life events including marriage, divorce and the birth of children. But it is difficult to predict how long it will take for turnover speeds to climb back to more historically typical levels. Absent a major rates rally, it could take several more years for discount speeds to normalise.

Refinancing risk is limited for now, but speeds could surge in a major rates rally

Turning to the high coupons, refinancing risk remains contained at current rate levels as most borrowers remain outside of the refinanceable window (see Figure 1). With primary mortgage rates in the mid-6s area, only 6.0s and higher coupons are in the refinanceable range. But there are two caveats that investors should keep in mind:

1. The reactivity of the mortgage universe has increased – or in prepayment modeling parlance, S-curves have steepened. Technological advances, including the proliferation of artificial intelligence in the loan origination process and the rise in the market share of fast non-bank servicers, have played a role in increasing the reactivity of the universe when rates rally.

2. Post-COVID-19 era borrowers have been waiting on the sidelines for years. Theses borrowers are eagerly awaiting an opportunity to refinance into a lower rate. Speeds are likely to reach multi-decade highs if primary mortgage rates were to fall below 4%. Moreover, a major rally would likely trigger the ‘media effect’ – a surge in refinancing speeds beyond what can be explained by rate incentive alone when rates fall to a historic low or breach some psychologically significant level. As advertising and lender solicitations pick up and borrower awareness of refinancing opportunities expands, speeds can accelerate even on very seasoned or burned-out collateral.

Mitigating call and extension risk

Investors can achieve a more favourable convexity profile versus the to-be-announced (TBA) market by selecting well-priced bonds in the specified pools market. In contrast with the TBA market which provides generic mortgage market exposure, the specified pools market allows investors to select actual bonds with the desired prepayment profile. Specified ‘story’ bonds typically offer attractive prepayment characteristics compared to generic collateral. Popular stories include loan balance, credit, and ‘geo’ bonds – which are backed exclusively by loans from certain states, most notably, New York, Florida or Texas.

Alternatively, investors can consider call-protected collateralised mortgage obligation classes, or less negatively convex bonds in the private-label market (such as non-qualified mortgage bonds), trading convexity for credit risk.

Conclusion

Lock-in has continued to put pressure on discount speeds and it could take years for this effect to dissipate. And while refinancing risk remains subdued at current rate levels, post-COVID-19 era borrowers are eagerly awaiting the opportunity to refinance.

The combination of slow discount speeds and a potentially massive surge in refinancings if primary rates fall sharply imply a more negatively convex investment universe than in the past. But we believe the mortgage market offers many investment alternatives that are designed to mitigate these risks and help investors to achieve the desired risk profile.

[1] 18 May 2026

[2] Prepayment speed is the rate at which unscheduled principal is paid to investors, in any given period. Each month, MBS investors receive scheduled principal, unscheduled principal, and interest. Prepayments in mortgage pools occur because of refinancings, turnover, curtailments, and buyouts.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.