Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

How AI and conflict are reshaping markets

While war in the Middle East will continue to grip investor attention, we think the tech revolution will prove a more powerful and longer-lasting force.

The following is an extract from our 2026 midyear global outlook.

In the near term, markets are driven as much by sentiment as by fundamentals. AI narratives around capital spending, innovation and competitiveness are shaping investor positioning and amplifying price moves. Geopolitical tensions add to the volatility through higher energy costs and risk, reinforcing the sense that markets are contending with several overlapping forces. While the ongoing conflict will likely continue to sway markets in the short term, we believe AI will prove the more powerful and longer-lasting force – changing earnings and the credit landscape over the years ahead.

Fixed income

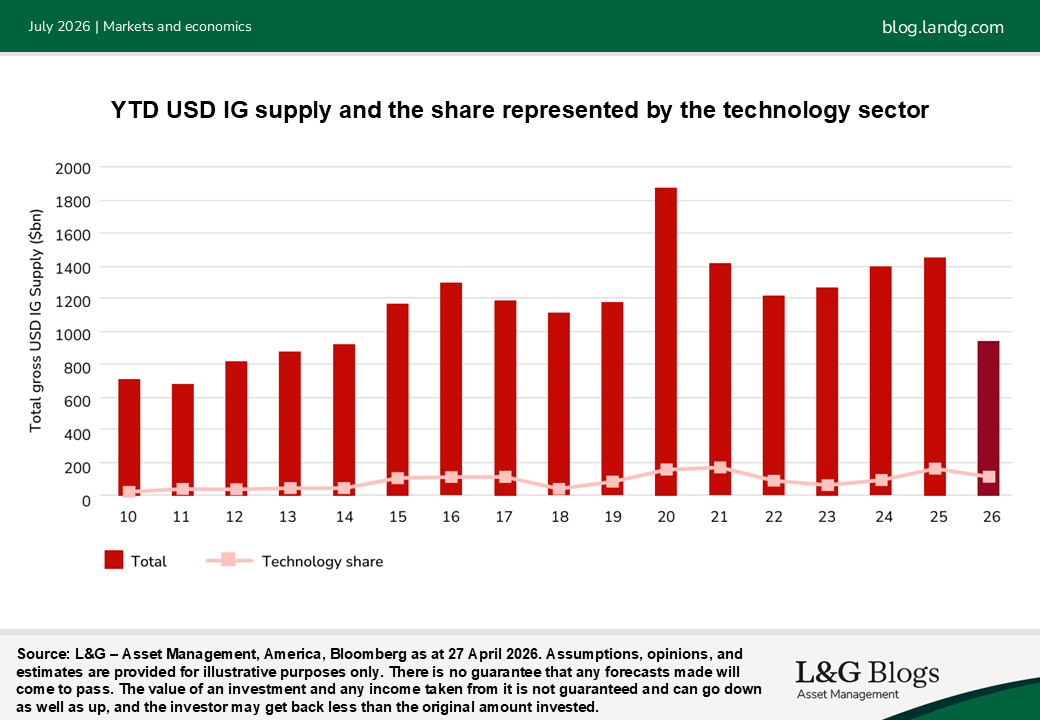

Hyperscalers are committing unprecedented sums to data centres, power infrastructure and chips, increasingly funding this investment through public bond markets. Even those with the strongest balance sheets are now issuing at scale, fundamentally transforming investment grade credit markets and increasing their index representation.

For example, Alphabet’s* rare 100-year sterling bond issue means the issuer will now account for 1-3% of key UK investment-grade benchmarks.[1] This growing concentration could introduce greater concentration risk within global credit markets. At the same time, AI is driving changes to how and where that issuance is being bought. For investors, the opportunity is no longer simply to participate in attractive new supply, but to identify curve- and tranche-level dislocations that arise because different investor bases demand different bonds, with differing maturity levels, currencies or features.

But the AI story is evolving from just being about capex to one of competitive pressures within industries as companies react differently to the technology: some will adapt quickly to cut costs and improve their offering, while others will find their margins – especially those dependent on routine cognitive work – more exposed than they thought.

For credit investors, this matters because fixed income captures less upside from winners than downside from losers.

Greater divergence between issuers has historically coincided with wider spreads. As AI increases disruption across sectors, we expect dispersion to rise above average, providing more opportunities for active managers to demonstrate their alpha generating skills.[2]

Concerns over the impact of AI on software companies have become widespread, and there are different concentrations of software in different markets: from over 20% in high yield private credit to 5% in public market high yield, which may suffer some contamination from concerns over private credit software concentrations.

Equities

While the conflict in the Middle East remains a risk, US equities have continued to rally since March. AI could explain their resilience despite this ongoing geopolitical uncertainty. Enthusiasm for the technological revolution has supported US equities reaching all-time highs, led by strong momentum from the semiconductor and tech sectors.

For equity investors, AI-related dispersion can create opportunities for stock selection as winners outperform companies that struggle to adapt.

Despite high equity valuations, we are mindful of emerging risks from the interplay between AI and geopolitics. For example, elevated capex, rising energy usage and supply constraints due to AI may contribute to inflation, as noted by Tim. Meanwhile geopolitical pressures could disrupt supply chains and hyperscaler capex plans, potentially weighing on growth and AI-sensitive equities. We believe this dynamic could support bottom-up alpha generation.

Digital infrastructure

AI demand is not the core driver of digital infrastructure sector supply-demand imbalances, but it does act as a swing factor to increase competition for capacity – especially in prime locations where power is already constrained. This adds pressure to a system where supply is structurally slow; for example, assets such as data centres typically take around six to 10 years to bring to fruition from scratch.

Long-term leasing dynamics reinforce this tightness. Contracts often extend beyond five years, with both hyperscalers and newer AI-focused entrants committing to up to a decade.

However, the durability of some AI business models remains uncertain, particularly as they approach critical hardware refresh cycles after roughly three years. If financing proves insufficient, some lease failures could emerge – though low vacancy rates suggest capacity would likely be reabsorbed.

Global conflict is pushing up energy and construction costs, slowing development further. Given the critical nature of compute, demand is relatively price inelastic and increased costs are typically passed onto customers or tenants.

If development projects slow down due to cost pressures, this will further exacerbate the supply/demand imbalances. This will strengthen pricing powers for data centres offering compute capacity and allow them to earn higher profits and margins.

*For illustrative purposes only. Reference to a particular security does not mean that the security has been, is currently held or will be held within an L&G – Asset Management portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] Bloomberg, as at 31 March 2026.

[2] Morgan Stanley Research, as at Feb 2026; Bloomberg Intelligence/BoA (January 2026).

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.