Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

AI goes global

AI’s global expansion is reshaping markets, politics and the balance of economic power

This is an article from our Q3 Active Fixed Income Outlook.

Some technologies have the power to change something forever. A rare few can change everything forever.

But if anything in our history has the ability to concentrate economic and political power in the hands of the few, it’s unambiguously AI.

We have witnessed extraordinary technological innovations before. They have deeply influenced the economic, political and social landscapes of their day. AI is no different – it’s just playing out much faster than even the most bullish early forecasts suggested.

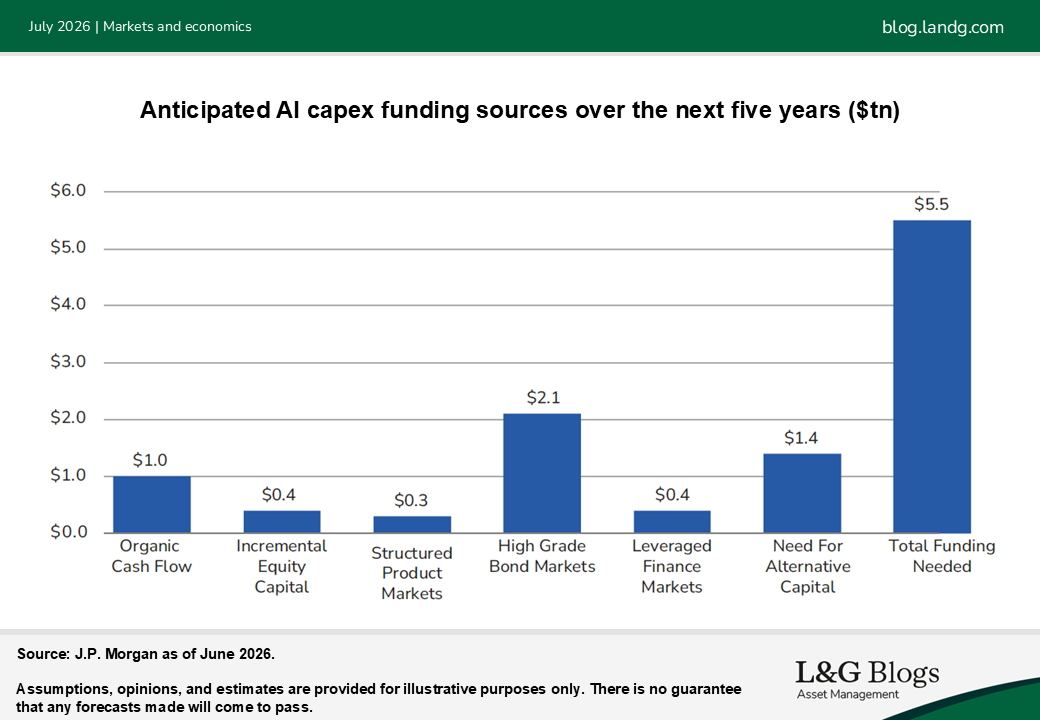

We have highlighted before that the investment required to build out AI infrastructure would be large enough to have macro significance. Today, we would argue that AI marks a fundamental decoupling of capital expenditure from traditional

productivity expectations.

This is now a regime shift from cost optimisation towards massive, almost non-negotiable capex outlays with the capital raising and borrowing to fund all of this required today, likely to extend over the next three years and beyond.

One of the reasons why credit spreads have been so tight so far could be that up until now, investment grade indices have been relatively insulated from the disruption the AI theme has caused. They are largely made up of the older, more capital-intensive industries. It’s hard to see how AI could disrupt regulated utility, infrastructure or asset-heavy parts of the economy anytime soon. Whereas the main equity indices are dominated by tech and related companies which are more

exposed to the early stages impact of this new technology.

That is now changing. Since late last year, AI-related infrastructure debt issuance

is in excess of $300 billion[1] and issuers have been quicker to diversify their investor base globally than most initially expected. What began as a US story is rapidly going global. US technology firms are increasingly raising funding in

international markets and spreading the AI capex boom across global credit markets. Data centres and the supporting infrastructure builds are accelerating across regions including Europe, the Middle East and Asia. In our outlook you can read our insights on how the globalisation of AI is impacting Euro credit, emerging market debt and global high yield.

As companies experiment with Claude Code and what it can do for them, there is a dawning realisation of how AI could potentially change how a labour market functions. People can see that it could disrupt livelihoods, jobs and the way society

currently conducts itself.

AI’s impact will be felt right across the labour market, but if it initially comes at the expense of those looking to enter the working-age population, then generational conflict is a possibility within society. We are seeing the early stages of the anxiety, tension and friction that AI delivers in the US, with a growing negativity around this new technology, especially at the state and local level.

Does this threaten the whole AI capex boom? We don’t think this will happen just yet, as the numbers are just too big.

However, the US political system will begin the long process to elect its next President after the mid-terms in November. If the pushback against AI becomes big enough to attract the attention of the politicians, what are the chances of an anti-AI

ticket emerging? The potential for a populist anti-AI narrative with a political figurehead could have significant implications for current equity valuations and portfolio concentrations. Either way, AI will be a key theme in the election of the next

US President. All candidates that run in 2028 will need to have a very clear message on their AI policy.

If governments seek to regulate the pace of adoption because of this perceived threat to jobs, then markets will start to question valuations and the return on investment for all this capex. Any meaningful shift in US policy on AI will undoubtedly have a ripple effect across global markets and politics.

The societal pushback is understandable, and the concerns behind it are legitimate. But returning to my initial point, AI leadership is increasingly becoming a proxy for economic and geopolitical influence. That could make the risk of the West pulling back unilaterally, while others continue to accelerate, one worth taking seriously.

This is an article from our Q3 Active Fixed Income Outlook.

[1] J. P. Morgan, as of June 2026

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.