Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Illiquidity innovation

What solutions are available to schemes for their illiquid asset exposure as they approach a buy-in or buyout transaction?

This article is an extract from our Solutions outlook 2025.

The PRT market displayed notable resilience last year, with transaction volumes likely to have exceeded £40bn in 2024, according to our estimates. With PRT likely to remain one of the popular endgame options, there is increasing awareness of the potential challenges posed by holding illiquid assets when transacting a buy-in or buyout. Thankfully, the market is evolving at pace to help schemes address these challenges.

What do insurance companies look for?

Insurance companies might be motivated to hold illiquid assets if they can provide predictable cashflows with relatively low levels of risk (consistent with an investment grade credit rating) and subject to insurance regulation. Additionally, these assets need to be held directly by the scheme (or in a ‘fund-of-one’).

An example could be a directly held portfolio of investment grade corporate bonds. If the assets are held within a pooled fund, whether that’s an open-ended or a closed-ended fund, then an insurance company cannot typically use it within its annuity-matching portfolios, leading to significant cost implications.

If either of these conditions are not met, i.e. assets do not provide predictable cashflows (e.g. private equity) or they are held in pooled funds, then the transfer of these assets to an insurer in-specie is not straightforward and might lead to both timing and cost issues.

A question of time

Schemes can choose to tackle this challenge either in the years ahead of a buy-in/buyout transaction or at the point of a transaction, with advantages and disadvantages of each approach.

By allowing a number of years to wind down an illiquid asset portfolio, schemes may be able to optimise opportunities to redeem units from open-ended funds, wait for a closed-ended fund to wind down or sell assets in the secondary market, all of which may help to preserve value.

However, if a buy-in / buyout is almost within reach and illiquid assets are the main hurdle, then there are options available when working with an insurer on a transaction.

Solutions for illiquid assets

First, the insurer may be able to offer a partial deferred premium such that a scheme can take some time to find solutions for the illiquid assets subsequent to getting a deal agreed. The scheme can then work in partnership with an investment manager and the insurer to find those solutions after a buy-in is agreed.

Investment managers working under an investment mandate can offer what is effectively a ‘private market transitions service’, borrowing concepts from helping clients with public market transitions where decisions to trade are made under a rigorous framework aimed at preserving value. Choosing whether to accept or reject bids can have financially very material consequences and investment managers may be best-placed to make these investment decisions.

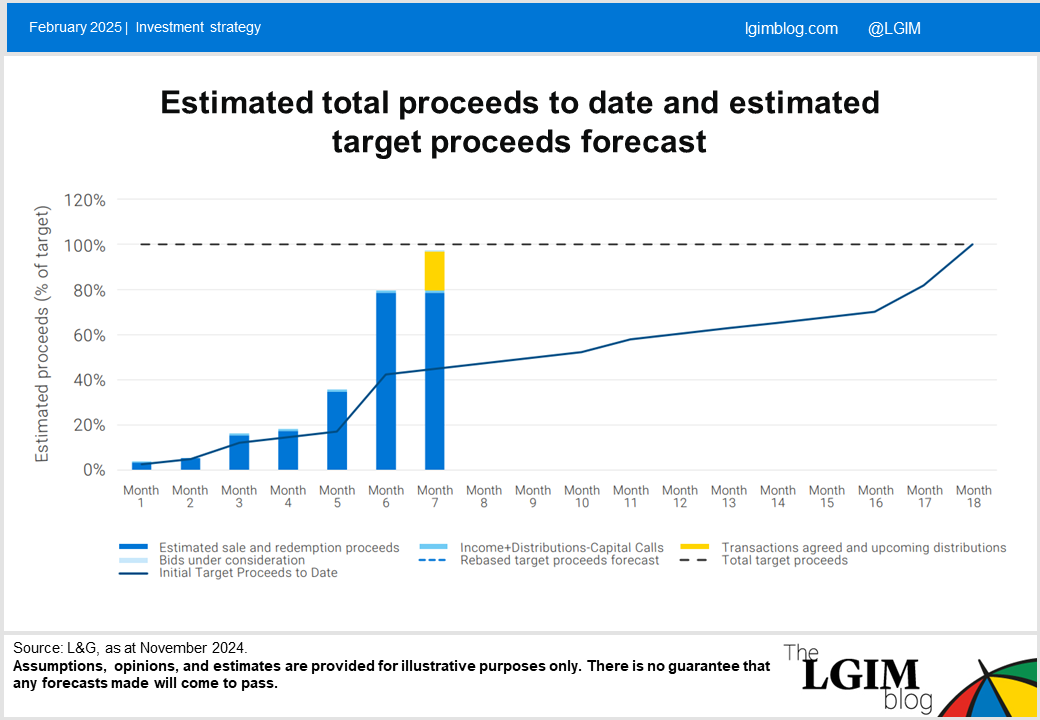

We believe this type of service could help schemes either in the years ahead of a potential transaction or in the context of an actual transaction. An example of a chart displaying progress winding down a portfolio against a benchmark agreed with a client is shown below. It has been derived from a version used in a real-life mandate where the investment objective was explicitly to sell funds holding illiquid assets over an extended, but defined, time period.

Outside of these routes, other potential options are currently being explored within the market, including securitisation of fund interests, which may allow insurers to hold pooled funds more easily. Similarly, platforms are currently setting up to help trade illiquid fund interests more transparently which could lower transaction costs over time, potentially increasing future buy-in / buyout affordability.

With this evolving backdrop in mind, we have three key messages for schemes:

1) If your immediate priority is buyout, then insurers have a range of solutions to ensure that illiquid assets need not be a barrier to transacting.

2) If you have more time, then a plan of action built in partnership with an investment manager can help you to restructure asset holdings to improve your scheme’s readiness for buyout down the line.

3) The real ‘illiquidity innovation’ here can be realised by combining approaches 1) and 2). In other words, you can ask your asset manager to help get your pension scheme ready while simultaneously giving your insurer a target to exchange the scheme’s portfolio of assets to enable the transaction to take place.

As schemes look ahead in 2025, we believe those holding illiquid asset exposure and also considering buyout may do well to heed the example shown in the chart above. As the saying goes, what gets measured gets managed. So consider analysing your illiquid asset options, setting a target on that basis and then measuring success against that target.

Read our full Solutions outlook 2025.

If you’ve enjoyed this content, we’d like to highlight that you can find all our latest content for DB schemes in one place at our designated DB blog page.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.