Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Latin love — Why we like South American bonds

Latin America’s early‑moving central banks are tightening once more as inflation pressures rekindle. Yet with real rates still priced at extreme levels and the political tide turning more market‑friendly, could long‑duration local bonds offer a compelling opportunity?

Key takeaways

|

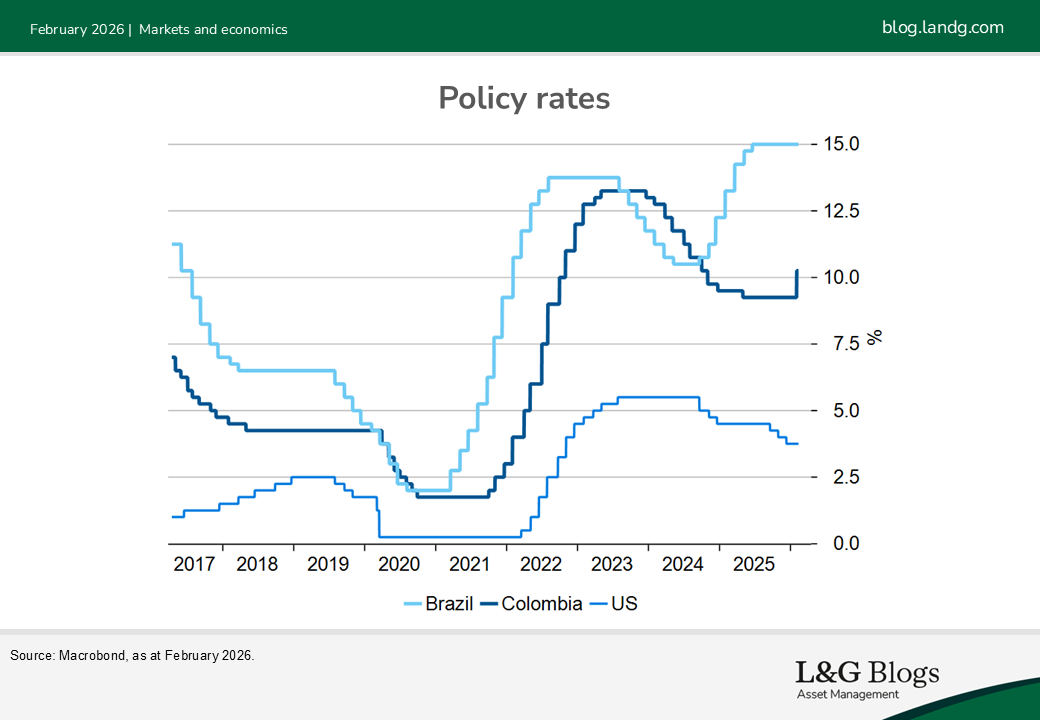

Latin American central banks have caught our attention. They were ahead of the curve when inflation spiked after COVID-19. They were the first to hike interest rates and the first to cut once inflation was under control.

Unfortunately, not all governments played along with those efforts. Once inflation returned to target, Brazil embarked on a large fiscal expansion culminating in a deficit above 12% of GDP. Inflation expectations de-anchored and inflation breached the target once again.

Similar dynamics were at play in Colombia. Bogota’s fiscal expansion started earlier and was over a shorter period, keeping inflation above target all throughout. The government abandoned the fiscal rule and when it raised the minimum wage by 23% in January, inflation expectations shot past 6%, three percentage points above target, even as the wage hike remains caught in a legal back and forth.

Central banks respond

This time central banks made sure their message was heard. Banco Central do Brasil raised the policy rate to 15% by mid-2025, significantly above the previous peak. Colombia’s central bank hiked rates by 100bps immediately after the minimum wage increase and economists expect another 100bps of hikes, taking the policy rate to 11.25%.

In our view, while a 13% yield on local currency bonds is enticing, we believe even greater potential could be in the offing when rates are cut again. In Brazil, the economy is slowing and both inflation and inflation expectations have returned to target. The first rate cut could come in March and we expect similar, albeit lagged dynamics in Colombia.

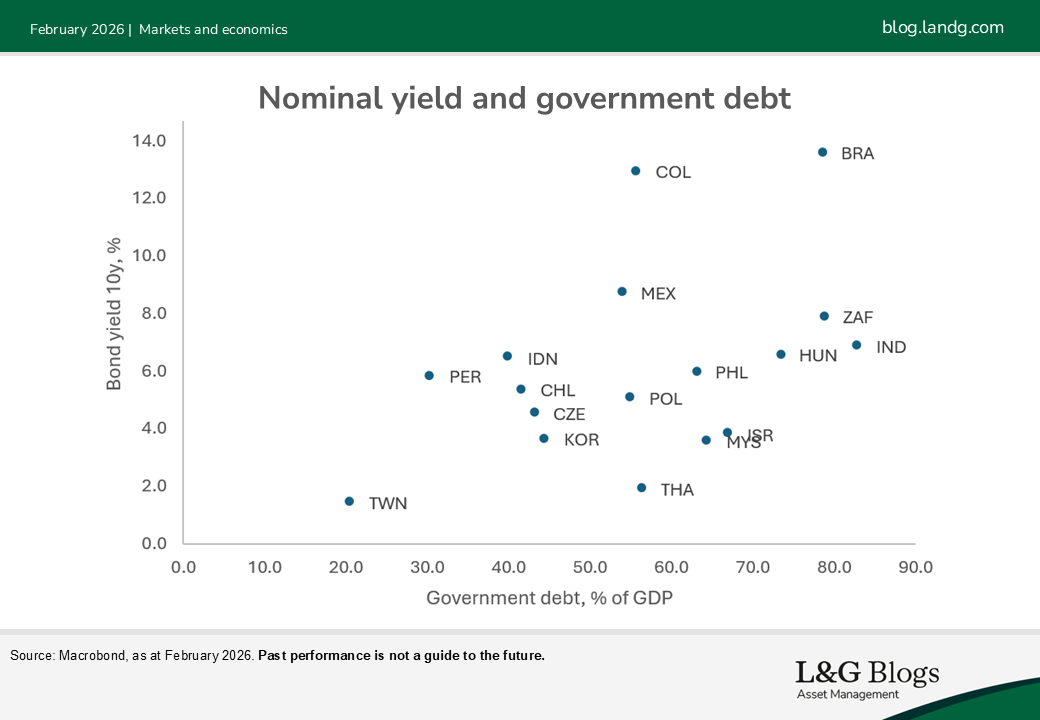

Is it all in the price? We don’t think so. In Brazil, markets are pricing a real policy rate (ex-ante) of 9% by year-end versus a historical average of 6%. In Colombia, the equivalent values are 8% versus 1%. On top of that, Colombia has the steepest yield curve among its emerging market peers by a large margin. In both Brazil and Colombia, 10-year yields are at the 87th percentile.

Long-term yields not only reflect monetary policy, but also credit risk. So, how worried should we be about debt dynamics? At close to 60% of GDP, Colombia’s government debt is close to Mexico’s with yields that are 400bps above Mexico’s. At 80% of GDP, Brazil’s debt is close to South Africa’s with yields that are 570bps higher.

There is a relationship between local currency yields and debt-to-GDP levels: When debt gets excessive, investors worry that central banks are forced to monetize the local currency debt. This inflation fear pushes long-term yields higher.

Could politics provide a tailwind?

The political cycle in Latin America could also potentially be shifting to a more favourable environment for investors. From the late 1990s to the early 2000s, Latin America voted leftist governments into power in what became known as the Pink Tide. This tide has turned decisively. Conservative governments have been elected in Argentina, El Salvador, Bolivia, Honduras and Chile. In Colombia, a win of the right looks more likely than not according to polls. In Brazil, Lula is still leading in the polls, but his right-wing challenger is catching up. Right-wing governments tend to generally be favoured by markets.[1]

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass. Past performance is not a guide to the future. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] Latin America’s turn to the right has been attributed to a desire for anti-crime policies, which is linked to the tripling of cocaine production over the past decade (see UNODC World Drug Report 2025).

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.