Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

SpaceX IPO launches: Implications for index exposures

Index vendors have been reviewing and updating their inclusion rules to adapt to a changing IPO landscape, though differences remain, with implications for investors.

2026 is increasingly poised to become the year of the mega-cap IPO. With listings from the likes of SpaceX*, Anthropic* and OpenAI* planned this year, index vendors are figuring out how to incorporate and fast-track these companies of such extraordinary scale into their benchmark indexes.

At a target valuation of $1.8 trillion, SpaceX’s IPO represents the largest ever, possibly soon to be followed by Anthropic and OpenAI, which are each indicating valuations approaching $1 trillion. These valuations are much larger than IPOs over recent years, reflecting how increased opportunities to grow in the private-market space have enabled companies to remain private for longer than in previous cycles. As a result, when these firms finally enter public markets, they do so at a far more mature stage – often with valuations that rival or exceed long‑standing index constituents.

In response to these exceptionally large IPOs, index providers, aiming to reflect the investible market are reevaluating their rules concerning eligibility criteria, timing of inclusion and size thresholds for mega-cap new entrants. Indeed, market participants have been asked to weigh in on multiple index consultations on these matters over the first half of the year. However, even with the inclusion rule changes, differences between index provider rules remain, with implications for investors seeking to reflect these IPOs in their portfolios in a timely manner.

As of writing, we have seen methodology updates from FTSE Russell and NASDAQ, whereas S&P ultimately made no change to its S&P 1500 Composite (which includes the S&P 500 Index). In the table below, we look across the index provider landscape to ascertain how index rules are adapting to the Mega-Cap IPOs.

Figure 1: Index providers are adapting rules as a result of mega-cap IPOs

| Index provider | S&P | FTSE RUSSELL | NASDAQ 100 | MSCI [No consultation /rule changes] |

Solactive | Stoxx |

| New Large/Mega-Cap Specific Rules | No new rules for mega-cap IPOs | Yes | Yes | N/A | Treatment varies by individual index methodology | N/A |

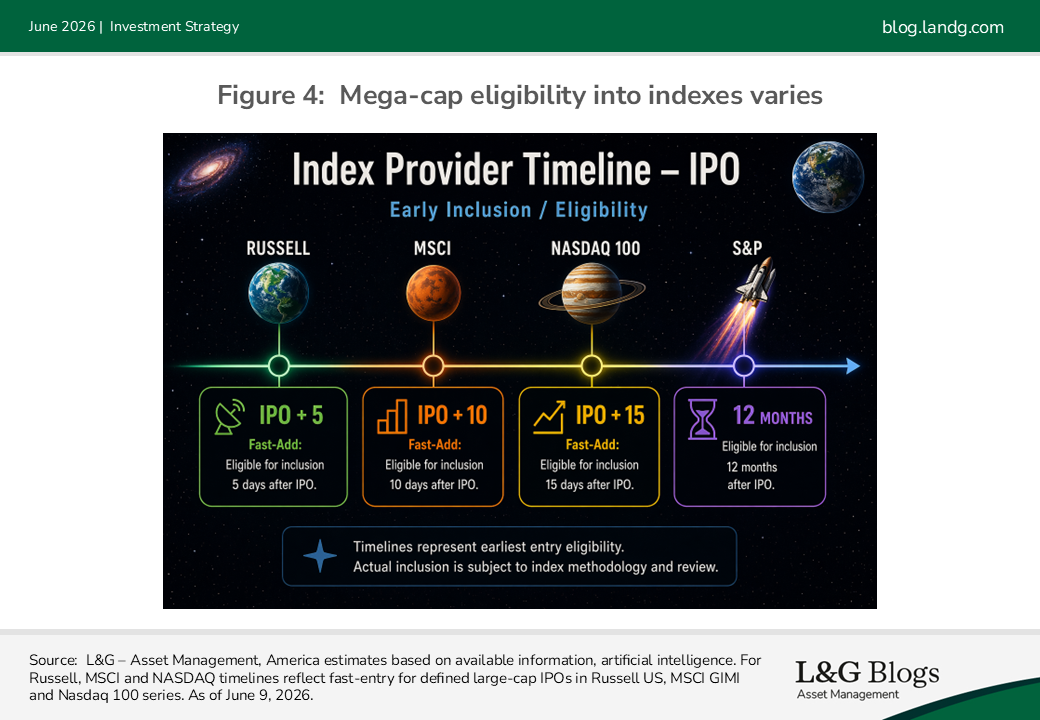

| FAST Entry/Inclusion Timeline Updates | No change [stock needs to trade for 12 months to be eligible] | Yes: IPO + 5 days entry for larger IPOs [from quarterly] | Yes: IPO + 15 days [from at least 3 months typically] |

Already in place: IPO + 10 days | Treatment varies by individual index methodology | No |

| Free-Float Rule Updates | No change [10% free-float threshold remains] | Yes: Eligible for fast entry if expectation for 5% free float within 12 months post IPO | Yes: Weight capped at 3x free float when float below 33.33% | N/A | Waiver of free-float for market capitalisation > $1bn | Standard criteria |

| Index Specific Eligibility Rules | Financial viability rule remains | Yes: Eligible for fast entry when 5% voting threshold expected to be met within 12 months | N/A | N/A | Treatment varies by individual index methodology | March and September only |

Source: L&G – Asset Management, America, S&P, FTSE Russell, Nasdaq, MSCI. . As of June 9, 2026.

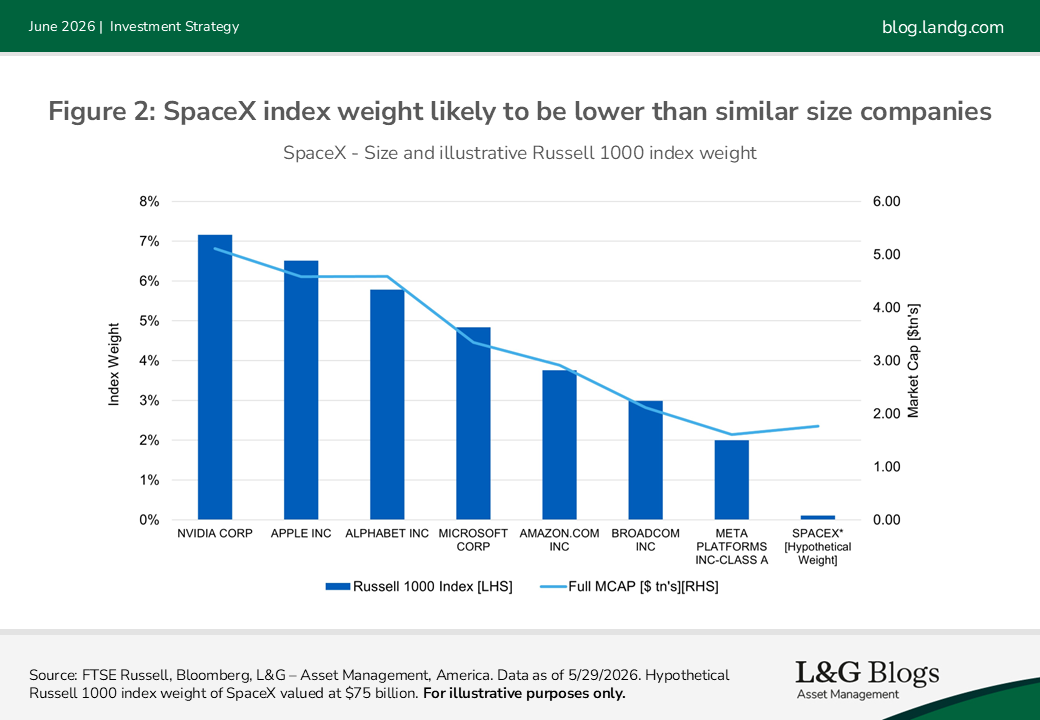

It’s worth highlighting that these mega-cap IPOs may not make up as much of the index as some may expect. While a company like SpaceX with a full market-cap valuation of nearly $1.8 trillion would place it in the top 10 of companies in the Russell 1000 by full market capitalization, companies are added to these indexes based on free-float rules. We expect that the SpaceX free float will initially be approximately 4%, representing a much smaller index weight than companies of similar sizes.

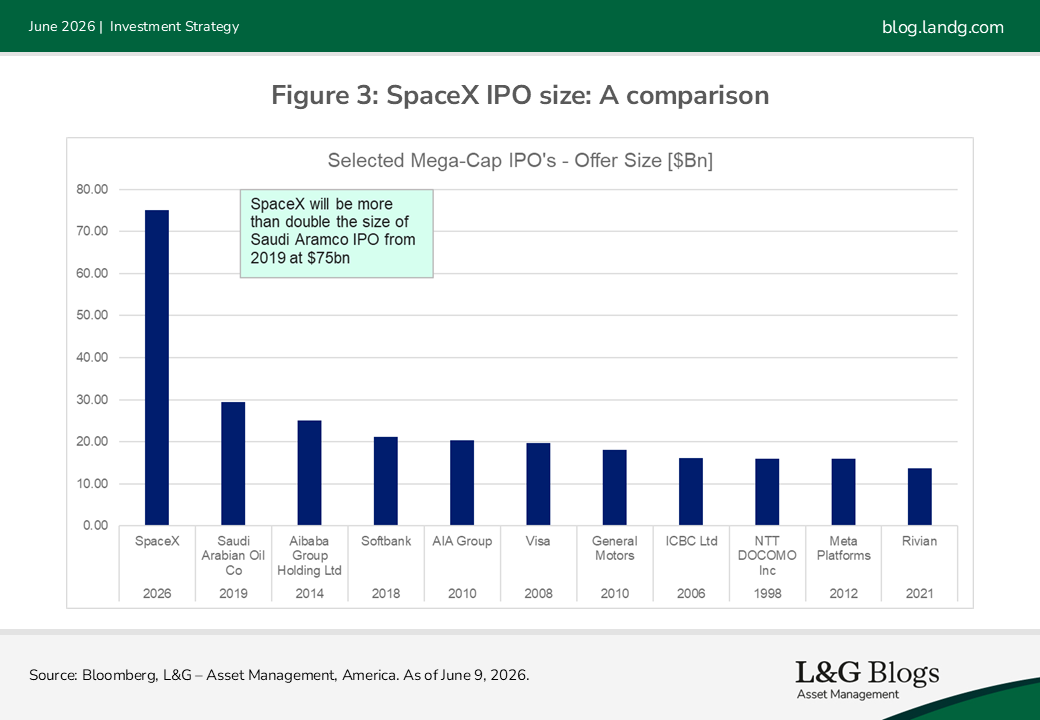

At a $75 billion IPO amount, SpaceX will be more than twice the size of the previous largest IPO – Saudi Aramco* in 2019, which raised $29 billion. These sizes reflect the underlying structural shift where companies can come to the market later in the investment cycle.

The investing implications

Although some index providers are moving to accelerate inclusion timelines for mega-cap IPOs, SpaceX would still likely need to wait at least 12 months before qualifying for S&P 500 index inclusion. Ahead of SpaceX’s inclusion in a given index, investment managers must carefully consider the trade-off between incurring tracking error and capturing potential upside by holding the stock ahead of its benchmark entry.

In terms of our core approach, which we refer to as pragmatic replication, it remains unchanged - we prioritise minimising transaction costs and managing known pricing pinch points (including IPOs and index changes), while operating within defined tracking error tolerances. We do not attempt to anticipate or trade ahead of IPOs based on short-term price dynamics; index-specific eligibility will remain the primary gating factor. Our focus is on efficient benchmark tracking, with implementation aligned to index inclusion events where possible.

Large IPO inclusions can create short-term imbalances between supply and demand, particularly where free float is limited relative to index-tracking demand. This can lead to elevated trading costs and price dislocations around inclusion events. Our pragmatic replication approach is designed to manage these dynamics by focusing on execution efficiency:

- Avoiding purely mechanical trading at a single point in time

- Accessing multiple sources of liquidity where possible

- Phasing implementation when appropriate

- Maintaining tight control of tracking error while optimising execution

This is particularly relevant in the current environment, where accelerated inclusion timelines and larger deal sizes increase the importance of careful execution. Where the approach has evolved is in how we implement around these events rather than philosophy. In practice, we will consider a range of execution strategies aimed at achieving efficient exposure while limiting transaction costs and market impact. This may involve trading around the inclusion date rather than exclusively at the closing auction.

We believe a flexible, risk‑aware approach to IPO inclusions can help reduce transaction costs, limit market impact, and achieve better outcomes for investors compared to a purely mechanical implementation strategy.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.