Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Deferred annuities in DC decumulation: understanding the trade-offs

Pension schemes are weighing whether deferred annuities can deliver the simplicity and longevity protection retirees need or whether the trade-offs in flexibility, pricing and investment risk could make them a costly form of security.

Key takeaways:

|

The decumulation phase in DC pensions presents a fundamentally different challenge from accumulation: while many retirees today cash out their pot or focus mainly on short-term drawdown, an increasing proportion are expected over time to seek a sustainable income for life amid uncertainty in markets, inflation and lifespan. With regulators now moving toward default decumulation pathways – and increasing expectations that schemes provide suitable, well-designed options for disengaged members – there is renewed interest in solutions that can offer simple, automatic later-life protection. Although the UK currently lacks a competitive retail market for deferred annuities[1], it is worth asking whether they could nonetheless play a constructive role, and what trade-offs their use would entail.

“Guided Income” versus “Drawdown + Deferred Annuity”

To explore, we compared two approaches, with the key distinction between them being when later-life annuity income is secured. The first is based on intellectual property we’ve developed over the last few years to create a solution we call “Guided Income”[2]. This involves:

- A dynamic spending rule

- A suitable investment strategy[3]

- Prompts for later-life purchase of an immediate (not deferred) annuity.

The spending rule links to how much annuity income they could secure if they annuitised, with adjustments for both the investment strategy and increasing mortality rates with age[4].

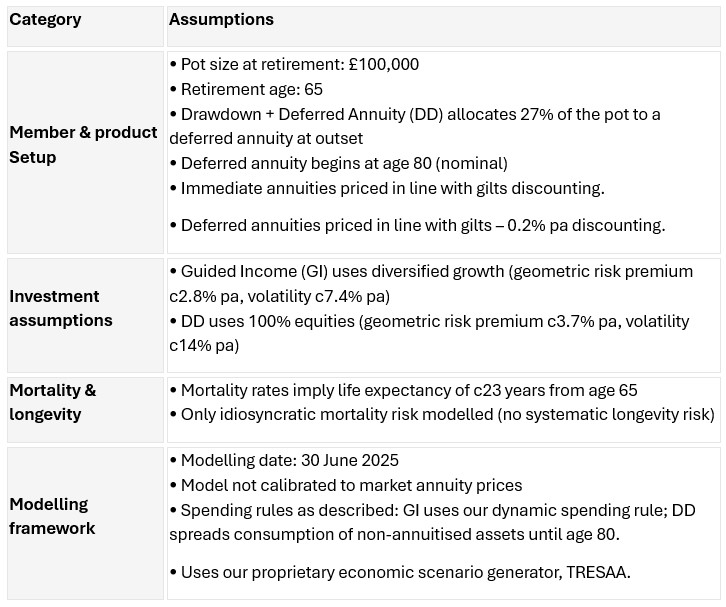

The second solution, that we call “Drawdown + Deferred Annuity,” involves a deferred annuity product. Rather than waiting until age 80 (say) and then buying an annuity, a portion of the initial pot at retirement – perhaps a quarter of it – is used to secure annuity income beginning at age 80. The remaining three quarters is used as income drawdown to provide a pension until then, with spending adjustments over time depending on market movements.

So how does Drawdown + Deferred Annuity compare with Guided Income? On the plus side we get:

- More longevity hedging. Deferred annuities pool longevity risk for longer than a wait-and-buy approach. It depends on the mortality rates assumed and the exact ages involved, but in isolation the extra longevity hedging could boost overall pension spending by c3%. This is thanks to “longevity credits” which are subsidies from those who live shorter than expected to those who live longer.

- Certainty in nominal terms of the amount they receive from age 80.

- Behavioural advantages: disengagement, cognitive decline or inertia could mean members using Guided Income never annuitise, even when it is in their best interests. It also removes the temptation to spend all their retirement assets before old age.

But there are drawbacks:

- Lower death benefits as a direct result of more longevity hedging (albeit the pensions falling under inheritance tax from April 2027 makes will make using pensions as an inheritance vehicle less attractive than it has been).

- Potentially “expensive”. While not a universal law, deferred annuities may be priced conservatively to compensate for financial and non-financial risks. If you assume that deferred annuities earn an implicit investment return that is 0.2% pa lower than an immediate one, rather than the same, then the c3% uplift to spending from extra longevity credits (due to hedging/pooling) above drops to c1% i.e. is practically wiped out. If the gap were 0.4% then the conservative pricing more than wipes out the extra longevity credits. Pricing depends on many factors, however, and will fluctuate. In some scenarios the gap could plausibly fall to zero or even negative, meaning there can be a tactical element to attractiveness.

- Increased sequence risk. The proportion of assets annuitised increases over time, hitting 100% at age 80, because income drawdown assets are spent first. Such a glidepath may make sense from a longevity-hedging perspective[5] but is inefficient in terms of growth exposure.

- Reduced diversification. The smaller capital base of the drawdown portion requires a more aggressive investment strategy to achieve the same expected spending outcomes as Guided Income. Given leverage constraints that can compromise diversification and efficiency.

- Compromised flexibility as members can’t “dip into” the deferred annuity. This creates consumption-smoothing issues if investment performance is worse than expected, as spending cuts must be concentrated into the years before age 80.

- Inability to buy an impaired deferred annuity, and we believe this is unlikely to change.

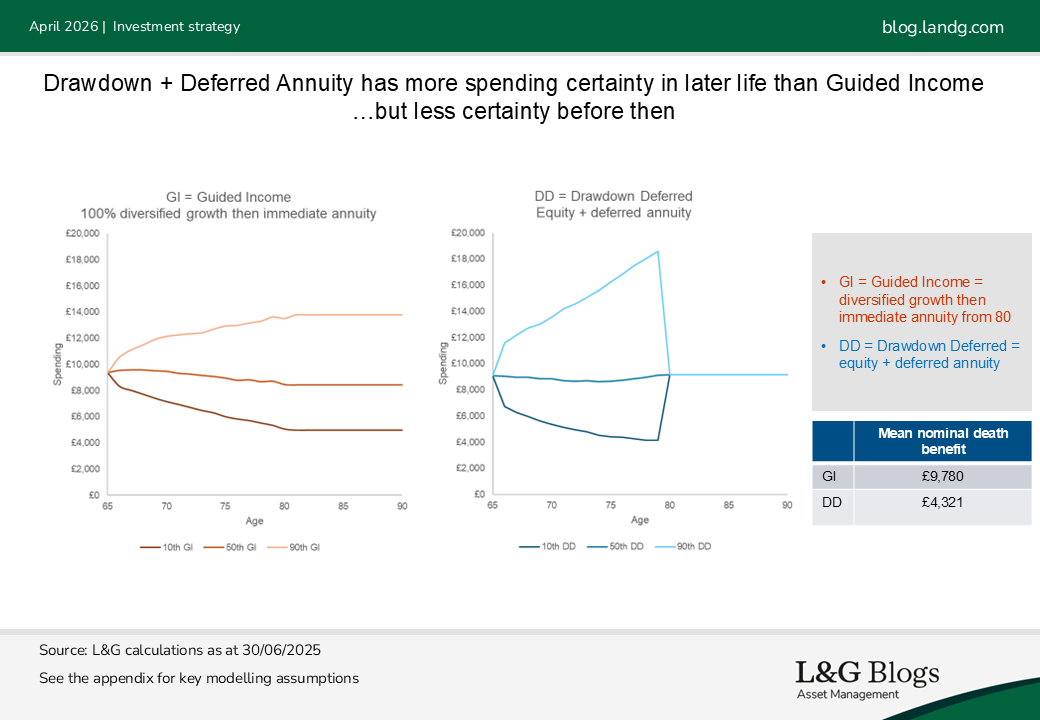

Modelling insights – engaged members

The chart below shows a “funnel of doubt” for spending levels - i.e. percentile spends by age - under the two approaches. For Guided Income, a diversified multi-asset strategy with only about half the volatility of equities was used. To obtain similar median spending outcomes for Drawdown + Deferred Annuity, its drawdown vehicle was 100% equity. Members in both solutions frequently change their spending based on changes in markets following prompts[6]. Those in Guided Income also annuitise at an appropriate time following a prompt.

As you can see above, nominal spending is more uncertain under Drawdown + Deferred Annuity before age 80 but certain after. However, in inflation-adjusted terms the spending power from age 80 is still risky. Death benefits are also lower – more than halved on average.

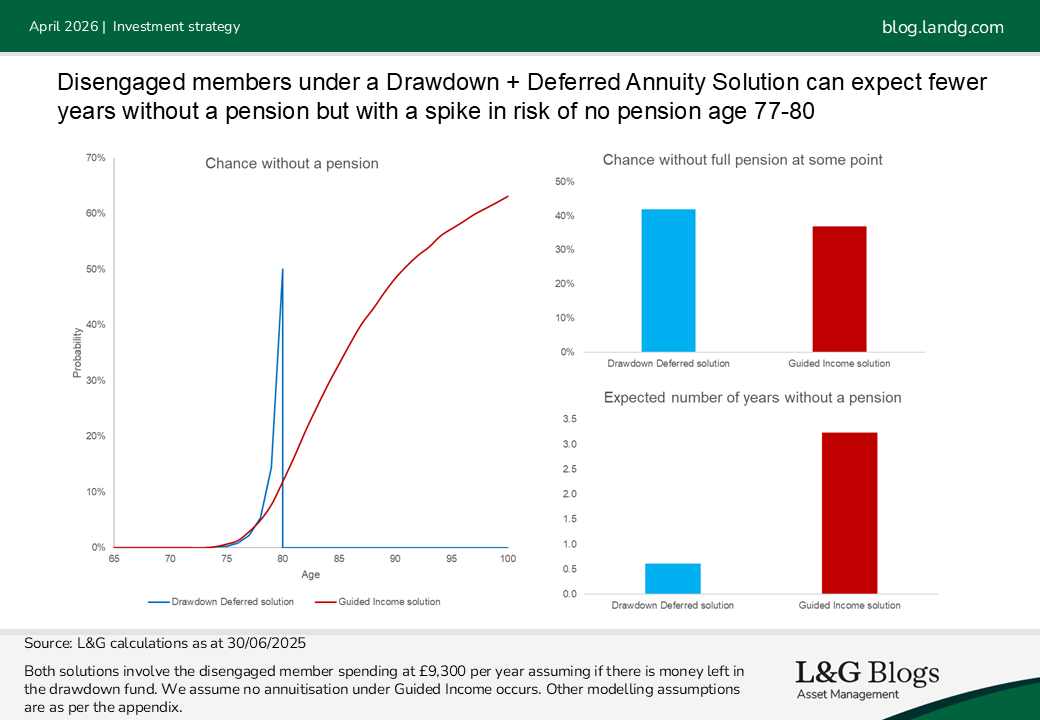

Modelling insights – disengaged members

The modelling shown in the previous section assumed members acted on prompts to change their spending and, for Guided Income, annuitise in later life. However, “disengaged” members may ignore or be unable to act on such nudging. For these members, we instead assumed they spend at the same constant level regardless (£9,300 per year) and never annuitise under Guided Income:

The Drawdown + Deferred Annuity solution has a much lower expected number of years without a pension. However, spending is at high risk for a few years prior to age 80. Conditional on survival, there is about a 50% chance of them running out of drawdown money before payments from the deferred annuity start.

Final thoughts

Guided Income and Drawdown + Deferred Annuity[7] manage retirement outcome risks differently.

The use of deferred annuities in DC decumulation has some challenges. Any uplift to lifetime income from increased longevity pooling is modest and is easily offset by conservative pricing. Deferred annuities also make it harder to smooth spending across retirement, increase exposure to sequence risk, and reduce the scope for diversification when trying to meet a given income target. These effects come alongside materially lower death benefits.

However, deferred annuities may offer value for disengaged members who maintain a constant spending level, as they provide some protection against failing to annuitise in later life, The trade-off is a material risk of having little or no income in the years immediately before deferred payments begin.

There are other advantages to hedging longevity risk earlier, rather than waiting until later life when cognitive decline may be a concern. One challenge with Guided Income is that, by age 80, a significant proportion of retirees may be poorly placed to judge whether annuitisation is appropriate. As such, while the UK does not yet have a competitive retail market for deferred annuities, they could suit some members - particularly those who feel uncomfortable with guided income and later-life decisions. There is no one-size-fits-all approach to retirement.

Appendix – key modelling assumptions

Key risks

The value of an investment and any income taken from it is not guaranteed and can go down as well as up, and the investor may get back less than the original amount invested. Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass. It should be noted that diversification is no guarantee against a loss in a declining market.

[1] This could be due to low demand (they seem unpopular), a small number of providers and scale issues, complex pricing and risk models over longer periods, and members potentially struggling to understand them.

[2] More on this to come in future posts.

[3] While we believe multi-asset diversified growth is ideal, the framework works with any growth strategy. However, an important feature of the proposition is that there is no de-risking into bonds prior to annuitisation.

[4] Higher mortality rates lead to more “mortality drag”. Mortality drag is the performance headwind you face when you don’t benefit from longevity pooling.

[5] the older you are, the higher mortality drag is, the more attractive longevity hedging is

[6] For simplicity in the DD solution, spending from the drawdown fund was assumed to be spread over the remaining period to age 80 whether it is better than expected or not. In practice better-than-expected could be spread over their future lifespan, whereas worse-than-expected cannot be because they can’t dip into the deferred annuity.

[7] We also considered the gradual purchase of deferred annuities but suspect this is unlikely to add value. Practical issues aside (members can’t pre-agree purchases, and staggered buying adds cost), Drawdown + Deferred Annuity already de‑risks into annuities over time (in percentage terms), so staged deferred annuity purchases may be unnecessary or counterproductive. Solutions involving drawdown (counterintuitively) ideally have uncertainty in later‑life income due to investment risk (necessary for expected excess returns) and spreading of its impact on consumption over future life. Gradual deferred annuitisation introduces uncertainty in later-life income but for the wrong reason – future deferred annuity pricing is currently unknown.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.