Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Equity valuations uncovered (part 4): How much of an edge do valuation tilts offer?

We explore the extent to which forming more accurate return expectations translates into efficient trading strategies. Whilst tilting using valuations alone may modestly boost risk-adjusted returns, we believe taking account of risk at the same time may substantially improve an investors’ edge.

Trading the future, one expectation at a time

In previous blogs, we’ve seen compelling evidence that valuation signals can help set expected returns on equities. This isn’t quite the same as creating an efficient trading strategy, though.

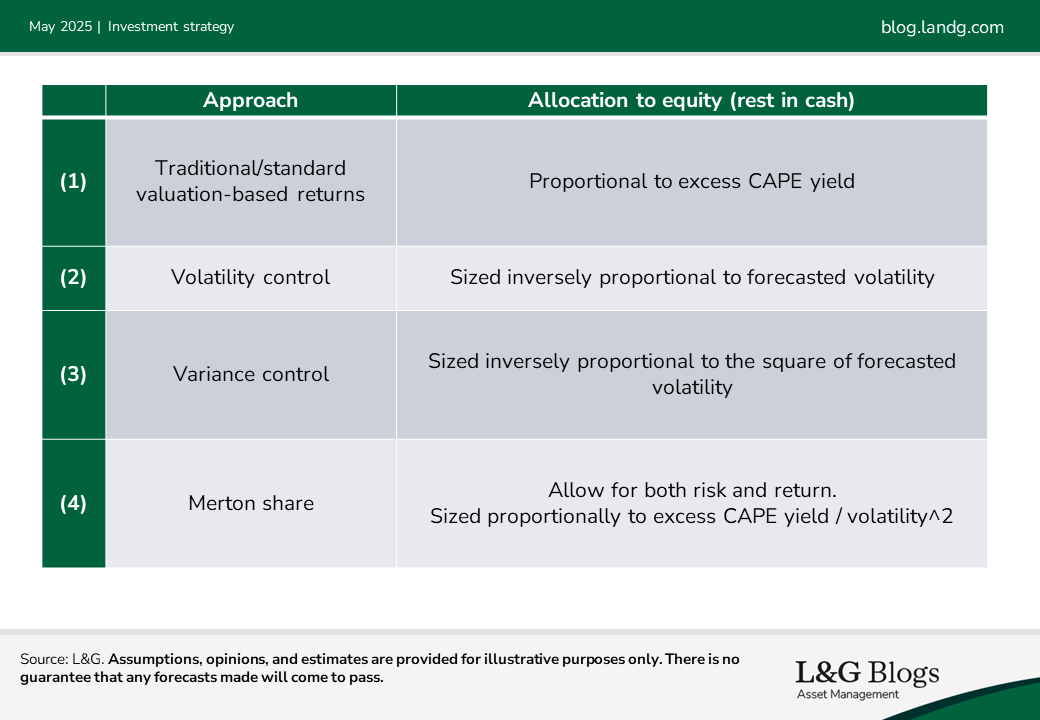

When it comes to portfolio construction, it’s easy to forget that expected returns are only half the story. As I explained in a blog last year, risk matters just as much. With this in mind, I investigated four different strategies combining equities with cash:

The first is a ‘standard’ approach investors could adopt to time markets, tilting in proportion to the valuation yield.

The second and third are purely risk-based and involve reducing allocations when risk increases, to stabilise risk exposure over time.

The fourth approach, the Merton share, requires some explanation! It involves sizing the equity allocation proportional to excess yield and inversely proportional to volatility squared. Under some reasonable assumptions this should lead to the most efficient strategy[1]. Up to scaling, it’s also equivalent to the Kelly criterion that you may have heard of. The Kelly criterion is used by some professional gamblers to size their bets, and by some investors.

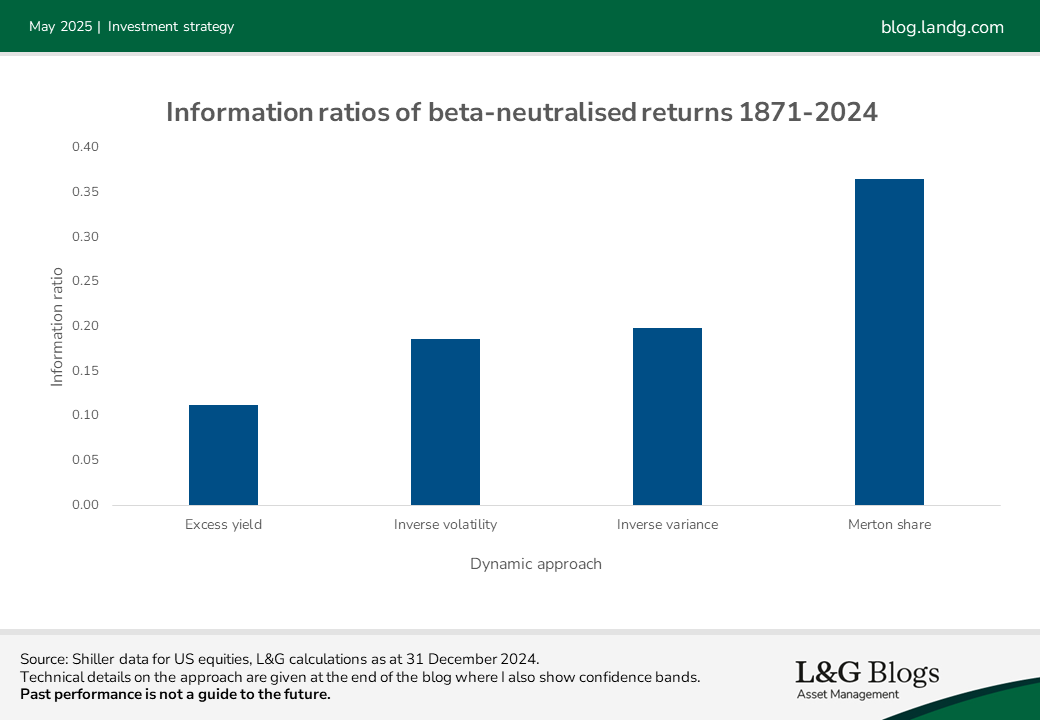

I tested these four approaches on as long a history as I could get my hands on, namely Shiller data (1881-2024) for US equities. A key question remained, however: how should I evaluate these strategies?

I settled on the information ratio of ‘beta-neutralised’ returns. Beta-neutralisation strips out any market exposure (or ‘beta’) from the strategy, so we’re left with the active tilts. The information ratio is then just the return per unit volatility of these. This essentially measures how efficiently a dynamic strategy adds value above a static one. The nice thing about this measurement approach is that it allows you to separate alpha and beta, rather than back-testing both together. If you want to size your tilts smaller, then you can scale them down and it doesn’t change the information ratio.

The below shows my results:

Starting with the first strategy, the information ratio is positive but modest, even neglecting trading costs. Other researchers have also found that simple market timing can struggle[2].

As you can see, both purely risk-based strategies do modestly well, despite paying no attention to expected returns.

But the big door prize is reserved for the Merton Share that combines risk and return forecasts. History suggests it offers a winning combination of traditional tilting and variance control. We must be careful with back tests, but it is reassuring that the theoretically optimal strategy did the best.

Why might contrarian investors neglect risk?

The above raises an interesting question: why is risk often neglected by those seeking to exploit valuation signals?

One potential reason is that with the benefit of hindsight, it becomes too easy to believe that once the market bottomed, there was only upside from that point onward[3]. This hindsight bias can make past downturns appear like obvious buying opportunities, leading investors to neglect the real uncertainty that existed at the time.

I also suspect it can stem from the belief that valuations are only important in the long run. For consistency, that suggests also considering long-term risk and, as long-term risk is relatively stable, this amounts to ignoring changes in risk. While this might sound reasonable, there are a couple of issues with this approach.

First, as I discussed in a previous blog, expected returns are most sensitive to valuations in the short run. Second, there’s a disconnect with the typical trading frequency - most investors have the flexibility to adjust their allocations frequently. If they can’t, it would be a stretch to call them dynamic investors! Trades based on 10-year risk and return assumptions may make less sense given the investor is unlikely to leave their portfolio untouched for an entire decade.

Fighting the tide

Another challenge for valuation-based tilting strategies is that the average level of valuation yields is only known in hindsight. As a result, investors may unintentionally drift from their long-term strategic allocation. For example, persistently richening valuations over recent decades has left contrarian investors under-invested in the equity risk premium. The yield normalisation they anticipated never materialised. While this doesn’t affect the efficiency of beta-neutralised returns (the information ratio remains unchanged[4]), it matters for maintaining the desired long-term equity exposure.

Where does this leave us?

Valuations can be important for setting expected returns, but this is only half the story when it comes to dynamic asset allocation. Our research suggests that also allowing for risk can lead to meaningful benefits, beyond what valuation signals alone can achieve.

Care is still needed though. With or without consideration of risk, relying too heavily on valuation signals can result in being meaningfully under or over-invested in equity markets in the long term versus strategic intentions.

Market timing certainly isn’t easy, but we believe can form a useful part of a dynamic toolkit including other sources of alpha, such as alternative risk premia and discretionary trades.

Stay tuned for the final installment in this blog series when I explore if valuations only matter in extremes.

Past performance is not a guide to the future. Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

[1] If return and variance expectations are unbiased then the strategy maximises expected quadratic utility, which leads to the highest Sharpe ratio over time.

[2] AQR believes that valuations are useful for setting expected returns and yet have disappointing performance in back tests. American economist John Cochrane notes that out-of-sample forecasting using dividend yields is poor even if all dividend yield variation comes from time-varying expected returns.

[3] This might be coupled with notions that cheap valuations act as a safety net. Cheap valuations are typically an indicator for high expected returns and high risk (not low risk)

[4] Because beta-neutralisation is performed with hindsight.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.