Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

UK Spring Statement: has the OBR missed tariff risk?

Wednesday’s Spring Statement contained few macro surprises and reiterated commitment to fiscal rules. But the likelihood of US tariffs was notably absent from Office for Budget Responsibility (OBR) forecasts.

UK Chancellor Rachel Reeves’ first order of business in Wednesday’s Spring Statement was to plug the hole in the finances left by higher interest rates and weaker growth.

These had more than eliminated the £9.9bn of fiscal headroom available to the Chancellor. But previously announced spending restraint (welfare, admin, switching foreign aid into defence investment) and, notably, pro-growth planning reforms have fully restored this. Projections that fiscal policy will be tightened by around ½% of GDP per year in coming years can be expected too subdue growth.

With the above measures widely flagged before the statement, attention was focused on the extent to which the Office for Budget Responsibility (OBR) would cut its relatively optimistic growth forecasts. Although it did so for 2025, the OBR ultimately argued near-term weakness is largely cyclical and growth will rebound as trade uncertainty and interest rates fall.

Downside risks to growth forecasts

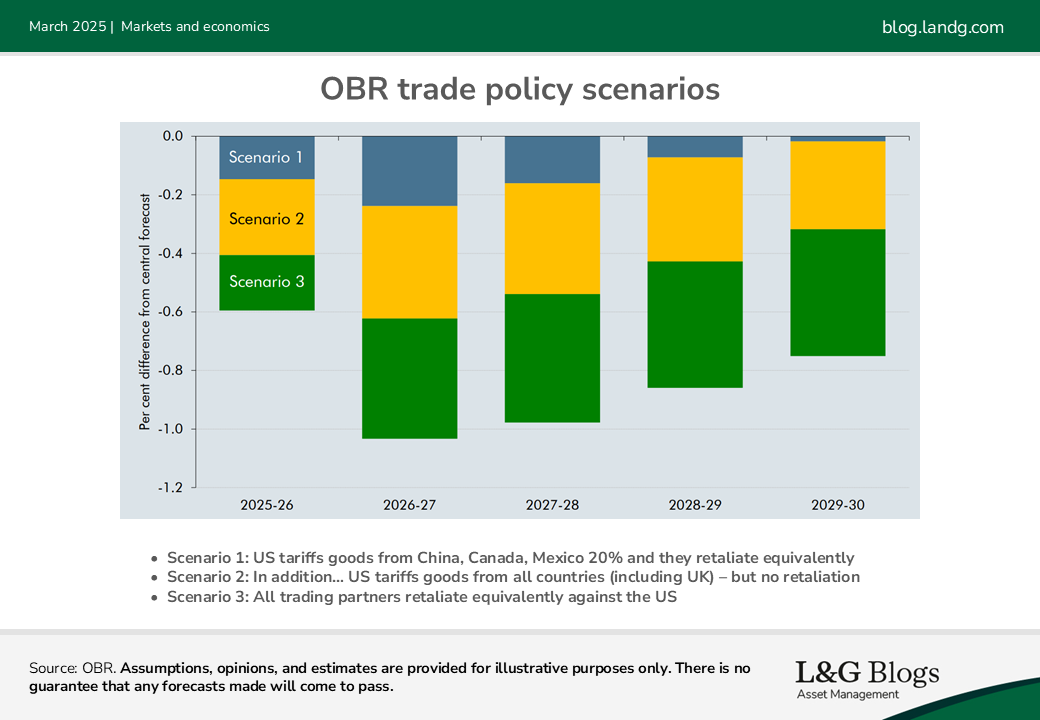

The key point of contention is President Trump’s tariffs. The OBR assumes away trade-war concerns. “Our central forecast does not explicitly account for the impact of recently announced tariff increases by the US and other countries,” the office said.

The OBR’s growth forecasts remain more optimistic than consensus or the Bank of England.

Comparison of forecasts for GDP, inflation and the unemployment rate

Source: OBR.

The risks to UK growth and the public finances are therefore to the downside, in our view, depending how long and how deep US tariffs turn out to be. Even if the UK is not directly tariffed, the OBR acknowledges it could still suffer collateral damage from global uncertainty and a worse growth/inflation trade-off.

Trump’s immigration policies are likely to add to this, in our view.

We expect déjà vu in the Autumn as a potential escalation of US tariffs keeps global growth subdued.

Implications for the gilt market

Despite maintaining the headroom against the fiscal rules at exactly £9.9bn, the government is still looking to borrow around £50bn more over five years than had been planned in October. Why the increase in borrowing despite no change in headroom?

First, the welfare reforms have essentially zero impact on the public finances until 2027/28 as all the cuts are backloaded.

Second, the increase in capital spending (defence equipment) still needs to be funded even if it falls outside of the fiscal rules. The overall financing requirement of the government remains large, with net borrowing needs of nearly £450bn over the next five years.

The fact the Chancellor took action to stick to the fiscal rules in the wake of a weaker starting position should be welcomed by the gilt market. She could have ducked the issue, saying the outlook was uncertain and see how things pan out in the autumn.

There was also some speculation the UK could fudge the fiscal rules to boost defence spending. But there was no sign of this.

One helpful measure was to shift issuance away from the more expensive long end of the curve (13.4% versus the expected 16.5%). The market reaction was a flattening of the gilt curve.

A pro-cyclical UK

Assuming the Chancellor sticks to the fiscal rules, this makes the UK economy pro-cyclical: weaker growth leads to more tightening, which leads to weaker growth and downward pressure on policy rates.

This is contrast to Germany, which – because it saved for a rainy day – is offsetting trade-war concerns by ramping up investment in infrastructure. Unlike the UK, its borrowing costs remain in line with potential GDP growth.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.