Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

T-bill stakes: of markets and accords

Exploring President Trump’s unconventional paths to securing dollar-treasury dominance.

It was under the gilded ceilings of the Elysée palace in 1965 that the first attack on US dollar dominance was launched. France’s then-President De Gaulle, in his Criterion speech, stated that dollar dominance led to “expropriation” of non-US companies, generating imbalances harmful to economic stability and an accrual of US power. While his proposed solution – a return to the gold standard – went nowhere, many other countries since have shared De Gaulle’s resentment of the US-backed dollar-treasury hegemony.

Egged on by foreign frustration at the dollar’s pre-eminence, watchful commentators have fretted about its dethroning as rivals launched efforts to reduce dependance on the dollar in 1965, 1979, 1999, 2005 and 2024. Despite these efforts, so far, king dollar remains in place. But for how much longer?

Amid all the turbulence of the Trump tariffs, can we expect challenges to the treasury market and the dollar to get more viable? In the second of this two-part series, I look at potential alternatives to treasuries and the dollar, alongside potential global bargains President Trump might strike that assuage or aggravate those who use it.

You’re gonna need a bigger market

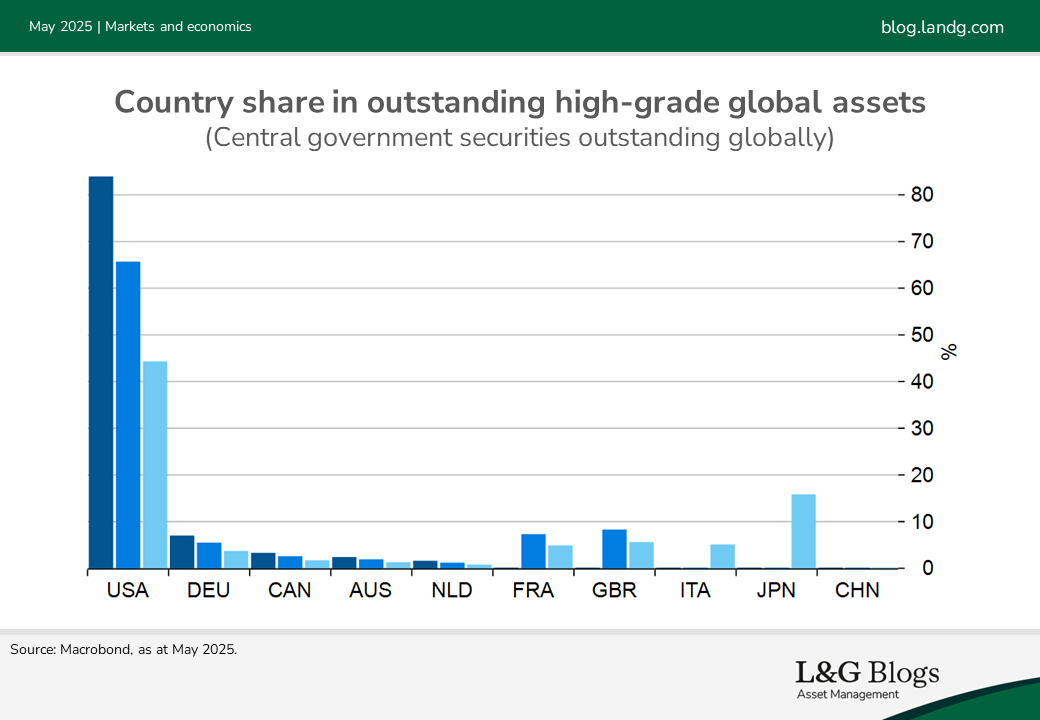

The dollar’s own supremacy is staggering to contemplate, comprising over 80% of all trade financing, 50% of SWIFT transactions and a little over half of all FX reserves. While US dominance of real activity has diminished (from a 33% GDP share in 1999 to a little under 25% now) other major currency prospects appear to remain inadequate. China’s strict capital controls, likely necessary for financial stability, stunt investor enthusiasm for use of the CNY, while the Euro-area’s fragmentation prevents a single, universal issuer comparable to the US Treasury.

For the treasury market, the depth and universality of acceptance across domains remains its strongest feature. Although European and Japanese markets are the US’s closest rivals in size, both remain relatively low yielding environments for investors to place capital. Dollar dominance also makes it comparatively cheap for foreign investors to hedge their USD earnings, making it easy for investors to insulate themselves from currency exposure.

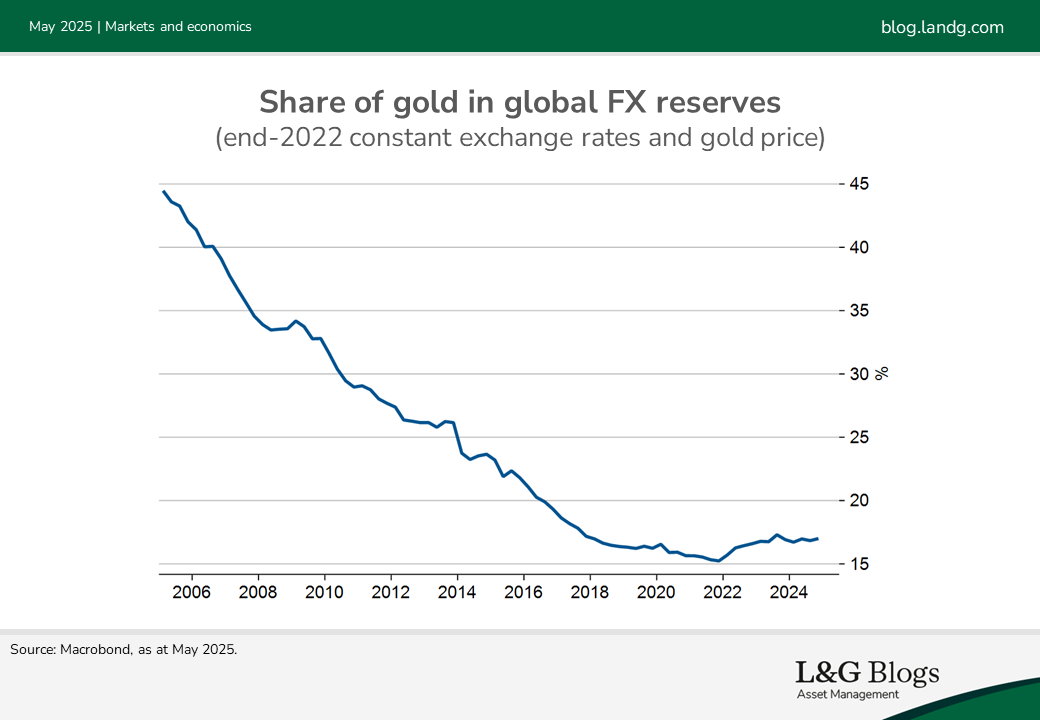

If not treasuries, perhaps other assets instead? Gold, proposed in De Gaulle’s 1965 address, remains a possible option. The stock of gold reserves in central banks has been rising since the end of the financial crisis, and its volume share in global FX reserves has risen slightly since 2022. Nevertheless, the asset struggles as it doesn’t produce a yield (unlike US treasuries), and physical possession of the gold (which often is not in the country that owns it), limits security.

Crypto is similarly often touted as an alternative to the dollar-treasury nexus, offering more anonymous, secure and inflation-protected asset. Sadly for its enthusiastic backers, it doesn’t throw off any yield, remains highly fragmented and frequently dislocates during periods of stress.

Dancing the macro in Mar-a-Lago

The factors underpinning the dominance of US treasuries as a universal asset lasted long before President Trump, and look set to outlast his second term. Nevertheless, a potential pan-national deal (a so-called ‘Mar-a-Lago accord’) involving treasuries could throw further uncertainty into the market. What might these deals be?

One focus is a currency-led. The idea is of coordinated dollar depreciation, echoing the Plaza Accord of 1985, reducing foreign financing needs by lowering trade deficits and easing pressure on treasury markets. Such a coordinated move, however, would rest on cooperation with China, which we believe is unlikely to willingly let its currency revalue as Japan did in the initial Plaza Accord.

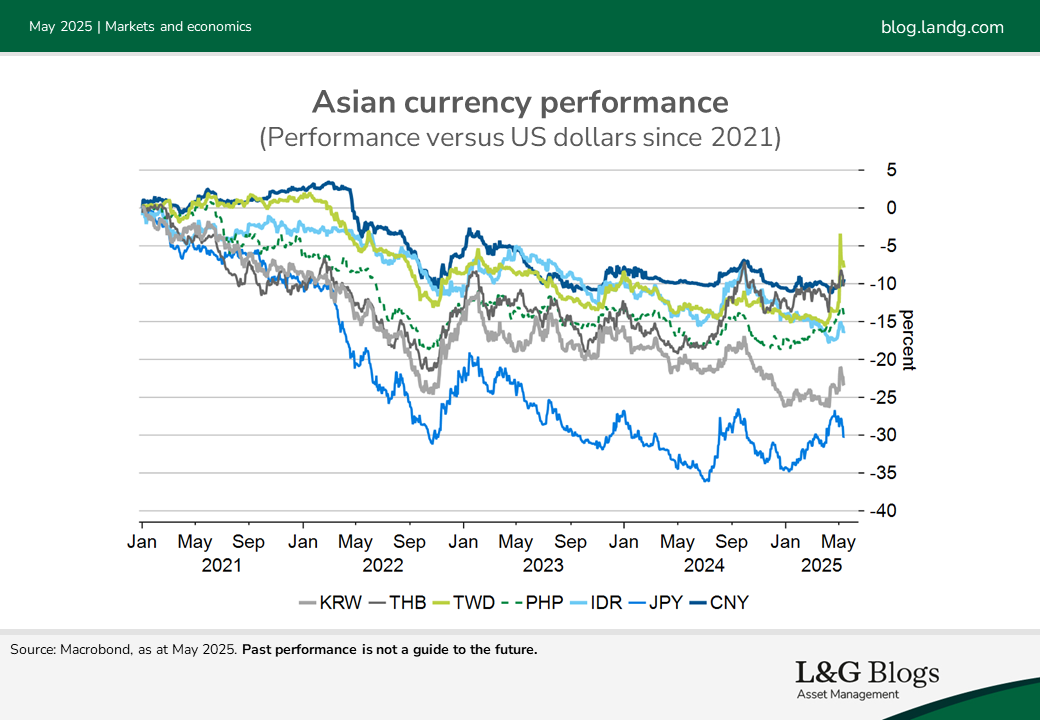

More possible is a Plaza Accord-lite, whereby Asian currencies are encouraged to revalue against the dollar, encouraging some depreciation and encouraging US competitiveness. Indeed, there is some evidence selective revaluation is happening in Asian currencies.

The second focus is more treasury-led. The US could try a restructuring of US debt to remove high-yielding short-term debt, swapping it for 100-year zero coupon bonds that radically reduce short-term financing needs, while preserving market functionality. However, this would substantially undermine trust in US treasuries market, wrecking its credibility and heightening incentives for others to find an alternative. What’s more possible is a change in domestic tax rules to tax interest income on central bank treasury holdings; this is something other countries already do, and would not be a radical departure from international norms.

Ultimately, whether by diplomatic accords reminiscent of the Plaza Agreement or novel fiscal measures, the search for a stable treasury market will ultimately hinge on retaining its deep pool of buyers. As the former piece illustrated, the treasury market has changed radically over the last 20 years, let alone the last 60. Today’s unconventional proposals underscore the crucial importance (and increasing difficulty) of keeping both investors committed and fiscal burdens low as the geopolitical environment turns harsher.

Which could be the implications for portfolios?

While threats to the dollar-treasury nexus remain quiescent, we believe President Trump’s actions will continue to inject volatility into the treasury market, as investors query the true risk embedded in US assets. We are minded to fade short-term rallies in front-end treasuries at this value, albeit looking for an attractive opportunity to re-engage if valuations become stretched in the opposite direction.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.