Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Seeking value in bulk annuity transactions

With record numbers of well-funded pension schemes seeking to insure, the question isn’t just about affordability and readiness, but how to maximise overall value safely?

The following article is an extract from our latest DB outlook.

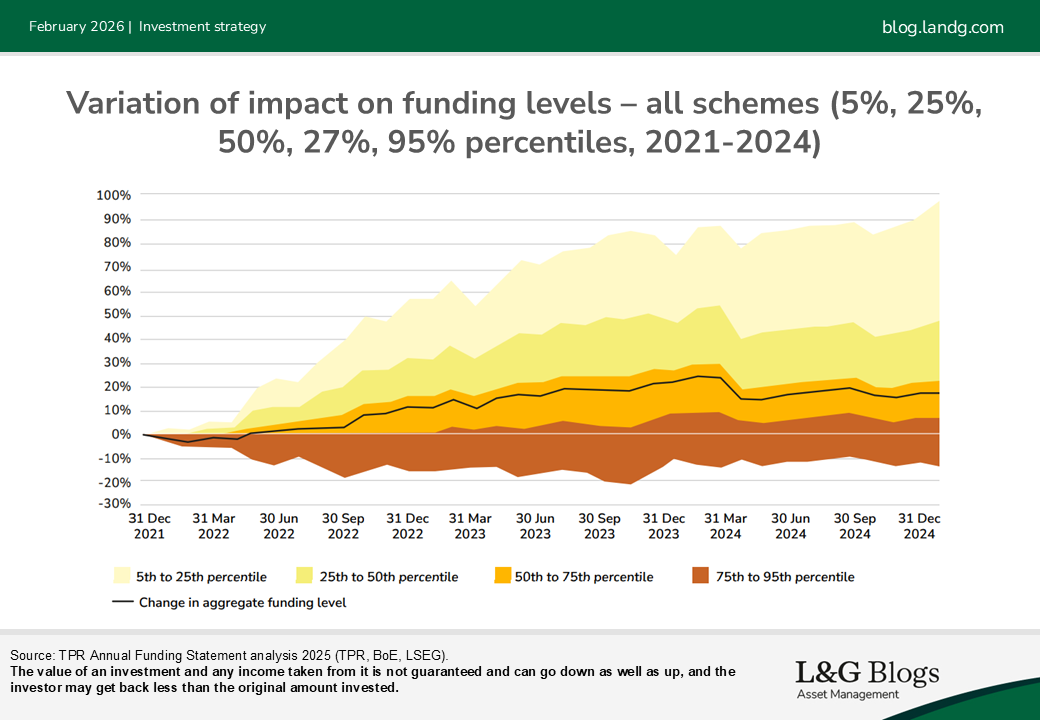

The Pension Regulator’s Annual Funding Statement 2025 estimated that 54% of UK DB schemes were in surplus on a buyout basis as at the end of 2024, equivalent to c.£600bn of buyout liabilities, with a wide dispersion of funding levels on an individual scheme basis.

Meanwhile, 2025 is expected to have been another strong year for pension risk transfer, with LCP estimating c.350 buy-in/out transactions with aggregate value of c.£40bn in 2025. Put this together and one thing is certain – it will take several years for fully funded schemes to collectively achieve their buyout objectives. Whilst they are preparing for buyout, schemes will want to seek to preserve affordability, improve pricing and manage any residual asset surplus.

Preserving affordability – hedging buyout pricing

Trying to hedge buyout pricing is easier said than done for three main reasons:

- Liability target: Liability cashflows within LDI mandates are typically calculated on a technical provisions basis, from member data as at the latest actuarial valuation and rolled forward over time. By contrast, insurers will project a liability profile using up-to-date member data and by adopting their own views on demographic and other liability risks, resulting in a liability profile with a different shape.

- Discount rate: A pension scheme may make a prudent assumption on a solvency discount rate – for example ‘gilts-flat’. By contrast, live buyout pricing, expressed on a ‘gilts+x% basis is variable over time, primarily because investment opportunities change, for example we have seen insurers move away from corporate bond based investment strategies towards more gilts heavy approaches, and because pricing is also dominated by structural pricing factors.

- Differences between insurers: While all insurers are bound by the same Solvency UK framework, each will invest and price differently to achieve the most competitive price to win business.

A pragmatic approach? We believe the best way to hedge buyout pricing is to transact, but before that, pragmatic steps include updating the liability cashflow target to better reflect solvency assumptions (and regularly recalibrating over time) and hedging to a pragmatic prudent discount rate that evolves over time to reflect current pricing levels, including credit sensitivity.

Improving pricing – is time is on your side?

For schemes that can afford to pause, pricing could be improved through:

- Maturing liabilities: As a generalisation, it costs less to insure pensioners than deferred pensioners, largely due to risk and uncertainty of both demographic factors (e.g. longevity) and member optionality (e.g. commutation), so the implied buyout price for a scheme should (all else equal) improve over time as members age.

- Asset returns and realisation: If the implied buyout price evolves at, for example, gilts+0.25%, but the scheme assets can generate more than that (net of costs), then the buyout surplus can increase. In addition, restructuring illiquid assets before a transaction may reduce costs and simplify the transaction process, albeit that the insurance market has developed several innovative illiquid asset solutions for buyout.

- Trigger monitoring: However, as set above, hedging buyout pricing is difficult – there will always be volatility between a scheme’s assets and live insurance pricing, which could be a significant benefit…or detriment to the ultimate price achieved by a scheme. Being in a position where you can not only monitor the scheme’s buyout funding level over time, but also transact quickly when the buyout funding level reaches a target level, could generate significant value.

Managing residual asset surplus – what’s your target?

Finally, for schemes that transact insurance, there will be a pause between executing a buy-in and then executing a buyout, realising surplus and winding up the scheme.

In this period, how might schemes best invest residual assets? This depends on the purpose of the surplus:

- Augment member benefits: Where the final benefits paid to members under the buyout policy can be augmented (increased) with any residual surplus assets, then these assets can be invested to hedge the buyout pricing basis that is defined in the augmentation provision. An investment strategy can be implemented to seek to hedge the augmentation pricing provisions specified by the insurance provider.

- Transfer surplus to DC: Where the surplus is to be transferred to an associated DC scheme, to be used to fund future contributions, then the associated DB assets could be invested in a similar way to the intended investment strategy to be applied in the DC strategy, preferably so that the assets are easily transferable (or capable of novation) to the DC scheme.

- Release to the employer: Finally, if assets are to be repaid to the employer, then these assets could be invested to seek to maintain or grow the expected value to the employer, for example by investing in a low volatility absolute return or short-dated credit investment approach.

As we look ahead to 2026, we expect continued innovation in ‘Route to Buyout’ approaches that allow well-funded schemes to seek to maximise value in bulk annuity transactions.

The above article is an extract from our latest DB outlook.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass. The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.