Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Infrastructure: A look back at a look ahead

Infrastructure saw record fundraising in 2025 driven by megafunds. Transaction volumes, particularly asset creation, continue to be driven by digital and power demands, but face challenges like grid constraints and talk of an ‘AI bubble’. Growth continues, with diversification and investment discipline critical amid ongoing uncertainty and evolving market dynamics.

The year gone by…

Infrastructure attracted strong investor interest in 2025 with record fundraising amid rising investor allocations. These came on the back of strong performance and the need for asset creation to support growing global digital and energy demands[1].

This growth trajectory relative to infrastructure’s historically slower pace has created both challenges and opportunities. Grid capacity constraints have commoditised power interconnections, supporting data centre returns for those with access but delaying those without. Elsewhere, a lack of flexibility has led to blackouts and negative power pricing that challenged renewables but has boosted demand for battery storage.

Layering on DeepSeek, tariffs, and the One Big Beautiful Bill, 2025 has created uncertainty for infrastructure, stressing the need for diversification across geography and asset type.

Growth amid uncertainty

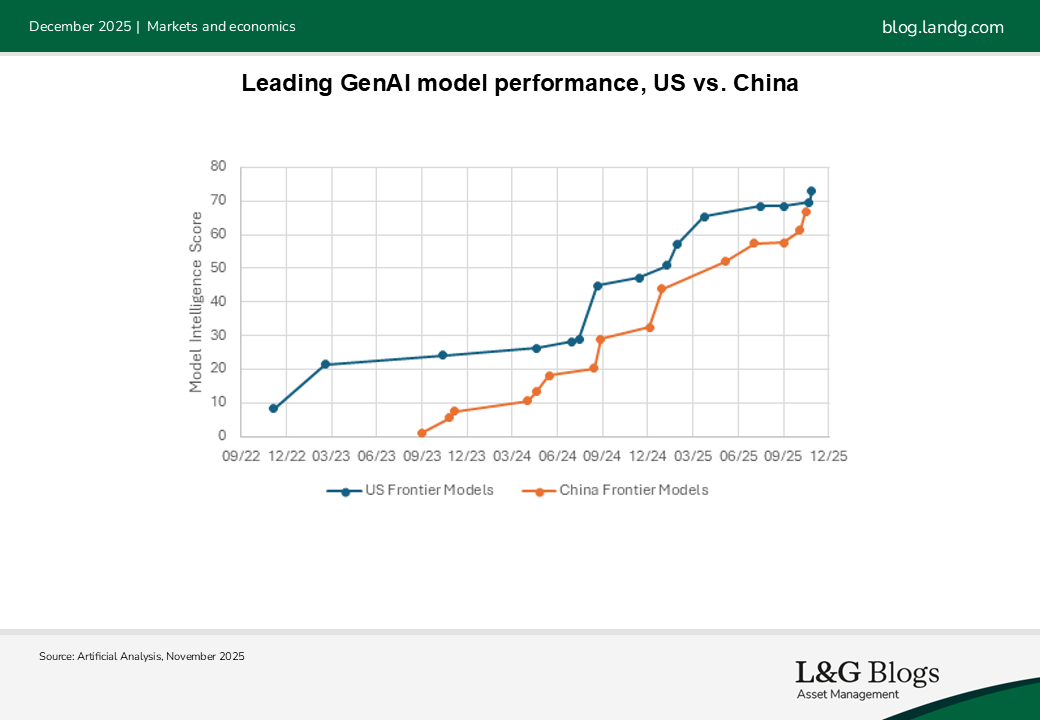

Despite uncertainty, growth and performance has continued apace. Demand for AI infrastructure has continued to outstrip supply[2]. Digital and (clean) power infrastructure have increasingly converged, and we’ve observed cheap, abundant and green energy alongside strong fibre connectivity driving ‘prime secondary’ markets for data centres, particularly in Europe.

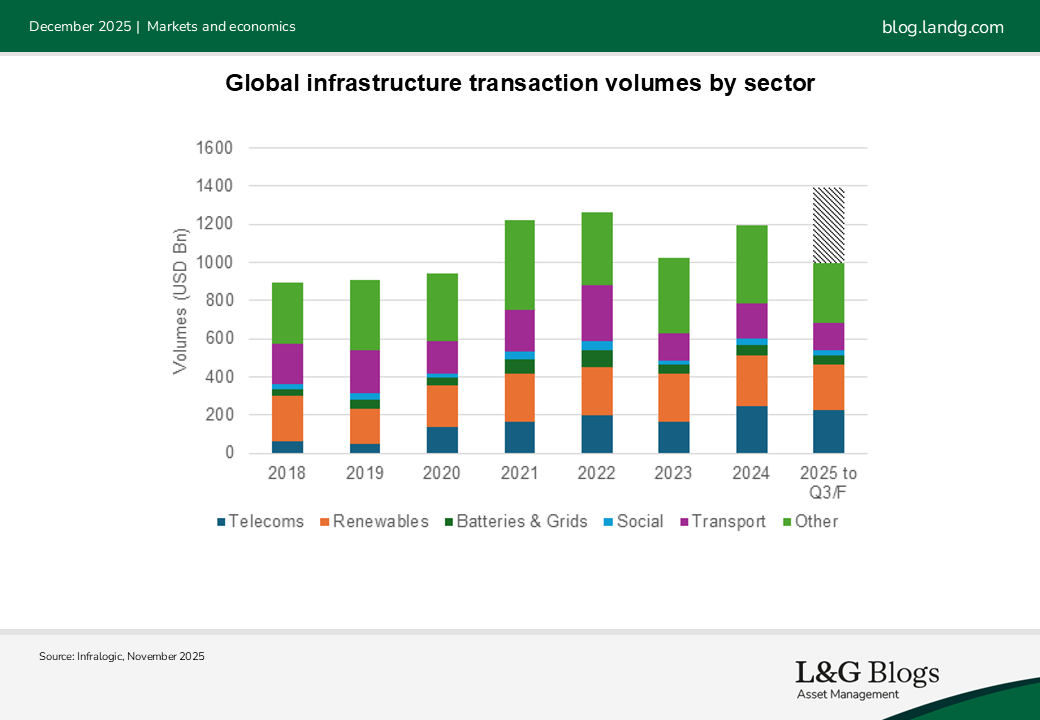

While transaction volumes in the transport, energy and power sectors (excluding nuclear and battery storage) have remained stable compared to 2024 levels, there has been growth in digital and renewables infrastructure, leading to record volumes in Europe and North America.

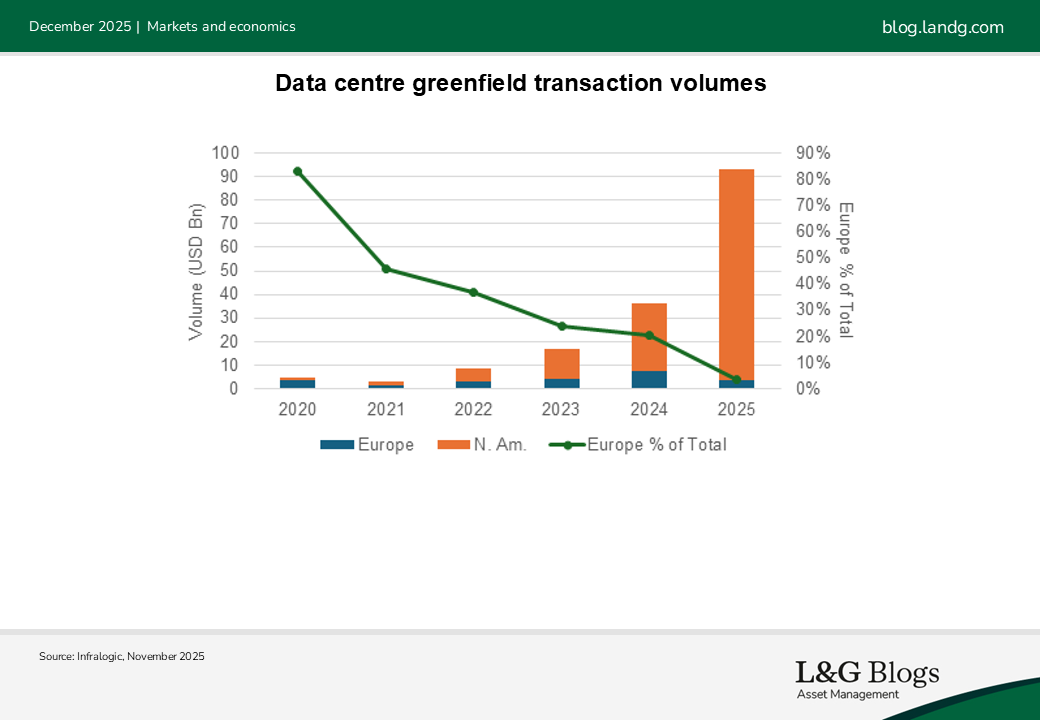

Regionally, this has been driven by the US and UK, while volumes in continental Europe are expected to remain more stable. The need for asset creation is reflected by record greenfield transactions in 2025, which is supported by data centres and renewables assets, underscoring the digitalisation and decarbonisation megatrends. Notably, deployment into European renewables has persisted despite challenges from negative power pricing and grid constraints, enabled by falling clean power development costs.

Such growth has certainly not escaped scepticism, however, with rising chatter about an ‘AI bubble’. With US data centre greenfield volumes being 11 times higher than those in Europe since the start of 2024, we believe bubble risk in infrastructure is more concentrated in the US[3]. Understanding how a potential bubble materialises in valuations and returns across infrastructure becomes key to fully measuring AI exposure and how to diversify against it. Strong investment discipline and gaining conviction on demand from the ultimate end user of an asset will be crucial.

At the end of 2024, we expected that 2025 would see national security and AI data centre capacity becoming more aligned. Subsequently, Western policy plans confirmed this trajectory: the US aimed to export AI to allies, while Europe sought to develop sovereign capabilities.

While AI sovereignty is a key demand driver, our view is that European firms are unlikely to have the fiscal capacity to fund their own AI infrastructure buildout and compete globally. Instead, the scale of capital needed requires a regional view: current capital flows into Europe by US Big Tech is deepening the continent’s reliance on US AI rather than Chinese alternatives, reinforcing Western security objectives.

However, as Chinese technology permeates Europe, including in clean power infrastructure, we anticipate a greater possibility of Chinese AI expansion into Europe in 2026. What does this mean for investors? We expect investment opportunities in European data centres to continue to be driven primarily by US hyperscalers over the next 12 months. Furthermore, investors should assess counterparty risk: emerging AI neocloud providers face weaker credit profiles, while Chinese firms, despite strong balance sheets, may carry significant geopolitical exposure.

With investors looking to increase allocations to infrastructure, we expect a strong fundraising environment in 2026. Volume could be tempered from the 2025 highs but still robust. We anticipate continuous strength in demand for digital assets, though uncertainty will persist with respect to AI’s longer-term trajectory. The need to decarbonise could be met by greater challenges for renewables from negative power pricing, boosting needs for greater grid flexibility.

We are left with pertinent questions for 2026. Notably, if the AI bubble does burst and given data centres are commonly defined as ‘infrastructure’, would this lead investors to reframe their traditionally stable and resilient view of the asset class? Could this bifurcate infrastructure between a traditional segment and an ‘infra 2.0’ that demands a higher risk premium? 2025 has reminded us to stay humble in our outlook, but we have conviction that the space becoming increasingly dynamic.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts will come to pass. Past performance is not a guide to the future.

It should be noted that diversification is no guarantee against a loss in a declining market.

1. Prequin, as of November 2025

2. Company reports, as of November 2025

3. Infralogic, as of November 2025

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.