Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

The sponsor’s dilemma: when the ‘legacy problem’ becomes a strategic asset

In our first in our series of six blogs on pension scheme run‑on, we start with the perspective of a corporate sponsor – looking at how improving funding levels are prompting a reassessment of traditional endgame thinking.

For much of the past two decades, defined benefit pension schemes were viewed primarily as a risk to be eliminated. A pension scheme introduced balance sheet volatility, constrained cash flow, and diverted management attention. The default solution was clear. Pay the insurance premium and remove the liability entirely.

Framing is now changing. Funding positions have strengthened, surpluses are emerging, and with new legislation, the rush to buyout is being questioned. The strategic question has shifted from how to exit as quickly as possible to, whether the certainty of buyout justifies the cost – can more value can be retained by running a scheme on?

The accounting reality

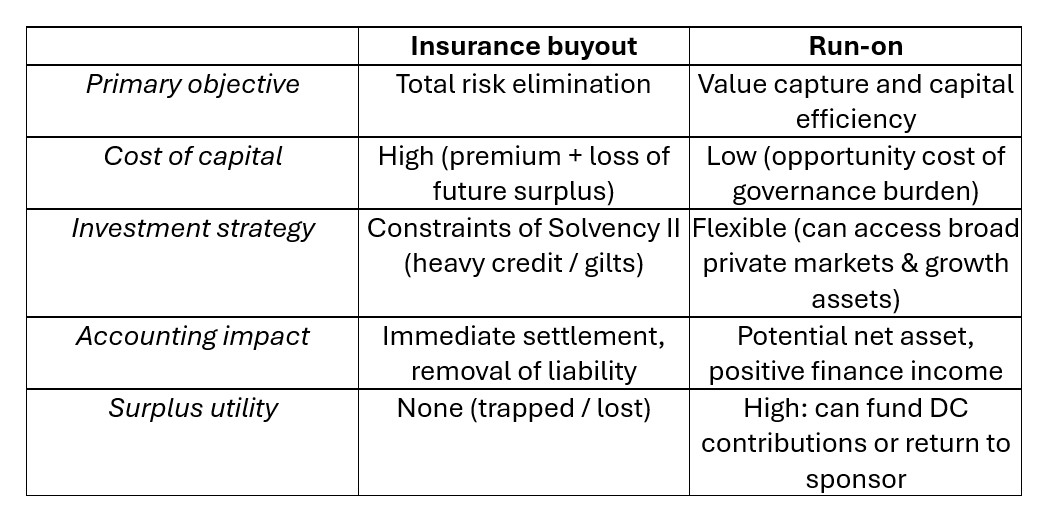

A key challenge with buyout is its accounting impact – as it often crystallises a one‑off P&L loss.

Insurers price liabilities using highly prudent discount rates, typically gilt-linked and including margins for capital and profit. IAS 19 liabilities, by contrast, are discounted using high‑quality corporate bond yields. As a result, even a scheme that appears fully funded on an IAS 19 basis may still require a cash injection or a reduction in shareholder equity to meet the insurer’s price.

For CFOs, buyout therefore represents a visible use of capital rather than a neutral clean‑up exercise.

Changing the financial impact by running on

A run‑on strategy reframes the pension scheme from a cost centre into a potential economic asset. By retaining assets on the sponsor’s balance sheet, where scheme rules allow the sponsor to access future surplus, value can be generated rather than paid away.

From an accounting perspective, surpluses retained within the scheme can, in some circumstances, contribute positively to reported financial outcomes. Where the sponsor has an unconditional right to surplus, typically at wind‑up, that excess can also be recognised as an asset rather than being trapped within the scheme.

Investment flexibility

Run‑on also offers greater investment flexibility. Insurers operate under Solvency II constraints and rely heavily on gilts and high‑quality credit.

Sponsors running schemes are not bound by these restrictions. This flexibility allows access to a broader opportunity set, including private markets and other areas that offer illiquidity or complexity premia. Core infrastructure, and long‑lease property for example, can play a role in improving returns without materially increasing risk.

Running on allows sponsors to retain these returns, rather than transferring them to insurers through capital charges and pricing margins.

Governance considerations

The most common objection to run‑on is governance capacity. Sponsors are not asset managers, and historically trustee structures were not designed to support complex, long‑term strategies.

Delegated investment models can now provide a practical solution. Sponsors and trustees retain control over objectives such as funding targets, risk tolerance, and ESG constraints, while implementation and day‑to‑day management are outsourced. Outsourcing reduces the governance burden and allows schemes to be overseen professionally without becoming a management distraction.

The strategic trade‑off

Ultimately, the decision between buyout and run‑on comes down to certainty versus value.

Conclusion

For sponsors with strong covenants and well-funded schemes, buyout is no longer the default option. Where surplus is accessible, risk is manageable, and governance can be professionalised, we believe that running on offers a credible way to seek to preserve economic value.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.