Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Which housing markets are most vulnerable to rising rates?

Rising interest rates will hit housing markets. But which countries are most exposed? Our index offers some answers.

Central banks have scrambled to contain the well-documented rise in global inflation, yanking interest rates higher in a short period of time.

Across much of the developed world, the pace of hikes has been unprecedented, with some – such as Canada and Sweden – opting for 100 basis points (bps) in one go. Upward moves of this size have not been seen in decades.

The space race

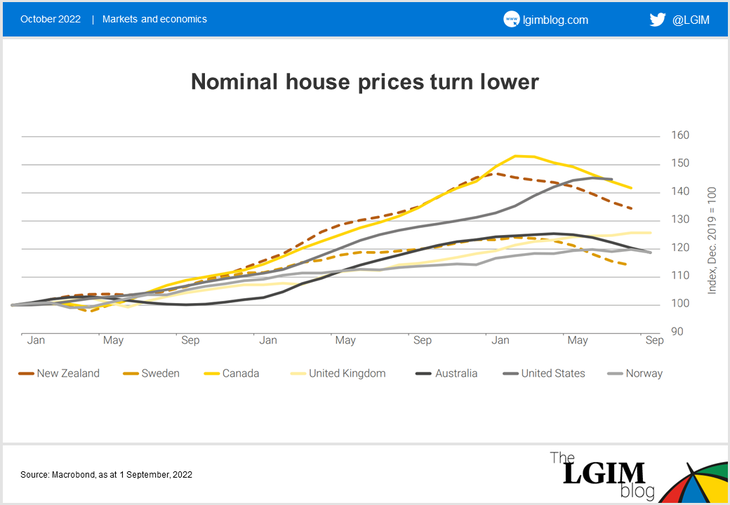

But consumer price inflation isn’t the only thread that many countries share: a sharp rise in house prices also became very widespread.

This was partly driven by policy stimulus unleashed during the pandemic that kept interest rates low, as well as pent-up demand during the lockdown phase and a preference shift towards larger living spaces as more people spent time at home.

Now interest rates are rising rapidly, we are starting to see a reversal in several housing markets. With plenty of evidence that housing cycles can be a threat to financial and macroeconomic stability, it’s worth a closer look.

How the index works

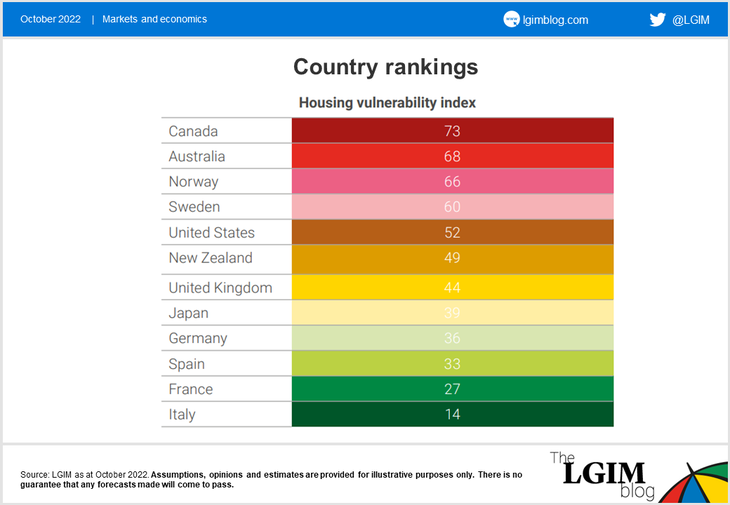

Some countries are more exposed to changes in interest rates than others. To assess the extent to which they differ in this regard, we have compiled a housing vulnerability index, based on a range of indicators. These include price metrics, relative debt serving burdens, residential investment and mortgage market structure, among others.

As illustrated below, for a given interest-rate shock, Canada, Australia, Norway and Sweden appear to be some of the developed markets most exposed to higher rates. The US and UK are in the middle of the pack, while Japan and the major euro-area countries look the least vulnerable.

However, the magnitude of interest rate increases will also vary by country, so this needs to be overlayed, too. Moreover, real incomes also play a significant role. For example, the squeeze on real incomes in the UK is more severe than that in the US; as such, the housing market in the former is likely to experience a larger downturn than that of the latter, in our view.

What this means for rates

We do not think the price declines witnessed thus far are enough to prompt an imminent about-turn in rates – indeed, many central banks have clearly signalled their desire for both housing markets and inflation to cool significantly.

But we believe the more vulnerable countries are likely to see an earlier end to the rate-hiking cycle, as spillovers from their housing markets exacerbate economic downturns and the accompanying disinflationary forces.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.