Disclaimer: Views in this blog do not promote, and are not directly connected to any L&G product or service. Views are from a range of L&G investment professionals, may be specific to an author’s particular investment region or desk, and do not necessarily reflect the views of L&G. For investment professionals only.

Unconstrained strategies: keeping an eye on AI

How can unconstrained bond investors navigate AI-related issuance?

This article is an extract from our Q1 2026 Active Fixed Income Outlook.

The past – what just happened?

In recent years, the world’s largest technology firms have been pouring significant sums into artificial intelligence (AI) related spends. The competition for capital is set to intensify in 2026. According to a recent McKinsey report, hyperscalers will spend nearly $7 trillion in AI-related capital expenditure by 2030, while Morgan Stanley estimates a spend of $3 trillion over the next three years.

Even with hyperscalers funding a healthy portion of this from their free cash flow, the implication is $500-800 billion of additional debt annually, or $2-3 trillion cumulatively by 2030.

Companies like Microsoft* and Amazon* have already been committing tens of billions annually to AI-related capex, largely funded from retained earnings. Despite their sizeable current commitments, forecasts suggest that to meet demand, over half of the required investment will need to be sourced from alternative funding methods – debt, for example.

Towards the end of 2025, four hyperscalers (Microsoft*, Amazon*, Meta* and Alphabet*) were expected to have spent a combined $250 billion in 2025[1].

Present – positioning and performance

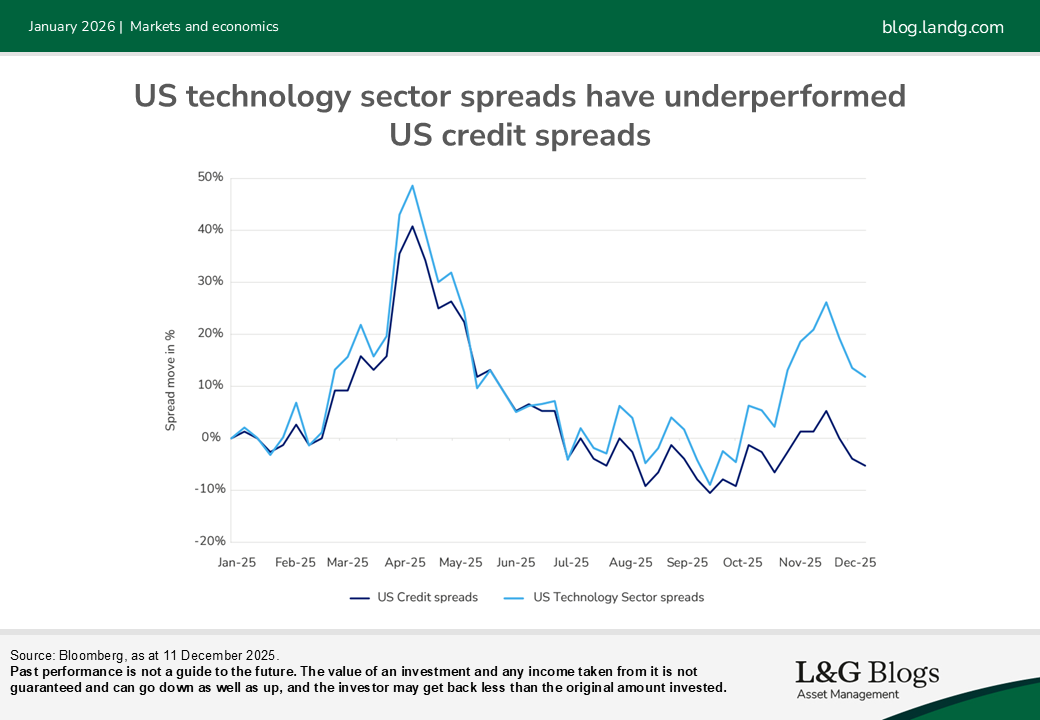

These substantial funding requirements and expected increase in issuance have the potential to exert widening pressure on spreads. This is something we have already started to witness as the US investment-grade technology index has underperformed the US aggregate credit index since May 2025, amid record tech debt issuance (c. $100 billion in the fourth quarter of 2025 alone).

As a result, we continue to be cautious over investment grade credit as spreads have limited room to compress. We prefer to own higher income-generating assets such as subordinated bank debt, as we believe banks remain strongly capitalised and their margins are benefitting from the upward sloping yield curve.

Emerging markets are another area we currently like. Although valuations are not as attractive as in the past, we believe fundamentals are improving in contrast to deteriorating government deficits in many developed markets.

Outlook

Despite the staggering scale of investment required to support AI infrastructure, the largest hyperscalers appear well positioned to manage the financial burden in the short term. Strong free cash flow, benefitted by tax incentives, strong credit ratings, and diversified financing strategies (including private credit and securitisation) give these firms the flexibility to scale rapidly, in our view.

While risks like overcapacity and tech obsolescence remain, the current financial and policy environment suggests that it is possible that the aggressive hyperscaler expansion may also be financially sustainable, at least for the Big Tech players.

However, timing is key, and constant issuance could weigh on credit spreads. Some prominent deals have underperformed shortly after primary issuance, and the Global Unconstrained Bond team has selectively added exposure through both primary and secondary markets. As those issuers continue to turn to the public credit market for their funding needs, their weight in key indices such as US credit will continue to increase. Currently expectations vary from $200 billion to $400 billion of increased public market AI issuance for 2026. This would be an increase of c. 20% from 2025 gross US investment grade issuance figures from one sector alone. If you add in funding pressure from the energy/utility sector required to power this AI initiative, this may weaken the technical balance within US credit spreads which are already entering 2026 at very compressed levels.

What could go wrong?

Away from the public market pressure, increasingly we’ve seen hyperscalers accessing private credit markets, particularly for bespoke or off-balance-sheet projects; Meta’s* recent $29 billion public/private credit deal is a notable example – and our colleague Ken Berlin has explored this in more detail on page 22. Some operators are exploring securitisation, packaging long-term lease income from data centres into asset-backed securities (ABS) to raise capital while keeping debt off the parent company’s balance sheet. Given the size of the private credit and securitised markets they are likely unable to absorb all of the proposed issuance. We expect that hyperscalersmay increasingly need to use hybrid deals to source funding. This diversified capital stack may enable hyperscalers to maintain flexibility, manage risk, and scale rapidly in response to surging AI compute demand.

The rapid expansion of the market will inevitably create winners and losers. In this environment, the case for an active approach is compelling, in our view. Active strategies, leveraging bottom-up credit selection, can selectively own stronger issuers and exploit opportunities created by constrained investors who may lack flexibility to avoid crowded trades.

This article is an extract from our Q1 2026 Active Fixed Income Outlook.

Assumptions, opinions, and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

*For illustrative purposes only. Reference to a particular security is on a historic basis and does not mean that the security is currently held or will be held within an L&G portfolio. The above information does not constitute a recommendation to buy or sell any security.

[1] Source: Reuters, November 2025

Recommended content for you

Learn more about our business

We are one of the world's largest asset managers, with capabilities across asset classes to meet our clients' objectives and a longstanding commitment to responsible investing.