Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

DB investors in a higher-rate world

Strategies in the UK and US are evolving to capture market opportunities.

The following is an extract from our 2026 midyear global outlook.

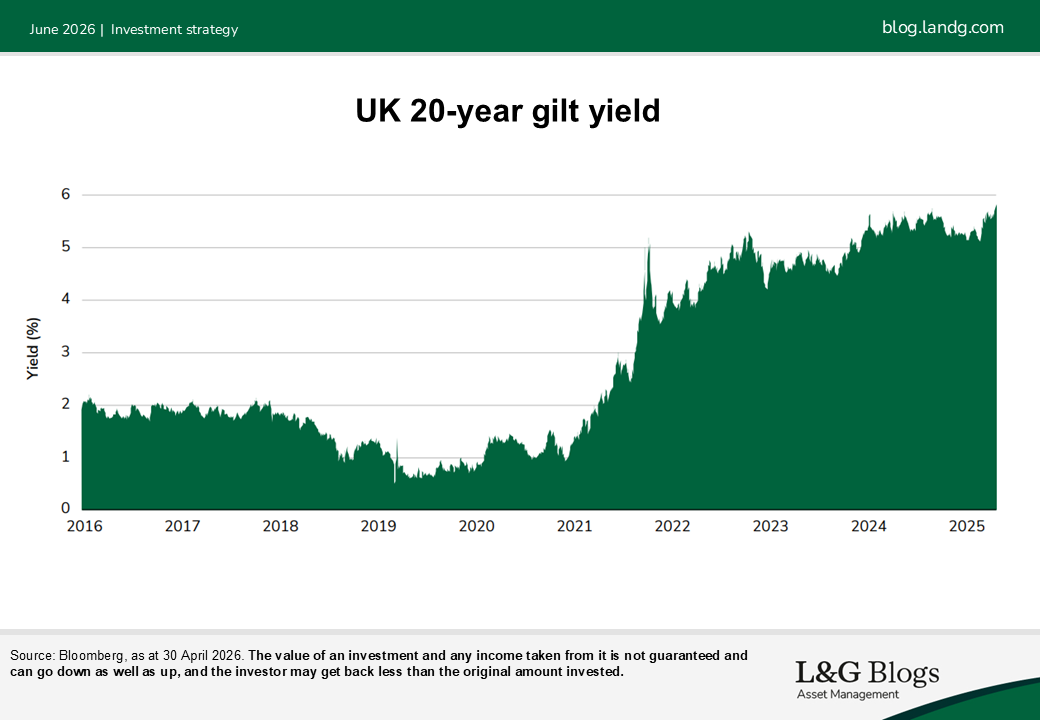

With UK yields near multi-decade highs, many defined benefit (DB) schemes have benefited from lower liability valuations and increased funding levels: 80% of schemes are now in surplus on a low-dependency basis and 60% are in surplus on an insurance buyout basis.[1]

This presents several opportunities for DB schemes to evolve their current strategy and potentially capture current attractive interest rate levels.

Strategic or value investor – or both?

DB schemes may view themselves as a strategic investor that values certainty, or as a value investor that’s prepared to take an active view in interest rates.

As strategic investors, they’d see interest rates as an unrewarded risk and aim to be hedged to their strategic asset allocation, which is typically set at the current funding level (and sometimes capped at 100%). Accuracy is important to preserve current high funding levels, so we are increasingly seeing clients apply:

- Funding level hedge ratio rebalancing, so the hedge ratio is managed to equal the funding level

- Regular liability accruals, so the hedge is increased as the value of liabilities increases

- Dynamic Limited Price Indexation (LPI) rebalancing, so that the liability target is dynamically adjusted to reflect changes in inflation

Meanwhile, a value investor could believe that today’s rates provide a potentially attractive level to capture and increase hedging. For schemes that use trigger-based levels to increase hedging, this may in fact be triggering already. Others may want to go further and proactively hedge some future accruals; e.g., hedge all of 2026 and 2027’s anticipated accruals at today’s market levels.

Furthermore, plenty of schemes have a dual endgame objective; for example, to run on for now but be opportunistically ready to execute buyout with an insurance company if pricing and governance align.

In our view, this presents a further opportunity as, while the scheme might be fully hedged against its technical provisions basis, it may be simultaneously underhedged to its buyout basis. In this way, the scheme becomes both a strategic and a value investor, able to seek value by choosing to strengthen its liability basis (i.e. increase hedging, seeking to ensure funding levels match liability levels calculated at a lower discount rate), thereby more closely hedging buyout pricing.

For more endgame insights for UK schemes, discover our latest interactive guide.

A more nuanced US picture

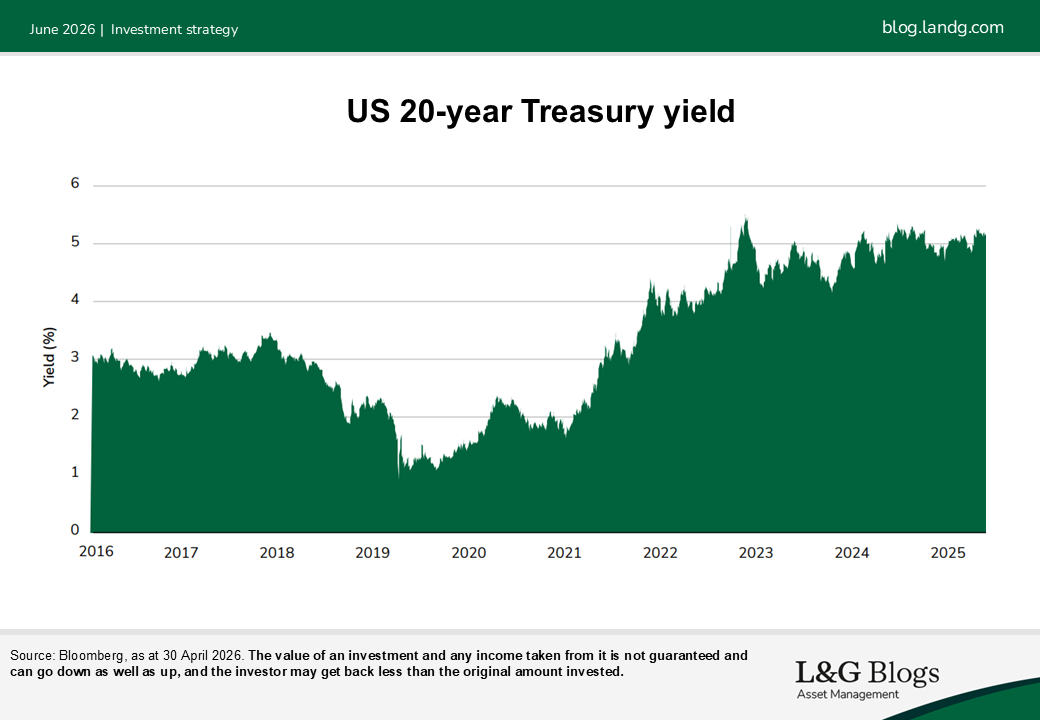

US rates remain elevated relative to the pre-COVID era, but they have not risen as sharply as in the UK. And so while government yields may be more topical in the UK LDI conversation today, US DB plans have been more focused on their growing fixed income allocation alongside rising funding levels. As such, the next phase of liability-driven investment (LDI) in the US is increasingly looking different compared to the traditional LDI strategy from 10 years ago.

Many US plans are already fully funded or in surplus and looking to complement the traditional LDI instruments of long corporates and treasuries. Expanding the opportunity set can help plans maintain their hedging and funded status volatility objectives while incrementally improving potential returns. Several building blocks are emerging as particularly relevant in today’s higher rate environment:

- Short-duration fixed income to enhance collateral efficiency and optimise liquidity and yield objectives

- Opportunistic fixed income to seek to improve diversification[2] and unlock uncorrelated sources of return potential

- Securitised assets for potential spread pick-up, while maintaining high credit quality

- Investment-grade private credit to increase yield potential and diversification

Indeed, many of these are also being considered by UK DB schemes in addition to considering interest rate hedging levels.

As such both in the UK and US, as DB plans continue to mature and funding levels remain strong, sponsors have more flexibility than ever to rethink how their fixed income allocation is constructed.

LDI has always been about seeking to minimise volatility and improve funded status outcomes. In today’s environment, achieving those goals increasingly means expanding beyond the traditional toolkit to build more diversified, resilient and return-aware fixed income portfolios.

For more details on the choices facing US plans, read our recent blog.

[1] The Pensions Regulator as at 31 December 2025.

[2] It should be noted that diversification is no guarantee against a loss in a declining market

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.