Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Responsible innovation

What evolutions in the responsible investment arena should DB trustees have in mind in 2026?

The following article is an extract from our latest DB outlook.

Trustees face an increasingly crowded responsible investment agenda in 2026, with multiple priorities competing for attention. Climate change remains paramount – particularly as commitments from some countries and companies begin to falter, underscoring the need for sustained action. Closely linked to this, nature-related risks such as biodiversity loss and water security are rapidly rising on the investor agenda. Both topics underscore how critical engagement remains for driving meaningful, real-world change.

Climate

The feasibility of the world meeting the objectives set in the Paris Agreement has been and will continue to be called into question. COP 30 has highlighted that despite general agreement about the importance of meeting these goals, the journey remains foggy.

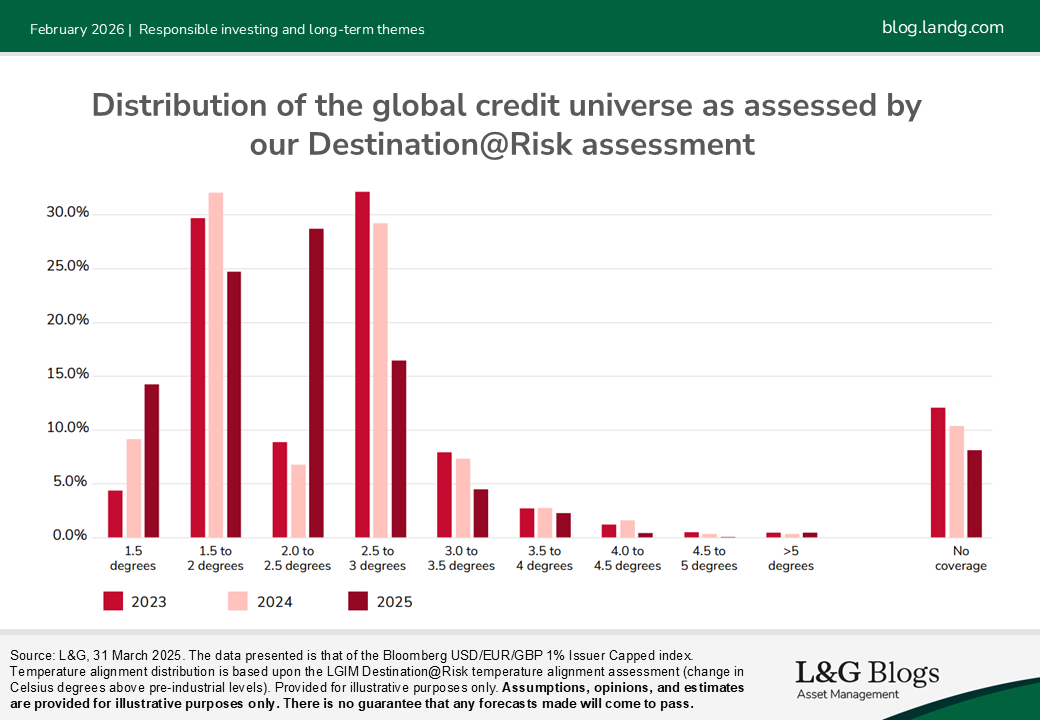

In the last three years we’ve seen encouraging progress made by companies to meet their climate commitments, with c.10% of the global credit universe improving to a temperature alignment of 1.5 degrees Celsius, although the majority of the global credit universe currently still sits above 2 degrees.

The removal of climate objectives for companies and countries may be fed through to the dataset more immediately, while divergence from previously predicted carbon emissions pathways will be fed through slower due to the lags used in carbon emissions datasets. Therefore, we believe that its important pension schemes continue to focus on climate and review the prudence of any objectives in the context of the real world.

Nature

Following roughly three years of climate reporting to meet TCFD requirements for the majority of pension schemes, many now recognize that this is only one piece of the puzzle that affects the resilience of our world as we know it. The Taskforce for Nature-Related Disclosures (TNFD), although voluntary at present, provides a framework for companies and pension schemes to leverage as focus sharpens on this topic.

The data to support many of the proposed metrics lacks the integrity that has been developed in the climate change reporting sphere. Much of the existing data relies on estimates with varying approaches to materiality across the industry, making assessment and management complex. However, company disclosures required in the UK and EU may change this in the coming years with EU anti-deforestation regulation, although delayed to December 2026, and work between TNFD and ISSB to build awareness and capabilities, which would improve scheme’s ability to invest in a manner consistent with their responsible investment principles.

Engagement

For trustees, engagement is a powerful mechanism for shaping the future by encouraging more sustainable, long-term practices from companies. Despite regulatory uncertainty and political pushback, engagement continues to be a cornerstone of effective stewardship. We believe transparent engagement strategies are essential for targeting sustainable returns in an increasingly complex global environment, where climate and nature, social factors, and corporate governance practices continue to present material risks to long-term portfolio performance. Our commitment to active ownership remains unwavering through our aim to support long-term value creation through addressing financially material and systemic risks and opportunities.

As we look ahead to 2026, there are three key forces we believe that have the potential to re-define the landscape:

1. Political tensions and the impact on country and company net-zero commitments:

When it comes to progress on climate goals, the global political and economic backdrop is challenging, while the energy landscape is fast evolving. Despite the political backdrop this year, the UK submitted new Nationally Determined Contributions (NDCs) in January, committing to ending petrol car sales by 2030 and reaffirming £11.6bn of international climate finance to be spent between April 2021 and March 2026, with £3bn earmarked for nature protection.[1] Over 2025 so far, the European Council have amended the EU Climate Law to introduce a binding intermediate 2040 climate target, strengthened the EU Emissions Trading Scheme with the EU Carbon Border Adjustment Mechanism and confirmed that in 2024 the EU contributed €31.7bn in climate finance to support developing countries. Bright spots remain in this stormy sky.

2. The AI data centre build-out and the energy required to support this:

Facing the prospective staggering demand for energy by AI data centres, we expect this will require more power generation than current energy infrastructure supports. This may encourage many to consider less clean energy sources to meet demand. The World Energy Outlook, published by the International Energy Agency, recently warned that global oil and gas demand will rise for the next 25 years without a course correction. This is despite investment in renewable energy continuing to ramp up, especially in China, where investment in renewable energy sources comprises 70% of total investment in energy in 2025 (IEA, World Energy Outlook 2025). As innovation in climate technology accelerates, the future energy-mix to support AI remains up in the air.

3. Investment opportunities in a world where adaptation is the answer:

The independent Climate Change Committee warned in October that the UK must prepare for weather extremes in the scenario that global warming reaches two degrees by 2050. With that in mind, should investors look to support more climate adaption solutions? With estimates of the adaption financing required between 2025 and 2030 in the region of $200-$300bn (Investment Opportunities in the Climate A&R Market | BCG) and stark warnings from the World Economic Forum, we believe this may present a potentially attractive investment opportunity.

The above article is an extract from our latest DB outlook.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass. While L&G has integrated Environmental, Social, and Governance (ESG) considerations into its investment decision-making and stewardship practices, this does not guarantee the achievement of responsible investing goals within funds that do not include specific ESG goals within their objectives.

[1] Source: https://assets.publishing.service.gov.uk/media/679b5ee8413ef177de146c1e/uk-2035-nationally-determined-contribution.pdf and https://www.gov.uk/government/consultations/phasing-out-sales-of-new-petrol-and-diesel-cars-from-2030

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.