Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Investing like an insurer? This seems familiar!

Changes in insurer allocations over 2024 may mean that asset strategies are now closer to a typical ‘low-risk’ pension scheme strategy. This has been driven by both market and regulatory changes.

Many pension schemes are now a position where they can afford a buyout with an insurer (over a third of schemes by value are in surplus on a buyout basis, as at 31 March 2024[1]). However, executing a transaction may take some time – as the scheme prepares to get buyout-ready. This includes, for example, data cleansing and preparing benefit specifications, putting a plan in place for any illiquid assets and preparing to engage with the insurance market (for more information see our article How to secure DB pensions in a crowded market).

So, as they prepare for a buyout transaction, how best can a scheme seek to lock in this very strong funding position? In other words, how best to maintain (or grow) the funding level versus insurer buyout pricing?

The high-level answer to this question remains the same: to invest ‘like an insurer’. The aim is to minimise price volatility in the buyout funding level and have a portfolio that an insurer can ‘price-lock’ to at the point of transaction and then accept in-specie at the point of settlement. This is because insurer pricing will reflect the value of the portfolio of assets that they intend to use to match the scheme liability cashflows.

Out with the credit, in with the gilts

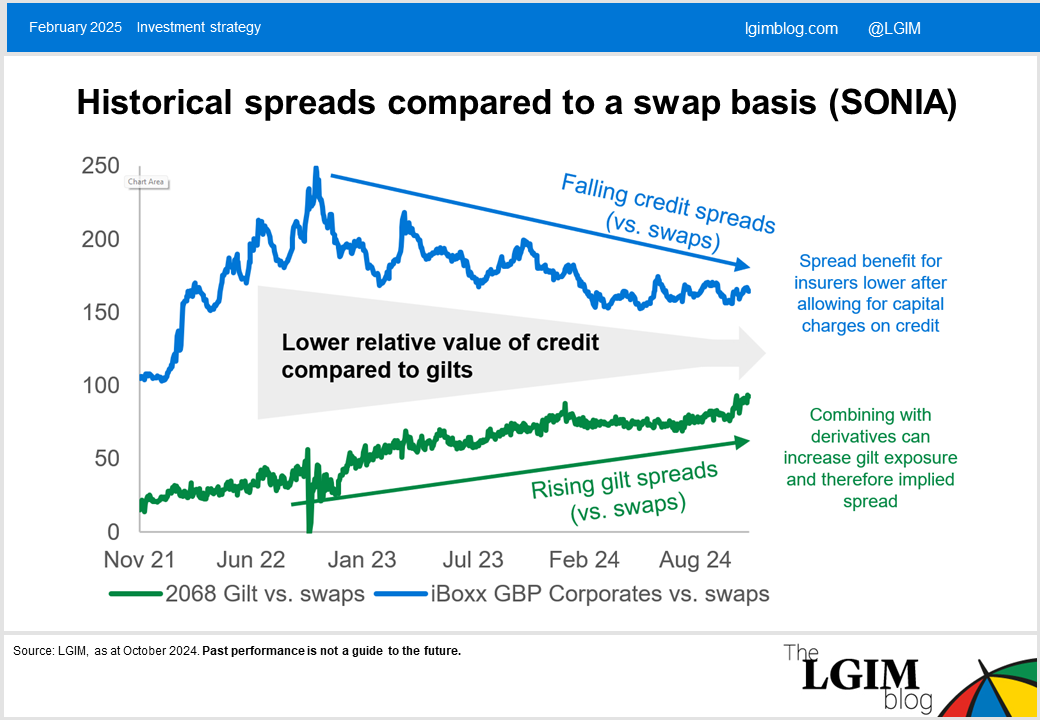

However, the way insurers have been investing has changed materially over the past year. Traditionally, insurers largely invested physical assets in corporate bonds and illiquid direct investments (often credit-type assets such as infrastructure debt). The allocation to government bonds was typically kept at a relatively prudent level, given that gilt yields were much lower than corporate bonds.

However, over 2024, insurers increasingly favoured government bonds (relative to corporate bonds). This has been due to:

- Falling corporate bond spreads relative to government bonds

- Rising government bond spreads relative to swaps (this is important given that insurers assess spreads on investments relative to swap curves given insurance regulation)

Through an insurer’s lens, government bonds can now potentially look more attractive than corporate bonds after also taking into account:

- Insurance regulation which requires more additional capital to be held versus corporate bonds (given perceived credit and downgrade risks[2])

- The ability to pair government bonds with derivatives to further increase the exposure of the government bond spread relative to swaps

Investing ‘like an insurer’? Haven’t I heard about this before?

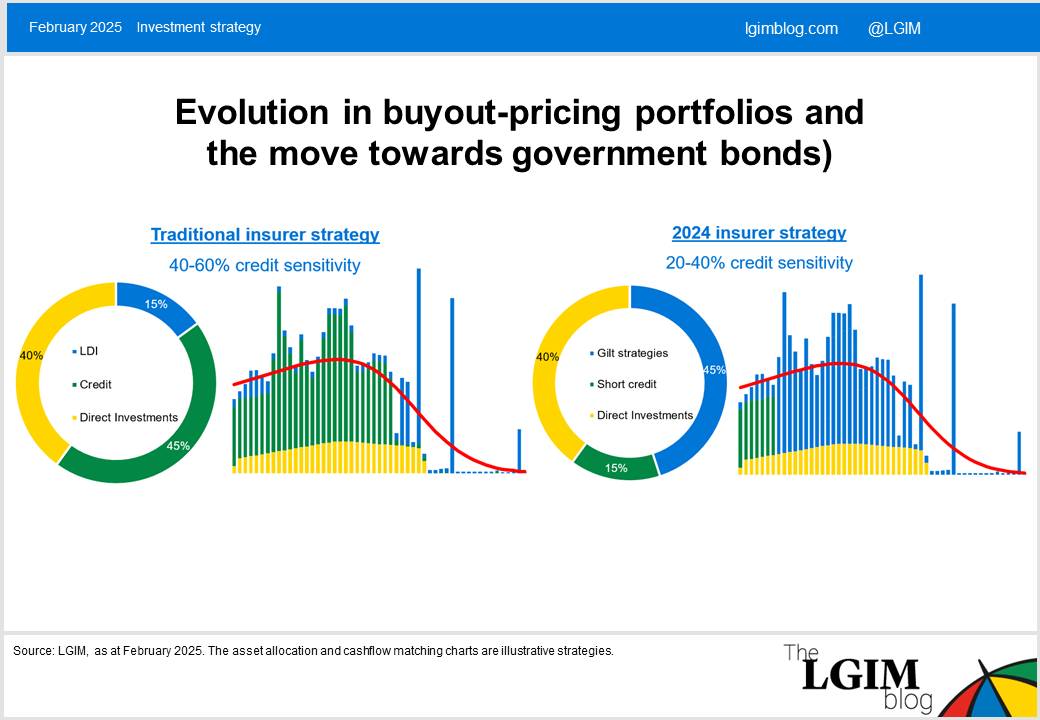

This backdrop means that insurers have been tilting their allocations (when pricing new transactions) to:

- Increase the allocation / exposure to UK government bonds

- Materially reduce the allocation to credit

- Reduce credit duration

The last point reflects the fact that government bonds could now potentially look even more attractive for insurers versus credit on a medium / longer-term time horizon.

The chart on the right might seem familiar to many pension schemes, as it might not look too dissimilar to a typical liability hedging profile (bar the illiquid direct investments). This is because pensions schemes (compared to insurers) have traditionally had:

- A higher allocation and exposure (reflecting liability hedging derivatives) to UK government bonds

- A lower allocation to credit, with greater use of shorter-duration credit

The upshot is that many schemes could find that their current investment strategy is now closer to how insurers invest. As insurers are now investing more similarly to how pension schemes (targeting a lower-risk investment strategy) have typically invested. However, we note that many pension schemes remain underweight credit compared to even the lower credit allocation insurer portfolio.

How (highly) predictable?

As well as these market drivers, we believe that regulatory changes also have the potential to further align pension scheme and UK buyout insurer portfolios. Traditionally, insurers have been somewhat constrained in which parts of the credit universe they can use (when matching liability cashflows) due to the ‘matching adjustment’ requirement that investments have fixed cashflows. This is a stringent constraint which has ruled out most of the securitised universe and any bonds which can be called or prepaid early (subject to certain criteria[3]).

A revision in UK insurer regulation last year has broadened the eligibility criteria (when matching liabilities) to now allow assets with ‘highly predictable’ cashflows (subject to a limit[4]). i.e. there is now a wider net of credit-like assets which can be used by insurers.

We will have to wait to see how this new regulation will impact insurer pricing portfolios. However, we expect that insurers may start allocating more to asset classes, including securitised credit, which have become increasingly common place in ‘low-risk’ pension scheme portfolios.

If you’ve enjoyed this content, we’d like to highlight that you can find all our latest content for DB schemes in one place at our designated DB blog page.

[1] The Purple Book 2024

[2] This is the credit spread risk component which contributes to the insurers overall Solvency Capital Requirements (SCR)

[3] Some bonds which can be prepaid early are still eligible, e.g. if earliest call is close to the bond maturity date or if there is sufficient compensation to replace the bond with an equivalent, known as a spens clause

[4]This limit is 10% of the total matching adjustment benefit

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.