Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

India’s withholding tax cut could unlock billions in foreign inflows

We explore the potential impact of India’s tax cuts on investor returns, and how the move reflects a broader structural tailwind for local-currency emerging market debt (EMD).

Key takeaways

- Many emerging local bond indexes do not account for taxes on interest, resulting in a drag on realised returns

- India’s tax cut could result in 7 basis points (bps) of extra yield per year for index-tracking investors

- Taxes were once an underappreciated headwind, but their removal is transforming EMD local bonds into a more efficient and accessible asset class

Local currency EMD is an asset class where returns reflect both local and global forces. Performance is driven by fundamental factors like domestic interest rates, inflation trends and currency movements, along with the credibility of economic policy and the ebb and flow of foreign capital.

Yet beyond these familiar drivers, tax treatment[1] is an often overlooked but material influence on investors’ realised returns, participation levels and market access conditions. Different withholding taxes (WHT) and levies can significantly alter net-of-tax yields, shaping how attractive a country’s bonds are to global capital.

This blog explores the impact of tax policy on EMD local currency returns and flows – using India’s recent removal of withholding tax as a case study.

The invisible impact on returns

Many emerging local bond indexes do not account for taxes on interest. For example, the J.P. Morgan GBI-EM index assumes zero taxes, meaning any WHT will cause a drag on realised performance.

The below table provides an indicative WHT impact against the index, showing that pre-tax reform adjustments to Indian WHT, the impact on performance is approximately 21 bps p.a.[2] This is a meaningful amount in a low-yield environment.

Indicative withholding tax

| Weight (excl. zero coupon bonds) | Coupon | Tax | ||

| Brazil | 3.40% | 10.00% | 15.00% | 0.05% |

| Chile | 1.70% | 4.70% | 4.00% | 0.00% |

| Colombia | 3.80% | 8.80% | 5.00% | 0.02% |

| India | 10.00% | 6.90% | 10.00% | 0.07% |

| Indonesia | 9.90% | 7.20% | 10.00% | 0.07% |

| 0.21% |

Source: L&G analysis of J.P. Morgan index data as at June 2026. Based on the J.P. Morgan GBI-EM Index and ICAV fund structure.

Case study: India’s WHT “friction cost”

Prior to April 2026, non-resident investors in Indian government bonds faced one of the highest WHT rates globally (~10% on interest[3]), which had to be deducted at source. Combined with Indian capital gains taxes on bonds (previously 12.5% on long-term, 30% on short-term gains), this significantly reduced net returns for foreign investors and made India’s otherwise high yield less attractive.

High withholding taxes create a “friction cost” that can act as a deterrent for some foreign investors. Currently, foreign portfolio investors hold only ~2.6%[4] of India’s government bonds, a strikingly low share given India’s large bond market.

Expected impact of the tax cut

By eliminating both interest WHT and capital gains tax on foreign-held government securities from April 2026, India aims to spur tens of billions in new foreign inflows.

Analysts estimate that removing the WHT alone could unlock ~$20-25 billion[5] of stable inflows if paired with index inclusion. Indian policymakers see this as a way to ease balance of payments pressures and support the rupee via stronger bond demand.

India’s move is part of a broader pattern in emerging markets to adjust tax policies to influence foreign participation.

- Indonesia similarly halved its standard bond interest WHT from 20% to 10% in 2021 for foreign investors

- Colombia gradually slashed its WHT from 33% a decade ago down to 5% in recent years

- In Colombia’s case, foreigners now hold ~25% of local government debt, up from only ~4% before the tax cuts.

These examples underscore how lower taxes can significantly boost foreign participation and liquidity by improving net returns and signalling a more investor-friendly environment.

Structural uplift: tax reforms enhance EM local index performance

Emerging markets’ drive to reduce or eliminate withholding taxes is emerging as a structural tailwind for local EMD bond investors. Over the past decade, EMs have steadily trimmed levies to attract foreign capital, and India’s recent zero-tax reform for government bonds now caps this trend.

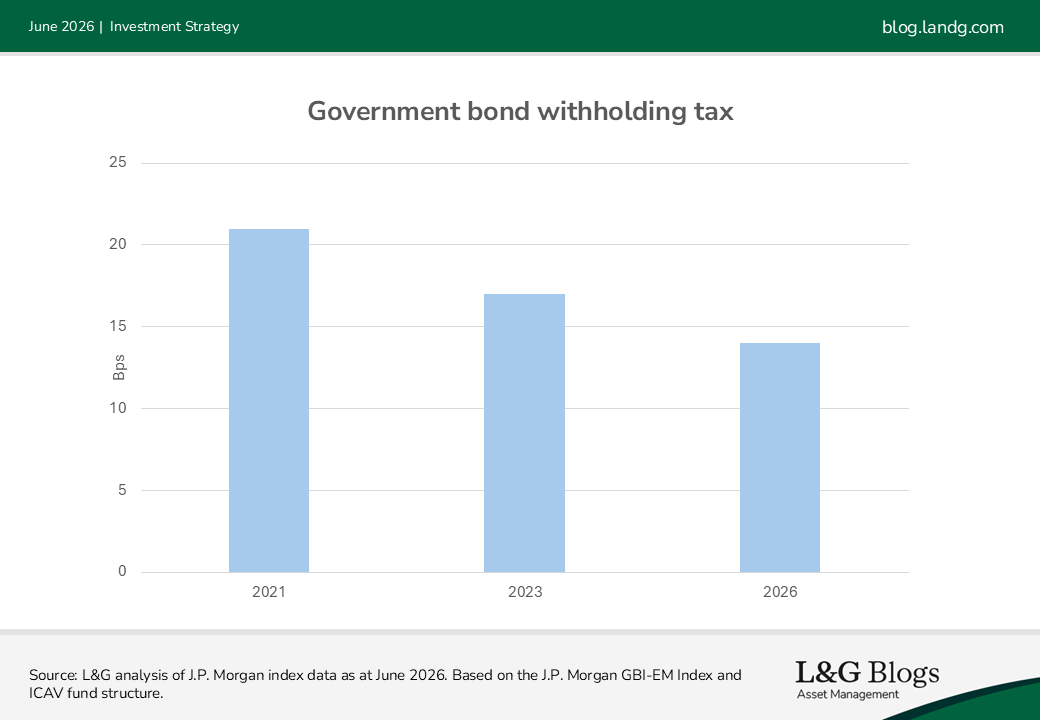

The practical upshot is that a longstanding “invisible” performance drag on EMD local bond portfolios is being significantly eroded. Historically, withholding taxes shaved roughly 0.2% per annum off realised returns on a broad local-currency index, as benchmarks assume no taxes.

Going forward, with India’s reform integrated, that aggregate tax drag is set to drop by around half – translating into ~7bps of extra yield per year for index-tracking investors. Reclaiming 0.1% of annual carry via improved tax efficiency is a meaningful boost to net-of-tax returns and compounding.

Crucially, this isn’t a one-off but part of a multi-year structural shift making EMD local markets more investor-friendly.

The elimination of tax frictions improves index replication efficiency – index portfolios can now capture a greater share of the index yield rather than steadily lagging by a tax-induced gap.

Long-term investor implications

Professional investors, who increasingly focus on net returns, will benefit from this enhanced carry. Over time, as more stable foreign inflows are encouraged by higher post-tax yields, markets can enjoy deeper liquidity and broader participation.

The chart below shows an indicative tax evolution for the J.P. Morgan GBI‑EM Index, suggesting a gradual reduction in portfolio-level tax drag (indices assume no taxes), largely reflecting increased diversification benefits and increased exposure to countries with more favourable tax regimes (subject to prevailing tax conditions).

While taxes were once an underappreciated headwind, their gradual removal is transforming EMD local bonds into a more efficient and accessible asset class. This tax reform trend delivers a small but tangible performance tailwind for EMD local currency portfolios, reinforcing the asset class’s appeal to global professional investors in the years ahead.

Sources

[1] Tax treatment is dependent on individual circumstances and is subject to change.

[2] Based on the J.P. Morgan GBI-EM Index and ICAV fund structure.

[3] Based on the J.P. Morgan GBI-EM Index and ICAV fund structure.

[4] Source: Bloomberg 9 June 2026.

[5] Source: https://economictimes.indiatimes.com/markets/expert-view/withholding-tax-removal-could-unlock-25-billion-in-bond-inflows-says-citis-aditya-bagree/articleshow/131504872.cms

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.