Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Why credit investors should consider a hedging toolkit

Amid challenging market conditions, we believe it's important to use a robust and diverse[1] hedging toolkit.

“The only perfect hedge is a Japanese garden.” Eugene H. Rotberg made this observation in 1990, speaking to the National Association of Corporate Treasurers, as markets placed growing faith in derivatives and financial engineering. His message was simple: no single hedge can deliver protection in all conditions. Durable outcomes come from combining different elements, each with a distinct role.

Within our unconstrained bond strategies, we focus on three key hedges: duration, credit default swaps (CDS) and liquidity.

Geopolitical tensions and their associated risks are top of mind for investors around the world. During these periods, financial markets rarely react in a neat or uniform way. As a result, relying on any single hedging tool can prove insufficient when events unfold in unexpected ways.

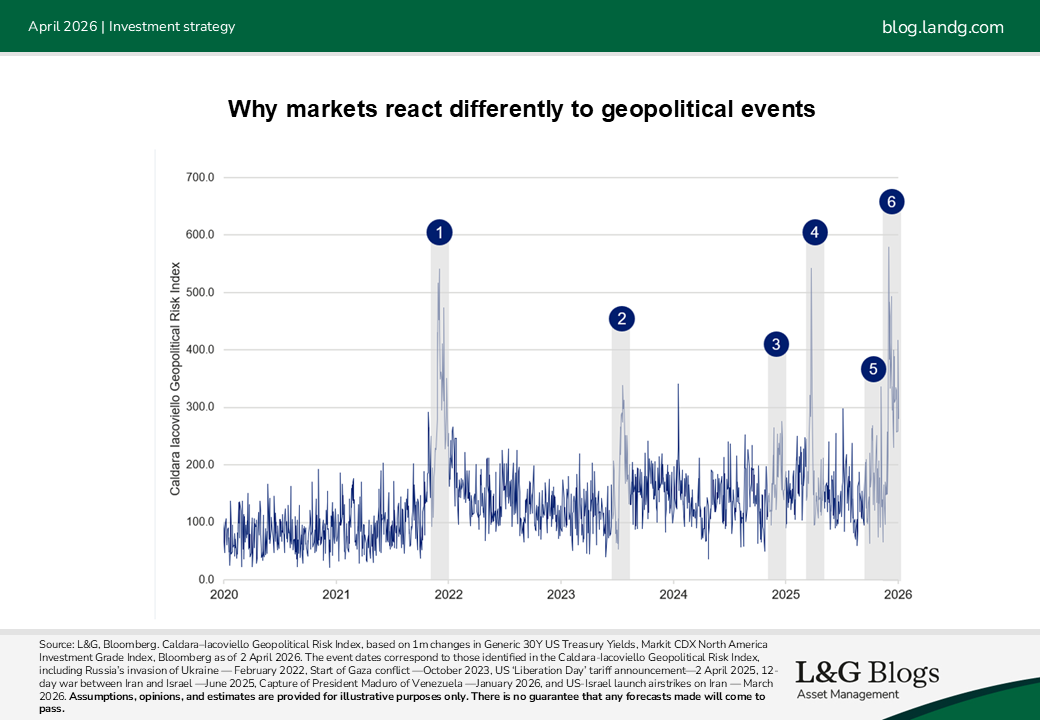

The Geopolitical Risk Index (GPR), developed by Federal Reserve Board researchers Dario Caldara and Matteo Iacoviello, provides a systematic, quantitative measure of geopolitical risk.

In recent years, geopolitical tensions have been on the rise with the GPR index showing several notable spikes since 2023. In this environment – be it a result of conflict, sanctions or tariffs – global markets often shift abruptly into risk‑off mode. For fixed income investors in particular, each geopolitical event can trigger a distinct and unpredictable market reaction. Interest rates may rally, sell off, or remain range‑bound. Credit spreads might widen dramatically in one episode yet remain surprisingly stable in another.

This inconsistency makes relying on any single hedge very challenging. In our view, no single risk management tool works reliably across all geopolitical regimes[2]. Therefore, we believe a more flexible hedging toolkit is essential — one that adapts to the specific type of geopolitical shock rather than depending on a single hedge to perform in every scenario.

What history tells us: duration vs. CDS

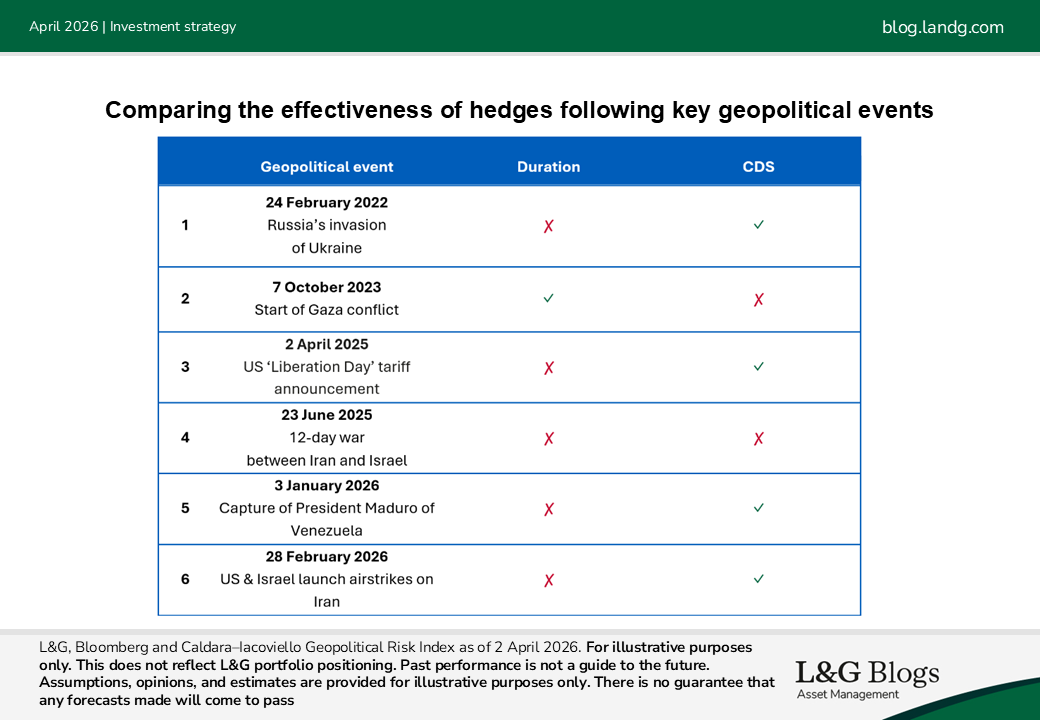

We looked at how increasing duration and CDS have worked as hedges in the one-month period following spikes in the Geopolitical Risk Index between February 2022 to April 2026. Usually, during risk-off environments, we expect to see a flight to quality, as investors shift towards capital preservation and safe-haven assets, such as long-dated government bonds in currencies such as the US dollar and Japanese yen. Intuitively, this makes sense: when markets de-risk and capital flows into government bonds, yields fall. If the impact is expected to reduce growth, interest rate cuts become more likely and long-end yields tend to fall on risk-aversion and expectations for rate cuts. However, if the impact is expected to increase inflation, then rate rises can be expected, and this means that duration can materially hurt fixed income portfolios.

Therefore, duration has not consistently been an effective hedge. When investor sentiment deteriorates and if inflation is expected to increase, credit spreads tend to widen, therefore we believe a position in CDS (buying protection) can potentially be a better tool, especially in credit-centric portfolios.

An often-overlooked hedge: liquidity

Raising liquidity can help to provide investors with enhanced control during periods of heightened uncertainty. It serves as a buffer for portfolios, especially during periods when neither duration nor CDS offer significant risk mitigation. Liquidity enables investors to withdraw from volatile markets and return when valuations appear more attractive, while also allowing them to capitalise on potential opportunities created by constrained investors being forced to sell. Frequently, liquidity can potentially be the most valuable hedge during disorderly, correlation-breaking events.

An unconstrained approach which leverages all three hedges

Rather than depending on one dominant lever, we employ a robust toolkit that can use multiple defensive tools at the same time. This gives us a more diversified[1] and adaptable risk management framework[2] that can respond flexibly as market dynamics evolve, rather than forcing all scenarios into a single hedging method.

In periods of elevated volatility, we believe investors should not simply ask whether to hedge, but rather what type of hedge is most appropriate for the underlying risk. Different shocks drive different market responses; therefore, hedging decisions must be made with a clear understanding of the underlying risk.

We view duration exposure primarily as a hedge against the credit risk we take. We therefore actively consider when it could act as a risk-reducing hedge, and when it could act as a volatility-increasing source of losses. When credit spreads widen amid uncertainty, duration often acts as a counterbalancing force. But when inflation fears are also dominant (as in 2021 and 2022), duration could act as an additional source of losses. This gives us an additional defensive anchor or another string to our bow. For example, in 2022 following the invasion of Ukraine, our unconstrained strategies had low duration, as well as high levels of liquidity.

Conclusion

Geopolitical uncertainty is unlikely to disappear soon. To navigate these challenging conditions with minimal disruption, we believe it is essential for portfolios to use a multi-dimensional hedging toolkit. When market volatility occurs, adapting how much duration, CDS and liquidity we hold in portfolios can help create a stronger foundation for achieving more stable long-term results.

History demonstrates that using a combination of these three hedges is far more effective than relying on just one.

[1] It should be noted that diversification is no guarantee against a loss in a declining market.

[2] Risk management cannot fully eliminate the risk of investment loss.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.