Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Digital infrastructure: AI keeps the pressure on

2026’s opening months reinforced the reality that AI and digital infrastructure are co-evolving.

Data centres dominated digital infrastructure transactions in the opening quarter of 2026. This came against a backdrop of hyperscaler capex rising again, generative artificial intelligence (GenAI) capabilities being bolstered, and value being repriced across the vertical AI infrastructure stack.

At the same time, Europe’s sovereignty agenda, tight power supply constraints, telecoms regulation and a higher‑for‑longer rate environment continued to shape the investment outlook.

Fundraising and transactions show appetite for digital infra

Fundraising closed 2025 delivering a record year. Funds have been taking longer to close – around three years versus under two pre‑2022, as distributions have remained muted.[1] Some large closes in 2025, therefore, may have reflected several years of pent‑up fundraising.

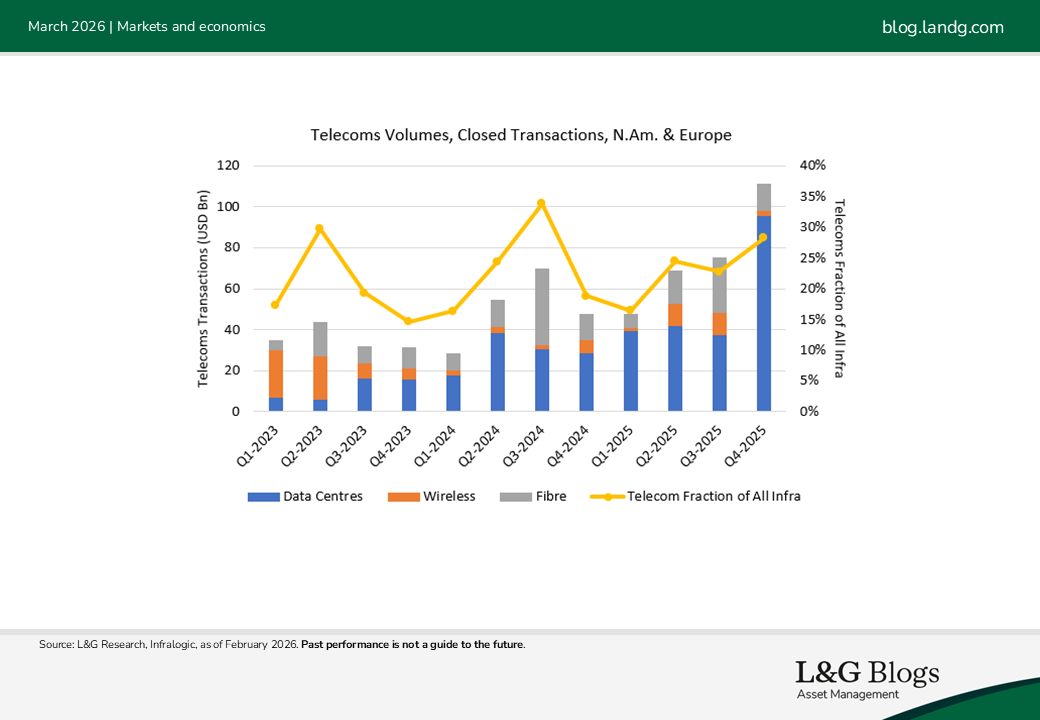

Transaction activity was dominated by data centres, with Q4 2025 seeing a record period of activity. Dealmaking in towers and fibre was comparatively quiet.

The US remains more greenfield‑led, while Europe is more M&A‑driven.[2] Tower and fibre activity in Europe stayed softer, which we believe reflects valuation pressure and financing constraints from higher rates. If yields remain elevated, this subdued activity may persist.

Data centre demand continues to strengthen

We see Europe and the US diverging. US leasing strengthened through H2 2025, while Europe’s improved only modestly. The continent now represents a smaller share of combined demand. This increases the potential future opportunity for Europe if data centre power demand balances on a per capita basis, in our view.

Nevertheless, the underlying picture is clear. Vacancy remains low and both regions are being pushed beyond traditional primary hubs. More than half of 2025 leasing took place in non‑primary markets, driven by power scarcity and land constraints.[3] On supply, the US is expanding more aggressively, with a higher share of live capacity under construction. Europe is growing more steadily, with increasing momentum in non-primary markets.

Big Tech revenues again rose strongly, accompanied with further upward revisions to capex guidance, supporting the view of greater momentum in AI infrastructure buildout. Commentary seems to support that supply is constrained, with grid access a key constraint.[4] While some spend is being absorbed by higher chip costs, infrastructure demand remains strong.

AI continues to grow

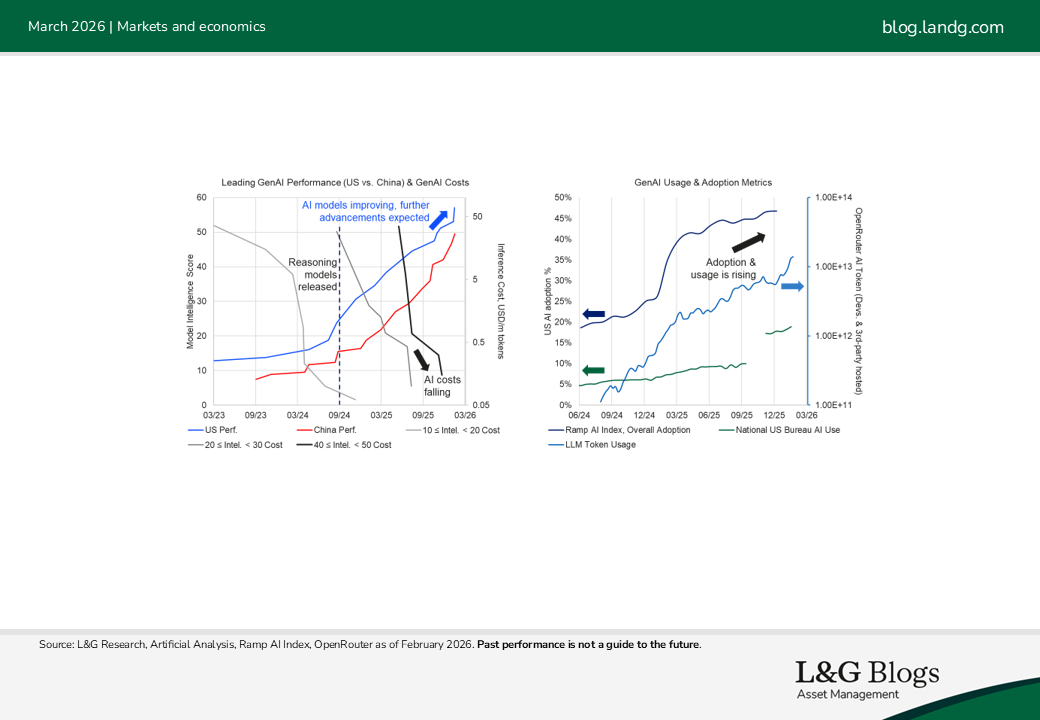

AI revenues continued to scale rapidly in 2025, even if overall profitability remains uncertain. Inference economics are improving, yet total costs - including training, talent and revenue‑sharing - still dominate financial outcomes[5]. We believe the clearest path to profitability is likely to be found in cost efficiencies and vertical integration.

The supply chain continues to validate demand. Nvidia* delivered another strong quarter, and neocloud providers are starting to report longer contract tenors[6], suggesting increased visibility on medium-term robust AI demand. Meanwhile, model capability keeps increasing, inference costs are falling, and token usage is growing exponentially. In our view, this expands the range of economically viable applications while reinforcing data centre power demand.[7]

Improving GenAI capability triggered a sell‑off in listed software, while private AI‑native businesses have continued to revalue upward at significant growth rates. It would appear markets are questioning the defensibility of some traditional software models as GenAI enables faster development.

For digital infrastructure, we see this cutting both ways. Weakening tenants in the software sector could pressure credit quality, but competitive pressure may also accelerate AI adoption, increasing demand for AI data centre capacity.

Geopolitics are increasingly central. Europe’s ambitions on sovereign cloud and sovereign AI continues to intensify, though these are impeded by the significant capital needs of data centre infrastructure. In our view, increasing GenAI capabilities could greatly enforce the need for AI sovereignty. Cloud managed services, which support cloud migration and ongoing cloud operations, could benefit from rising GenAI capabilities and adoption in our view, particularly as enterprises increasingly require hybrid, secure and sovereign AI environments.

Meanwhile, we believe US-China competition and semiconductor concentration remain key long‑term risks, reinforced by tensions around Taiwan and growing links between frontier AI models and defence.

Data centre investment dynamics see signs of stabilising, but exposure is moving to earlier stage development

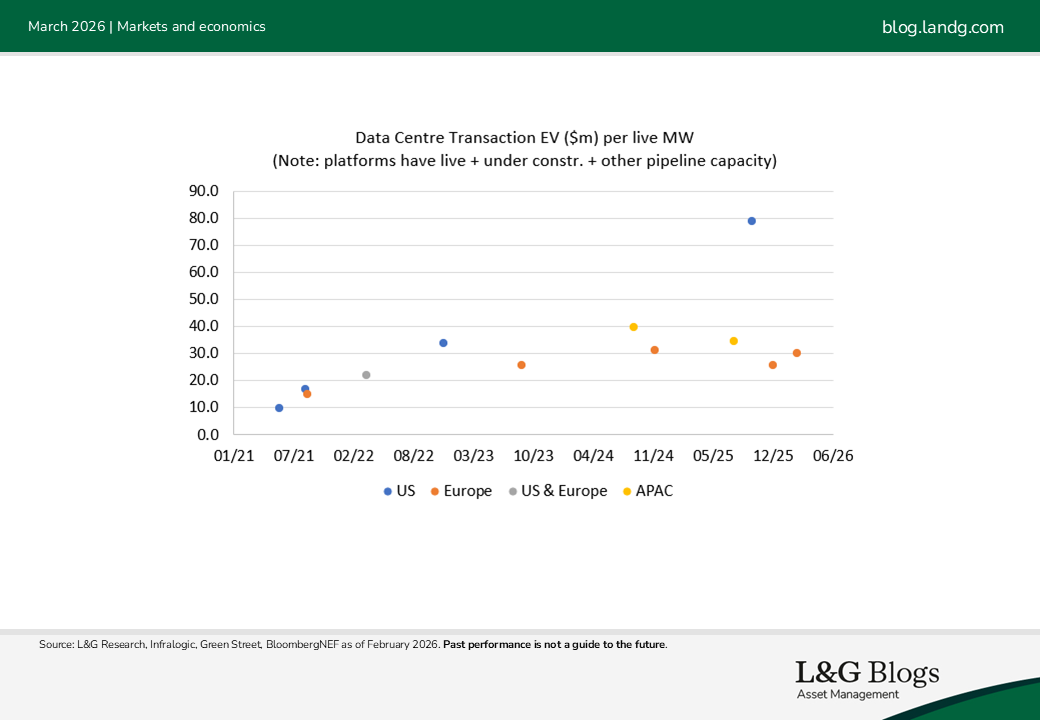

Valuation EV/EBITDA multiples appear balanced relative to their 5-year average around ~25×, and cap rates remain largely unchanged. However, we are seeing a divergence in return profile. US returns are being supported more by capital growth, potentially driven by more greenfield projects. On the other hand, the UK remains more income‑oriented. Tracking the EV as a multiple of live MW (so measuring how much investors are paying if development pipelines became unviable), we see a broad stabilisation in 2025 (at least on available data), particularly in Europe, suggesting to us a level of investor discipline.

Data centre hyperscale revenue growth favoured the US in 2025, reflecting a stronger demand profile.[8] Secondary European markets, such as the Nordics and Iberia, are increasingly seen as credible supply growth locations. The key underwriting risk, in our view, is delivery: capital is moving earlier into land, power and permitting, while grid delays and equipment lead times are causing more projects to stall. Markets where announced supply reliably converts into live capacity may command a premium.[9]

Towers and fibre offer selective opportunities

Listed towers valuation multiples remain subdued as yields remain elevated. European telecom mobile revenue growth has softened, and potential cybersecurity‑driven equipment replacement could, in our view, slow tower leasing.

European fibre remains highly market‑specific. We believe the UK shows some reparative signals but is still digesting overbuild, uptake challenges, and financing stress, with consolidation ongoing. Elsewhere, copper switch‑off policies support long‑term migration, but competition from both altnets and alternative wireless technologies including satellites is intensifying. We see fibre’s strategic case remaining intact, but navigating the fragmented European market is reliant on expertise and informed insights.

Final reflections

Three months into 2026, three themes stand out. First, AI demand remains structurally strong, supported by capex, rising GenAI capabilities, and tight capacity. Second, competitive advantage is shifting toward power, permitting and execution. Third, Europe still offers opportunity, but risks falling further behind the US unless ambition is matched by faster delivery.

From an investment standpoint, we believe the opportunity set remains compelling, just increasingly differentiated. This means it is critical to be precise about where value is created and where risk might be concentrating. This reinforces the need for diversification in portfolios across digital subsectors and geographies as AI market dynamics accelerate.

Assumptions, opinions and estimates are provided for illustrative purposes only. There is no guarantee that any forecast will come to pass.

* For illustrative purposes only. Reference to particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] Preqin as of February 2026, MSCI Private Capital Benchmarks Report 2025 Q3.

[2] Infralogic as of February 2026.

[3] Data Center Hawk, 4Q 2025 Data Center Market Recap, January 2026

[4] Company Management Earnings calls, Q1 2026; Reuters, “Power grid delays challenge Amazon's data center expansion in Europe”, February 2026; Reuters, “Google says US transmission system is biggest challenge for connecting data centers”, January 2026

[5] Epoch AI, Can AI companies become profitable?, January 2026

[6] CoreWeave Earnings call, February 2026; Goldman Sachs Research, Nebius Group, February 2026

[7] Artificial Analysis, Ramp AI Index, OpenRouter as of February 2026

[8] Green Street, 2026 Global Data Center Outlook, January 2026

[9] DC Byte, 2026 Data Centre Outlook, January 2026

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.