Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Emerging market debt – a fair wind

We believe emerging market (EM) credit returns this year will be led by both carry and a rally in high yield credit spreads. Assuming interest rates in the US remain range-bound, our belief is that EM credit could post positive total returns of high-single digits for 2024.

The following is an extract from our Q2 Active Fixed Income outlook.

The past: what just happened?

EM debt has had a mixed start to the year, with the selloff in US rates being offset by positive returns due to spread tightening. The latter has largely been driven by stronger-than-anticipated US growth, a positive factor for the EM universe.

While EM investment grade has produced negative returns year-to-date, EM high yield credit (hard currency sovereigns and corporates) has registered returns in excess of 4%.[1] Despite continued outflows from EM bond funds, the asset class has seen record primary market issuance year-to-date, which has been well absorbed.

The present: key themes

Favourable macroeconomic environment

According to the IMF, EM economies are estimated to grow by c.4% this year, more than their developed market (DM) counterparts, resulting in the widest EM-DM growth differential for eight years[2].

In addition, we’ve already seen interest rate cuts by many EM central banks throughout 2023 and 2024, which, we believe, will provide an additional impetus to domestic demand.

Renewed market access for some issuers

Idiosyncratic stories in distressed credits such as Pakistan, Egypt, Nigeria, Ghana, Sri Lanka and Argentina are also registering positive returns year-to-date[3]. As borrowing costs in these countries continue to fall, we believe several high yielding credits should regain market access, further reducing refinancing risks. We’ve already seen the likes of Ivory Coast, Kenya, Montenegro and Benin come to the market this year.

Renewed market access, strong IMF support and good macro fundamentals are being reflected in rating developments, with the number of upgrades and positive outlooks outweighing downgrades and negative outlooks so far in 2024, as actioned by various credit rating agencies.

What could go wrong?

The biggest risk for the asset class, in our view, remains US data, which could impact US rates and equity markets. If inflation prints come out higher than expected, the ‘higher for longer’ rates narrative might still come true, proving a headwind for the asset class. As a result, we remain cautious in our duration positioning, maintaining sufficient flexibility to act in different scenarios.

Geopolitical issues are another concern, even though markets have somewhat looked beyond these. This year will also see many countries hold elections, including India, Mexico, South Africa, Korea and Panama.

Furthermore, the outcome of the US election could have consequences for emerging markets – via its impact on geopolitics and macroeconomic fundamentals.

Outlook

Building on a strong performance in 2023, we believe the outlook for EM debt looks favourable, with EM growth holding up, inflation heading down, supportive monetary policies, strong support from multilateral agencies and capital markets reopening for several high yield credits. As more confidence builds around the rate-cutting cycle in the US, the focus will shift towards duration.

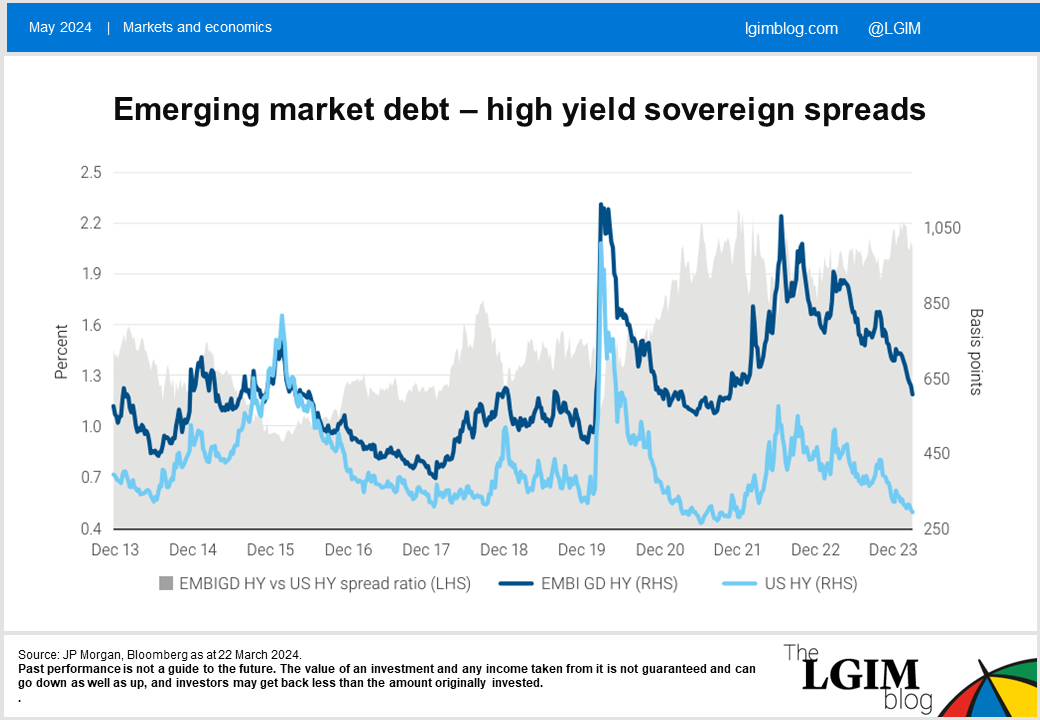

Despite the recent rally in spreads, we believe EM high yield valuations still appear cheap relative to historic levels. Yields remain elevated, particularly within the EM high yield sovereign area, so contributing to the carry trade.

By contrast, within the EM investment grade universe, spreads are not cheap on a relative basis and, we believe, spread tightening opportunities are limited. However, all-in yields still provide pickup over developed fixed-income markets, which could grow if we see the Fed delivering two to three interest rate cuts this year. This expectation has likely driven strong participation from crossover investors into EM bond strategies.

The above is an extract from our Q2 Active Fixed Income outlook.

[1] Source: JP Morgan, Bloomberg as at 21 March 2024.

[2] Source: IMF, World Economic Outlook as at March 2024.

[3] Source: Bloomberg as at March 2024.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.