Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Private equity and private credit: A recovery and a party?

In private equity, we’ve observed a lack of valuation correction and concentrated growth. Meanwhile, private credit is defined by softening yield and tight spreads, meaning asset selection will be key in 2026.

Private equity – still in recovery mode

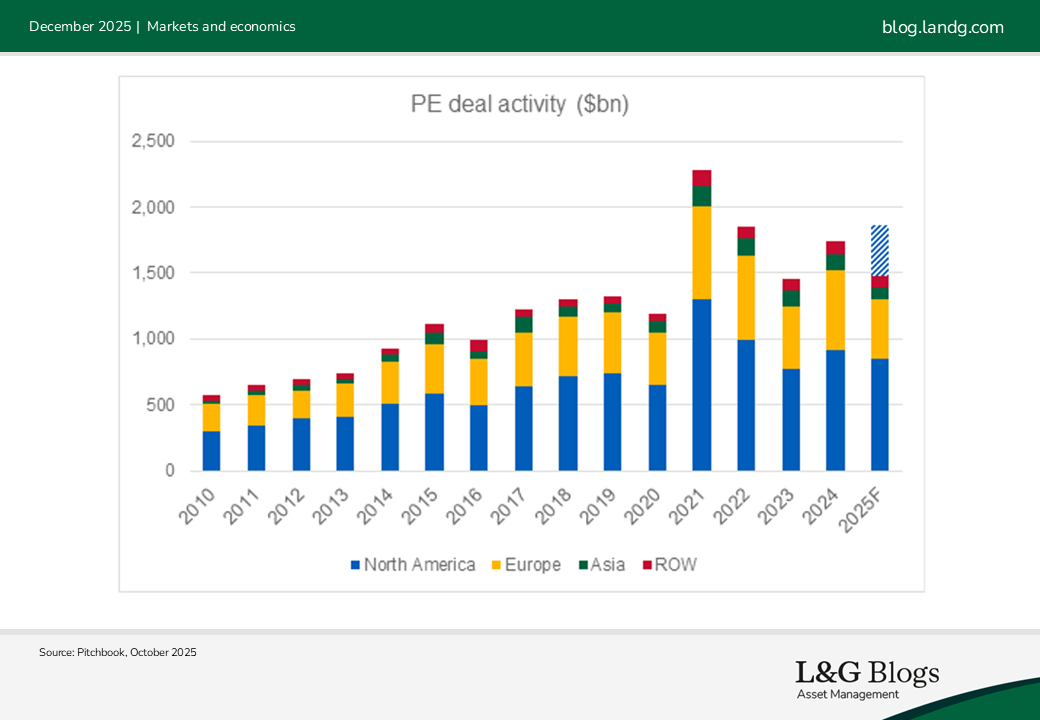

Private equity deal activity bounced back in 2025, boosted by a recovery in M&A transactions. Despite tariff uncertainties and a strong European equity market, the US continued to dominate transactions thanks to strong interest in AI and other technology sectors. Exit activity has also been higher than 2024, although a portion of these are to continuation vehicles rather than ‘true’ exits.

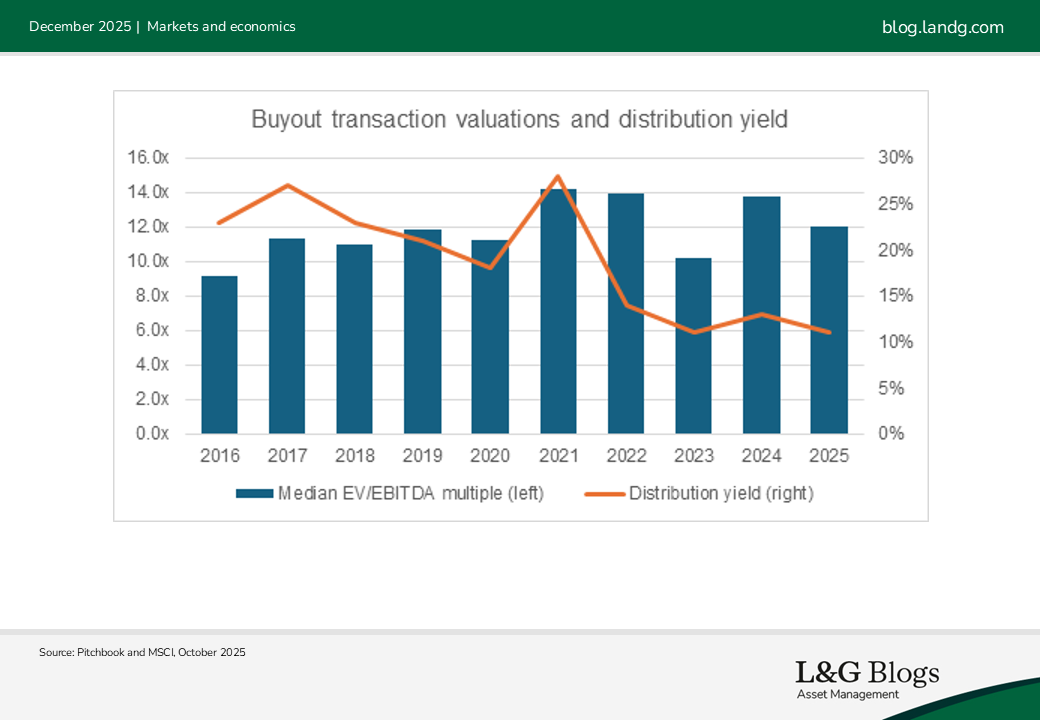

Despite positive signs, market conditions remain challenging. Transaction activity has focused on higher-quality assets, which skews valuation data and may not represent the true valuation of the wider universe. Distribution as percentage of AuM back to investors is still at an historically low level. The lack of distributions continues to put pressure on managers to return capital to investors and unlock new commitments.

As we go into 2026, we believe deal activity is likely to increase further in the absence of a global recession. We see this driven by the M&A rebound, easier financing conditions and growing use of liquidity options such as continuation funds. This may accelerate price discovery, narrow the valuation gap and increase distribution back to investors, which should boost fundraising.

Fundamentals continue to be robust underpinned by strong earnings growth, but it is concentrated in a narrow band of sectors such as technology and defence which means investor sentiment is highly vulnerable to the AI bubble bursting. In addition, there is ongoing uncertainty over the full impact of tariffs on the US economy. This drives us to retain a cautious outlook on private equity.

Private credit – is the party still going?

Before we delve into the latest developments in private credit market, it is worth re-iterating that like public credit, private credit consists of both investment-grade (IG) and sub-investment grade (sub-IG).

The former has been a core component of insurer and long-term institutional investor portfolios for decades due to its high credit quality and long-term cashflows. The latter, of which direct lending is a major component, has grown rapidly over the last 15 years as banks pulled back lending after the Global Financial Crisis. Both are over $1tn in size and global in nature, although the US is by far the largest market.

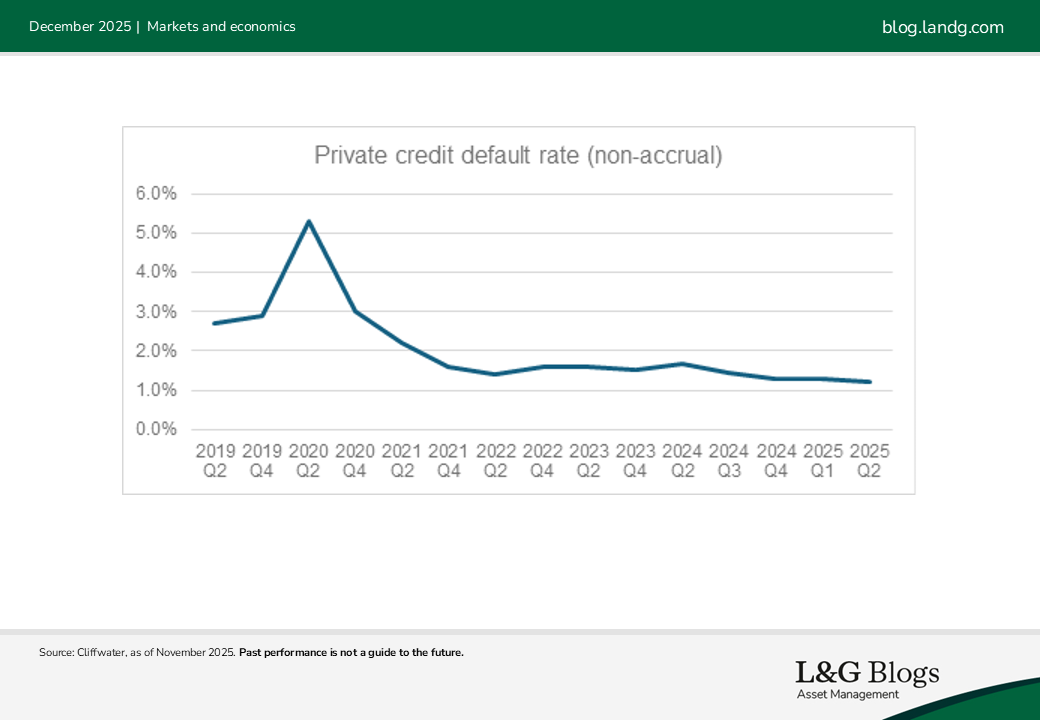

The distinction is important as we discuss the recent bankruptcies of First Brands* and Tricolor*, which have together created a lot of anxiety over the health of the private credit market. Both First Brands and Tricolor are sub-IG; thus their failures had no impact on the IG private credit market. Sub-IG exposure is also very small. Using Business Development Companies (BDC4) data as a proxy we estimated direct lending exposure to First Brands is significantly less than 1%.5

Idiosyncratic cases like First Brands point to emerging cracks but, in our view, there’s no clear evidence pointing to broader stress in sub-IG private credit. Default rates in direct lending remain low and falling interest rates should support debt servicing.

Nevertheless, recent events have been a useful wakeup call and once again emphasise the importance of robust underwriting and portfolio diversification. Investor caution should drive better underwriting standards which could lead to improved credit performance for future vintages.

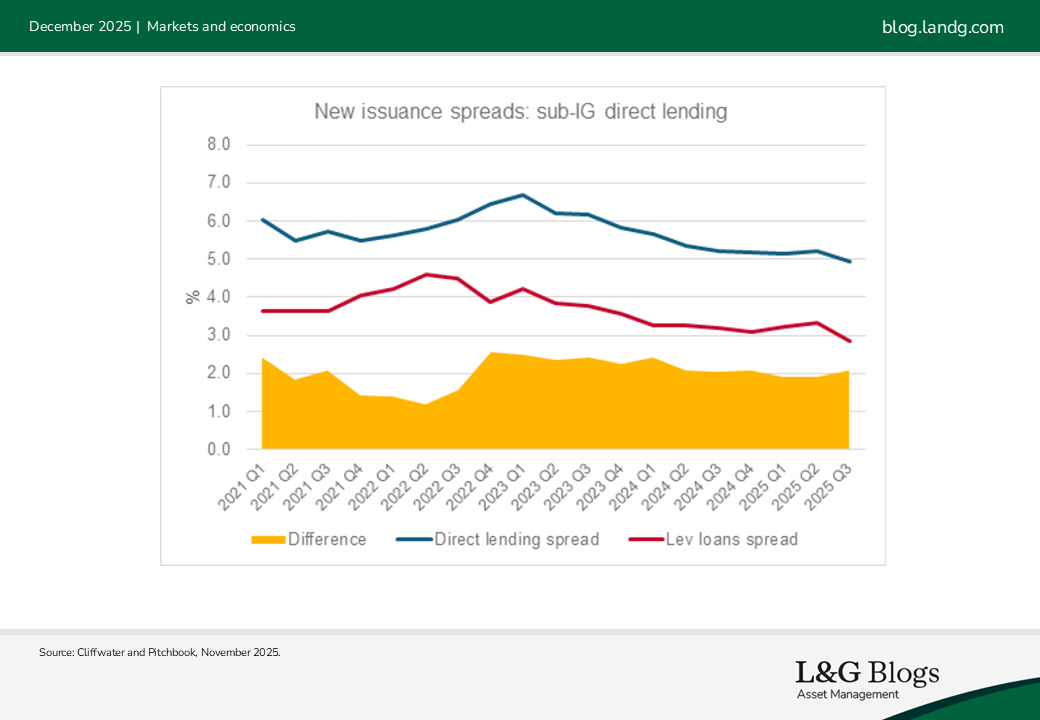

There are other reasons to be highly selective in this asset class, such as significant spread compression seen this year. In the public market, US IG and high-yield bond spreads are now below the 10th percentile versus the last 20 years6. Private credit spreads have followed a similar pattern, although the spread difference between public and private credit has remained relatively stable this year.

As at end of Q3 2025, sub-IG (direct lending) yield has dipped below its 10-year average. At c.10% it is still attractive relative to most private market asset classes, but the floating-rate yield will soften further with more rate cuts. IG (c.5-6%) screens more strongly on a tactical basis driven by still elevated base rate. It also offers fixed-rate assets enabling investors to lock in current yield. Lower interest rates could be mitigated by spreads widening, driven by either worsening macroeconomic conditions or an increase in supply from lower rates and AI capex.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts will come to pass. Past performance is not a guide to the future. It should be noted that diversification is no guarantee against a loss in a declining market.

*For illustrative purposes only. The above information does not constitute a recommendation to buy or sell any security.

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.