Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

LPI inflation: back in focus for DB schemes

In periods like today, forming a view on inflation remains challenging. But should schemes be asking a different question?

For many DB schemes, the key question to ask is not what the outlook for inflation is, but whether their current asset portfolio hedges the true economic liabilities with appropriate accuracy. And if the answer is no, what could be the risk or cost to the scheme? Spoiler alert… it could be significant!

As schemes seek to become better funded, with de-risked portfolio and higher hedge ratios, small sources of mismatch matter more. At the same time, the inflation backdrop is more shock-driven, so the path of inflation matters, not just the average.

LPI explained in 60 secondsLPI stands for Limited Price Indexation. It describes how many DB benefits increase: in line with inflation, but with limits. Example: LPI (0,5) where inflation is capped at 5% and floored at 0%.

|

From funding pressure to funding precision

Improved funding levels have changed the conversation. So the question shifts from “are we hedged?” to “are we hedged accurately?”

Two schemes with the same headline hedge ratio can see different outcomes depending on what the assets are hedging, and how LPI increases are treated in the cashflow benchmark.

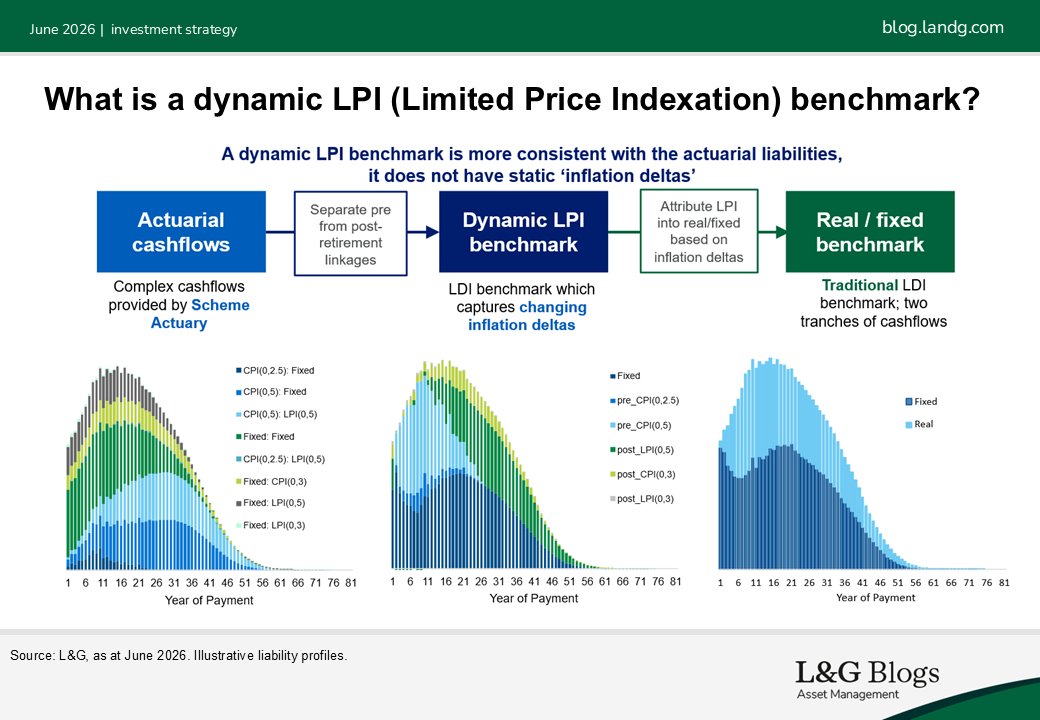

From a static benchmark to an evolving one

Many LDI mandates still rely on static liability cashflows comprised simply of fixed cashflows and RPI cashflows, updated periodically. A static benchmark is a good proxy of the liabilities at date of construction, however it has linear inflation linkage and can drift over time as it does not capture the nuances of LPI increases on an ongoing basis. That can create step changes in the benchmark when updated even though markets and the economic value of liabilities move every day.

However an ideal LDI benchmark should:

- Closely represent actuarial liabilities amid changing market conditions

- Align with the endgame objective, whether run-on or buyout

- Roll forward consistently with limited step changes

For inflation, that means reflecting benefit design, including LPI caps and floors, rather than relying on a linear proxy. This is known as a dynamic LPI benchmark, comprised of fixed cashflows, RPI cashflows and LPI-linked cashflows for the most significant increases.

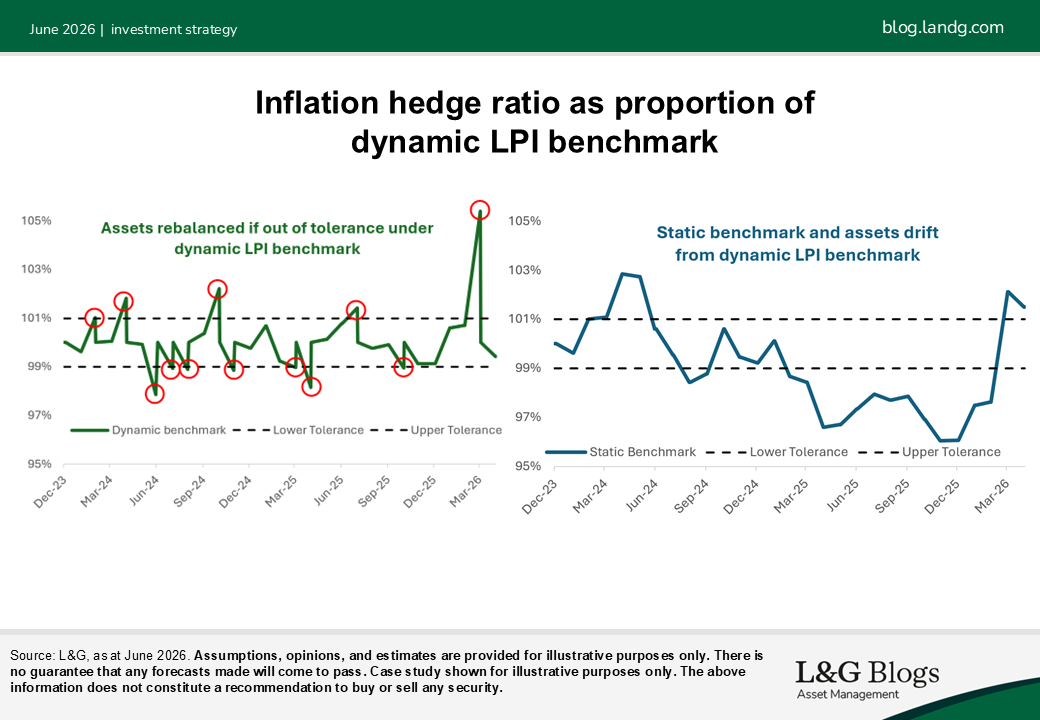

The impact of hedging against a linear or dynamic benchmark can be significant:

Case study 31 Dec 2023 - 30 April 2026Scheme with £3.5bn liabilities consisting of post-retirement LPI(0,5) increases which account for 52% of the present value, 57% of the interest rate and 73% of the inflation exposure of total liabilities

|

Today’s inflation backdrop makes this more relevant

The current environment increases the value of getting the shape right:

- UK policy uncertainty can shift the distribution of inflation outcomes. Today’s rapidly evolving political landscape appears especially uncertain.

- Geopolitics, supply chains and commodities can drive sharp inflation bursts

- AI may be disinflationary over time, but the transition can be uneven

Spikier inflation paths increase the likelihood that LPI caps or floors are impactful, which is where static benchmarks, and therefore hedges, can drift from liability reality.

A trustee and consultant checklist

If you want a practical way to bring this into governance, these questions are a good start:

- What proportion of our liabilities is LPI-linked, and which caps and floors apply?

- How frequently do we update our liability benchmark to reflect changes in market conditions affecting LPI?

- In which inflation scenarios do we risk being materially over- or under-hedged?

- Do we have clear triggers for revisiting the liability benchmark and hedge design or do we instead avoid step changes by using a dynamic LPI benchmark?

A practical next step for IMAs

Indeed, for some schemes, the most effective step is to update the liability benchmark used in the IMA so it includes explicit LPI cashflows. Once LPI cashflows are embedded in the benchmark, the hedge can be managed against a dynamic reference point that naturally captures changing inflation levels and expectations through time.

The bottom line

The strategic direction for DB schemes is unchanged: reduce risk, improve certainty and progress toward an endgame (the long-term objective of securing benefits, typically via buyout, run-on, or a combination of both).

But as funding improves and hedge ratios rise, the impacts of approximation increases. If your hedging is against a static benchmark that does not explicitly reflect LPI cashflows, we believe that it is worth considering this evolution.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.