Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Powering the digital world: what we learned from Data Centre World 2026

As AI scales, so does the need for resilient, power efficient data centres. Data Centre World reinforced that a clear opportunity sits with the enablers turning AI ambition into deployable infrastructure, and UK companies are playing an active role in that buildout.

In March, our Industrials equity analyst, Guy Kelly, attended Data Centre World to see first-hand how the sector is evolving. In this blog, he and UK equity portfolio manager Camilla Ayling share key takeaways from the event and what they could mean for investors.

A window into the world of data centres

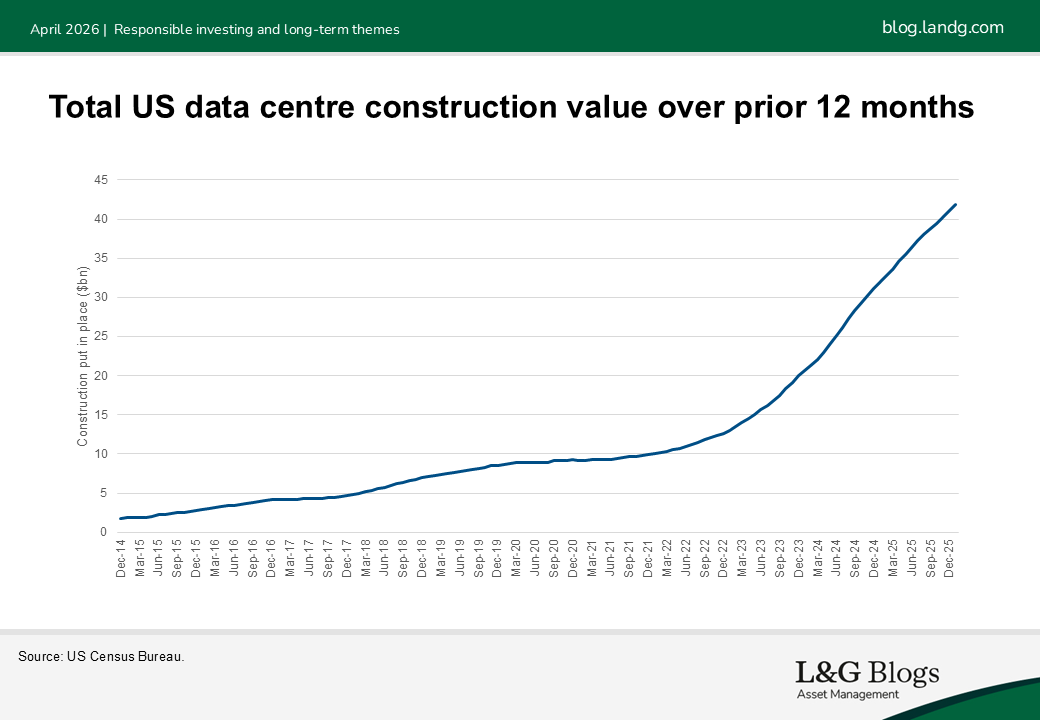

Data centres are fast emerging as core infrastructure for the global economy, powering everything from AI to cloud services and digital experiences. Each year, Data Centre World (DCW) comes to London’s ExCeL Centre, bringing together industry leaders to showcase the latest technological developments. From our perspective, this trade show importantly offers a window into how investment is accelerating both in scale and speed, alongside rapid innovation in enabling technologies.

Keeping pace with AI heat loads

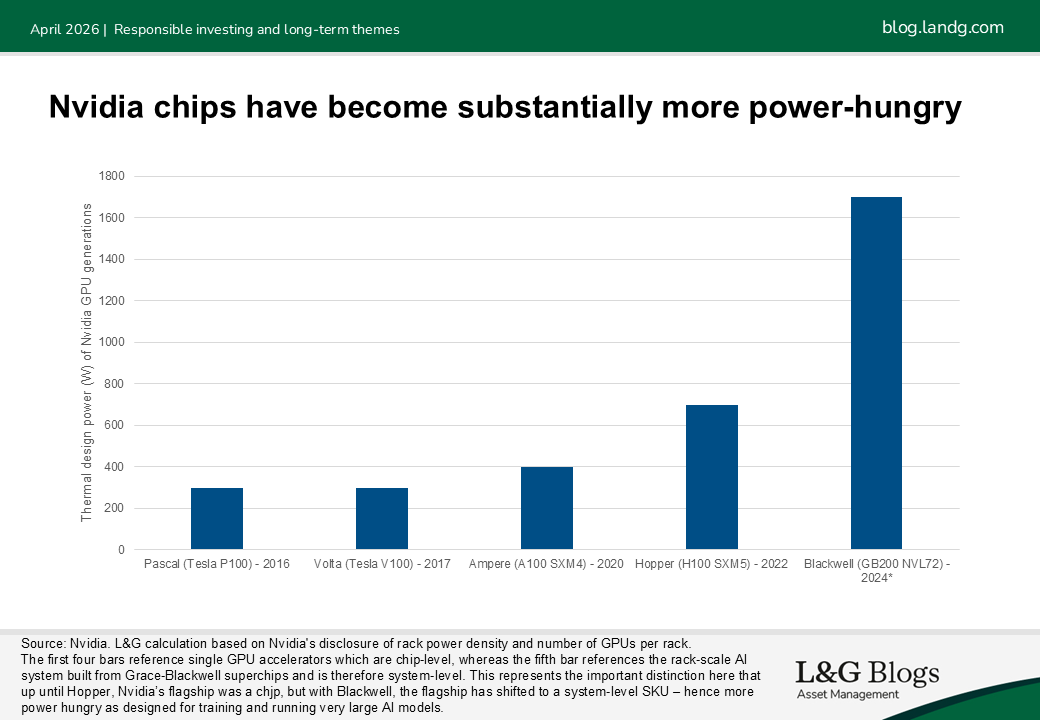

One trend that stood out was the surge in liquid cooling solutions, as well as the number of companies trying to position themselves as liquid-cooling providers. As chips become more powerful, AI-heavy workloads raise power density and heat. The result? Traditional air cooling no longer keeps up.

At DCW, many exhibitors showcased liquid cooling systems designed to deliver higher efficiency over these traditional cooling methods. Our industry research uncovered that ‘direct-to-chip and immersion cooling systems can reduce cooling-related electricity use by up to 40–60%’.[1] Companies at DCW such as nVent* highlighted how fast standards are changing, driven by AI chipmakers like Nvidia*. From our portfolio management perspective, we have been hearing the same theme in our conversations with companies building data centres. Accordingly, we believe cooling is increasingly becoming a central infrastructure policy and planning topic, moving from an engineering detail to a licence to operate.

The shift to higher voltage power

Another takeaway from DCW was the industry’s shifting power architecture. Legrand* highlights that while advanced 800‑volt DC sidecars[2] or direct-to-chip power represent the future, they are use-case specific and primarily relevant for ultra high‑density AI workloads; therefore may be limited to a subset of new data centres this decade.[3] However, that could depend on developing technology that does not currently exist. The push towards higher voltages is again being led by Nvidia*, reinforcing the extent to which chipmakers are increasingly shaping the direction of infrastructure decisions.

The hidden infrastructure behind AI performance

At DCW power reliability was a focus. Siemens Energy* is working with customers on ‘hybrid power’ models combining onsite generation with grid connectivity, an important development given persistent grid connection bottlenecks across the UK. One

Key innovation to highlight is Prysmian’s* ultrathin fibre bundles[4] bound into cabling, which point to the scale of engineering required to support the next wave of AI workloads. Technology strides like this enable more data-carrying fibres into limited spaces while remaining fully compatible with existing networks. To further increase network capacity, Prysmian* can also embed sensory fibres enabling the electric utility industry to catch up to its gas and water peers in its ability to monitor networks.

Portfolio manager perspective

Back at the desk, running through the extensive list of DCW attendees, we are encouraged by the breadth of UK companies that exhibited. Whether homegrown specialists, small privately owned firms, or FTSE All‑Share listed businesses generating an increasing share of revenues from data centres, the common thread was clear: the UK is not merely observing this innovation cycle, it is contributing to it.

A good example of this point was the recent update[5] from UK high-speed power and data connectivity solution provider Volex*. This FTSE AIM listed business communicated an upgrade to analyst consensus expectations driven by demand stemming from AI applications. Its full year data centre revenues are now expected to be approximately double the $118 million achieved in the prior year[6], and we view the source of this demand as an enduring structural tailwind.

Where competitive advantage is really being built

As AI adoption accelerates, so too does the demand for resilient, power efficient digital infrastructure. Our key takeaways from DCW echo Dr James Tyrrell’s conclusion in his recent blog: competitive advantage is increasingly shifting towards power availability, permitting and execution.[7]

With that framework in mind, we look to discover companies that offer sensible exposure to this expanding theme for our portfolios. We believe the most compelling investment opportunities are not those simply riding headline AI enthusiasm, but those sparking and enabling the essential technologies that make AI deployment possible in practice. And, they can even be found on our shores.

* For illustrative purposes only. Reference to particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

Assumptions, opinions and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass.

[1] AI-driven cooling technologies for high-performance data centres: state-of-the-art review and future directions - ScienceDirect, this statistic is compared to traditional chilled-air methods

[2] 800 V DC sidecar = a rack‑adjacent unit that converts incoming AC power into 800 volts of direct current, which is then fed straight into the compute rack.

[3] The road to 800VDC: Why it’s coming – and what we still need to figure out - DCD, Legrand, 2026

[4] These fibres are 160-micron, roughly twice the width of a human hair. This is around 36% thinner than traditional optical fibres, achieved by keeping the glass inside consistent (125-micron) but using a thinner polymer coating.

[5] RNS Announcement - Volex, 25 March 2026

[6] Ibid.

[7] L&G Blogs: Digital infrastructure: AI keeps the pressure on, 25 March 2026

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.